1. Introduction

The analysis of big business and its role in economic development is a crucial topic in economic and business history literature. From the studies of Ronald Coase and Alfred Chandler, the trajectories and growth strategies of large firms were incorporated into the analysis of the development of industrial capitalism (Chandler Reference Chandler1987). In recent decades, the questioning of the Chandlerian paradigm of postulating the large U.S. industrial enterprise as a normative model of business development was formulated from several perspectives (Chandler and Takashi Reference Chandler and Takashi1990; Hannah Reference Hannah1991; Chandler et al. Reference Chandler, Takashi and Amatori1997).Footnote 1 As noted by Cassis (Reference Cassis, Jones and Zeitlin2008), the role of big business has been set in a broader perspective, both theoretically and geographically, and «alternative» forms of large business organisation have been reappraised as part of modern societies rather than mere archaisms (Austin et al. Reference Austin, Dávila and Jones2017).

Several studies on late-industrialising European countries such as Italy or Spain or Asian countries such as Japan and Korea, have highlighted the diversity of institutional forms and the persistence of large family-owned corporations. In these countries, business groups (zaibatsu, keiretsu and chaebols) were the predominant organisational form of big business (see Colpan et al. Reference Colpan, Hikino and Lincoln2010). Meanwhile, in Latin America, several scholars have identified the significant presence of family-based business groups alongside foreign multinationals at the top.Footnote 2

In Argentina's case, historical studies have pointed out that foreign companies have played a key role in the economy and that the business group as an organisational form has become preeminent (Lanciotti and Lluch Reference Lanciotti and Lluch2018).Footnote 3 Family ownership was the norm in national firms rather than the exception (Barbero Reference Barbero, Jones and Lluch2015; Barbero and Lluch Reference Barbero, Lluch, Fernández and Lluch2016). Other studies have questioned the domain exercised by this type of company on the economic development of the country, as it implies that national income depends upon a few domestic and foreign groups controlling a large number of the big companies (Marichal Reference Marichal1974; Nochteff Reference Nochteff, Azpiazu and Nochteff1994; Schvarzer, 1995; Barbero Reference Barbero, Chandler, Amatori and Hikino1997; Manzanelli and Schorr Reference Manzanelli, Schorr and Schorr2013; Lanciotti et al. Reference Lanciotti, Schorr and García Zanotti2019).

As part of a broader and more comprehensive investigation of big business in 20th-century Argentina, this article provides the first comprehensive research into big business until the 1970s. Our analysis seeks to bring new evidence of the evolution and characteristics of capitalism in Argentina, from the perspective of business history. To this effect, the article analyses the structure and changes of corporate leadership based on a new database of the 200 largest non-financial firms operating from 1913 to 1971.Footnote 4 Our study explores the rise of large-scale enterprise in the context of a transformation, from an open and relatively wealthy resource-based economy to a more closed and unstable one in the 1970s. We also evaluate the complementary but competing participation of large national stand-alone companies, foreign multinationals and business groups in Argentinian corporate leadership between 1913 and 1971, with special attention to the impacts of external investment cycles and public policies. Finally, we also identify the main changes in the sectoral insertion of the largest companies throughout the period.

This article posits that Argentina's modality of insertion in the international market has a long-lasting trait: the role of foreign companies and locally controlled diversified business groups as conspicuous members of the corporate leadership, from the last quarter of the 19th century until the end of the so-called ISI period (Import Substitution Industrialisation), in 1971. Furthermore, we found that the presence of foreign companies among the 200 largest firms is higher than that identified in other countries, such as Italy or Australia, especially at the beginning (1913) and at the end of the analysed period (1971).Footnote 5

We also propose that the main changes affecting Argentinian corporations resulted from the impact of external investment cycles and industrial policies at two particular moments in time: at the end of World War II and in the 1960s. We argue that these changes were gradual but consistent with a shift towards state intervention to promote an economic development based on industrial activities during the second post-war period. In the 1960s, the government's promotion of new foreign investments in the most dynamic branches of industry consolidated the industrial profile of corporate leaders. The latter process oriented the rise of a new techno-economic paradigm; however, it was abruptly interrupted by the military dictatorship that came to power in 1976.Footnote 6

This paper is organised in three main sections. The first section presents a synthesis of the methodological aspects of the research. The second section synthesises the long-term evolution and main changes in the population of the largest firms between 1913 and 1971. The third section presents the conclusions.

2. Methodological notesFootnote 7

As Cassis (Reference Cassis, Jones and Zeitlin2008) observes, the concept of big business is one of the most commonly used yet least clearly defined in business history (Chandler et al. Reference Chandler, Takashi and Amatori1997). Even though a priori it may seem a straightforward definition, by considering the relative sizes among firms and narrowing down the focus to only the first 50, 100 or 200, different debates have emerged about what type of firm should be considered as such, the impact that national contexts may have on this definition, and the firms' origins, dominant features, and functions in the economic system.

Ville and Merrett (Reference Ville and Merrett2000, p. 14) have discussed the different criteria used for measuring the relative size of firms—including assets, output, sales, paid-up and market value of capital—or size of the labour force. As they rightly remark, none of them provide unambiguous size measures. For example, the number of employees can be misleading when comparing sectors, while production or sales figures are only useful when they allow value-added to be distinguished. Market capitalisation has been preferred in countries such as the United States or some European countries (England, Germany).Footnote 8 This indicator, however, is inadequate for companies whose shares were not listed or rarely traded, as in the case of Argentina where a minority of companies sought a stock exchange listing.Footnote 9 Including foreign companies into the analysis has not always been the norm in Europe or the United States. Still, it is appropriate to do so in countries such as Argentina. Finally, all historical measures face significant problems with access to information and, subsequently, data collection. Thus, we agree with Ville and Merrett in that the use of different methodologies «means that figures on absolute firm size must be analyzed circumspectly although the broad parameters for comparison remain valid» (Ville and Merrett Reference Ville and Merrett2000, p. 15). Our research is based on the elaboration of a homogeneous series of long-term companies that operated in Argentina from 1913 to 1971. We registered, organised and classified the data of the corporations listed in the directories/guides edited for seven benchmark years: 1913, 1923, 1930-1931, 1937-1938, 1944, 1959-1960, 1970-1971. The selected benchmarks allowed us to identify the changes that occurred in the population of the largest firms until the 1970s. These dates not only track the changes within the structure of the Argentinian economy, but also allow future comparisons with similar studies done for other countries. The sources of information varied between different years and are listed in the «References». In addition to the primary sources, information was obtained from the following publications: Monitor de Sociedades Anónimas, El Avisador Mercantil, El Cronista Comercial, Revista Veritas, Revista La Información and Revista Mercado. A nominal search was used in case of doubts or other situations.

We later created the ranking of the 200 largest non-financial firms for each year. Identifying the largest businesses for a single year is a substantial task since it is only by considering all relevant firms that it is possible to complete a size ranking by year. In this analysis, the fully paid-up capital stock has been adopted as the unit of measurement for it provides the most broadly available data across the whole period. The information was systematised in the «Base de Datos de Grandes Empresas en Argentina [Database of the Largest Companies in Argentina] BDGEA/BCAD (1913-1971) BID PICT 2015-3273.» This database provides the first available rankings for the whole period since the publication of the rankings based on annual sales dates from 1955, and there was no information on the preceding period. Moreover, previous figures were incomplete in terms of sectors (particularly the first ones published by Panorama de la Economía Argentina between 1955 and 1969, and later by Mercado or Prensa Económica).

Cassis (Reference Cassis, Jones and Zeitlin2008, p. 173) proposes three questions to understand big business: first, should the notion be defined in absolute or in relative terms, and in the case of the latter, should it be contingent on period, country size or other factors? Second, should only large industrial enterprises be considered as those that make up the world of big business, or should firms from other sectors also be included? And third, should the frontiers of big business be limited to the firm's unit, or should other forms of organisation be considered? (Cassis Reference Cassis, Jones and Zeitlin2008, p. 172).

By answering these questions, we identify Argentina's largest companies. Second, and as explained above, we opted for an absolute definition: a fully paid-up capital stock, but relative to the year of measurement and the companies' contexts. This type of capital was chosen, instead of other indicators, because our sources do not provide information on annual sales or asset values for the period of analysis. We decided to include firms from all sectors (except banking).Footnote 10 We also considered foreign companies because FDI was manifest in many parts of the economy.Footnote 11 Consistent with other similar studies, most state-owned companies are not included, except for those incorporated as «Corporations».Footnote 12 However, we include complementary information about state-owned companies, based on secondary sources so as to evaluate the role of the government as an entrepreneur; a widely developed topic in Argentinian historiography (Belini and Rougier Reference Belini and Rougier2008). Finally, since our sources analyse corporations [Sociedades Anónimas], we took each company as a unit of analysis. Still, we consider their insertion or integration within corporate networks and business groups.

Two more comments are worth noting.Footnote 13 The conversion of capital stock into dollars was necessary to integrate the data from both domestic and foreign companies. As for the activity carried out by the companies, in each case we chose to prioritise the main activity based on secondary sources. For the activity description, we used the categories proposed by the International Standard Industrial Classification of all Economic Activities, Rev. 4 (ISIC. Rev. 4).

3. The development of argentina's 200 largest firms: investment cycles and sectoral insertion

3.1 The first global economy (1870-1914)

During the first globalisation, the Argentinian economy specialised in producing and exporting agricultural raw materials to northern Europe. The most dynamic activity of the Argentinian economy was the production of agro-industrial goods and associated trade and financial activities. At the same time, domestic capital was concentrated in the production of agricultural goods and livestock and the production of consumer goods for the domestic market.

Economic specialisation was driven by the entry of northern European firms, mainly from Great Britain, investing in infrastructure (railroads and public services), commercial and financial services for export. By 1913, the most capitalised firms were British (see Table 1). The French and Belgian companies had a sectoral insertion similar to that of the British and also concentrated on transportation, infrastructure, credit and finance.Footnote 14 This cycle of foreign investment in the country began in the 1870s and lasted until the railroads and public utilities were nationalised in 1947-1950 (Lanciotti and Lluch Reference Lanciotti and Lluch2018) (see Figures 1 and 2).

Table 1. Top 10 firms, Argentina, 1913 and 1930

Source: Base de datos de Grandes empresas en Argentina—BDGEA/BCAD (19131971) BID PICT 20153273.

Figure 1. Argentina's largest firms by origin, 1913-1971.

Source: Base de datos de Grandes empresas en Argentina—BDGEA/BCAD (19131971) BID PICT 20153273.

Figure 2. Largest foreign companies by country of origin, 1913-1971.

Source: Base de datos de Grandes empresas en Argentina—BDGEA/BCAD (19131971) BID PICT 20153273.

The production of wool, meat and cereals, along with the impact of European immigration into the Pampas, shaped a dynamic domestic market at a high economic growth rate (Barbero and Rocchi Reference Barbero, Rocchi, Della Paolera and Taylor2003). This market encouraged the creation of local companies and the emergence of powerful business networks that linked traders of European origin, who settled in Argentina, with British, Belgian and German exporting and importing companies. As a result, by the end of the 19th century, a business elite closely associated with the commercial networks of northern Europe was formed. The members of this group became central players in corporate power, as reflected in the list of the largest companies in 1913.

On the eve of the Great War, the number of Argentinian and foreign firms among the 200 largest companies was equivalent. Among the foreign firms, 81 per cent were British (see Figures 1 and 2). This dominance was even more pronounced if we look at just the first ten positions in the ranking. The prominent presence of railroad companies at the top of the ranking is not surprising. As Cassis rightly summarises, railway companies were, on a global scale, the first companies to face organisational challenges due to their large scale in terms of costs, investment, internal organisation and coordination of their operations (Cassis Reference Cassis, Jones and Zeitlin2008, p. 176; Chandler Reference Chandler1987).

Therefore, among the largest foreign companies, British dominance was undisputed before the First World War (Figure 2, Table 1). American and German firms had a negligible presence (Figure 2) in those years, although they led strategic activities, such as the meatpacking industry and the electrical industry, respectively. The most capitalised companies in the food industry were the meatpacking plants, which were initially owned by British and Argentinian capital. With the arrival of Swift, in 1907, the scale of chilled meat exports increased, giving rise to the leadership of U.S. companies in this activity. As of the 1920s, three major players controlled the largest share of exports (US Swift and Armour and UK Anglo). The financial capacity of U.S. firms as well as the development of marketing structures in England favoured the displacement of older British and Argentinian firms from the meat production sector (Hanson Reference Hanson1938; Lluch Reference Lluch2019).

The 1913 ranking shows the highest number of partnerships (joint ventures) between Argentinian and foreign capital for the analysed period, around 10 per cent of the total (Figure 1). This share ratifies the early formation of alliances between Argentinian and foreign capital (primarily British and Belgian, and French) to invest in transportation and storage, cattle and quebracho exploitation and the food industry.

Our data also show the long-lasting presence among the largest firms of companies controlled by business groups with diversified investments in agriculture, land, finance, transportation and services (41 companies).Footnote 15 These business groups had some elements in common: (a) their investments were diversified in unrelated activities; (b) they were founded by foreigners residing in the country who acted as intermediaries between European investors and the local market; and (c) they were based on family networks. Early business groups were organised by traders of British, Belgian-German and French origin who settled in Argentina. They created commercial and financial companies based on kinship ties and grew through association with investors outside the family.

The largest Argentinian business groups expanded by diversifying investments from export and import activity to financial services and agricultural production. This was the case of the Italian group Devoto & Co, German-Belgian groups such as Tornquist and Bunge & Born, and the French group Bemberg (Marichal Reference Marichal1974). Early merchant houses created financial companies that acted as intermediaries in the negotiation of Argentinian securities and European banks, and shortly afterwards, in the 1880s, they diversified their investments into the real estate and mortgage sector. After the crisis of 1890, the wool, leather and grain exporting companies consolidated their position as financial intermediaries, eliminated their competitors and expanded their business from international trade to the local production of sugar, flour, quebracho and tobacco.

3.2 The first Post-World War period until the great depression

With the outbreak of World War I, Argentinian economic growth began to depend more and more on the expansion of the domestic market. In fact, industry became the most dynamic sector of the economy from the 1920s onwards (Barbero and Rocchi Reference Barbero, Rocchi, Della Paolera and Taylor2003). At this time, the level of effective protectionism had declined due to rising inflation and the failure to update customs duties. However, in 1923, the government of President Marcelo T. de Alvear promoted a customs reform that established a minimum level for inputs and machinery and higher tariffs for goods already produced in the country. Although it was not its objective, this policy of tariff protection created incentives for the arrival of new foreign firms.Footnote 16

In the 1920s, technological advances in agribusiness, new demands for goods, and modernisation in marketing and advertising techniques brought investment opportunities for new foreign companies. For example, at this time, Argentina was one of the world's major importers of agricultural implements and machinery. These items, unlike others, were not subject to higher customs duties, which facilitated the entry of foreign products. Most agricultural tools and machinery were British until 1913-1914, although this situation was radically altered after the First World War. From then on, U.S. dominance ranged between 80 per cent and 90 per cent, although with variations by type of product and period (see Avery, Reference Avery1925).

In this period of economic grow, Argentina's GDP grew more than that of the United States, Canada and Australia as the country received new foreign direct investment.Footnote 17 The locational advantages associated with the size and structure of the domestic market and low communication and transportation costs were decisive in this new wave of FDI. It can also be added that the level of taxation was low compared with the tax burden in the home countries. Legislation was also largely favourable to foreign firms. In some activities, such as transport and public services, foreign companies even benefited from tax exemptions on the introduction of imported supplies.Footnote 18

By 1930, the nationality of the largest foreign companies was becoming more diversified. The entry of U.S. companies increased, as did that of German and Belgian ones (Figure 2), all of them providing new goods and services. The entry of U.S. multinationals also responded to a global strategy aimed at strengthening their position in Latin America through direct investment. Some of these new companies (24/200) were controlled by the holding company American & Foreign Power, which acquired several Anglo-Argentinian and Argentinian electricity firms between 1927 and 1930 (Lanciotti, Reference Lanciotti, Jones and Lluch2015). As for Germany, the rapid technological development achieved by its industry facilitated the entry of German multinationals into Argentina's top business ranks in the electricity, import trade, telephony and radiotelegraphy sectors.

The predominance of British companies did not change in terms of the stock of capital investment and insertion in economic activities, as evidenced by their majority participation in the first ten positions of the rankings (Table 1). Nevertheless, the displacement of British hegemony in favour of the United States and the expansion of American multinationals in the world market gradually impacted Argentina's corporate leadership. This marked the beginning of the relative decline of the British presence in the country.

After WWI, leading Argentinian firms reorganised to take advantage of the new opportunities offered by an expanding domestic market. From 1913 to 1923, 58 per cent of the top companies had been founded or reorganised as corporations (or Sociedades Anónimas).Footnote 19 Many sole proprietorships and family firms organised themselves as corporations without resorting to public savings, public underwriting or stock exchange listing.Footnote 20 Most of these large companies maintained family ownership and management and self-financed through reinvestment of profits, contributions from the owners and their families, informal credit and short-term bank loans.

In 1923, the number of national companies among the 200 largest increased (Figure 1). Large national companies capitalised, increased their production scale, imported machinery and incorporated internal combustion engines and electric turbines in industrial plants to meet domestic demand and foreign markets in some sectors. Most of them were engaged in exploiting and marketing agricultural products and timber for export and agro-industrial production for the domestic market.

By 1930, a group of local companies (associated with business groups or stand-alone) was already consolidated at the apex of Argentina's capitalism. They were involved in mass consumption industries such as beer, sugar, wine, matches, sweets and tobacco, all locally produced, although sometimes marketed under foreign names/brands (Rocchi Reference Rocchi1998). Local companies also became crucial in the oil and mining activity (B) in the 1920s. This take-off resulted from the creation of the state oil company Yacimientos Petrolíferos Fiscales (YPF), not included in rankings due to its legal incorporation status. In 1930 there were already fifteen oil refineries operating in the country, three under state control. Foreign companies were also dynamic in this activity (Table 2). West India Oil Co., Standard Oil Co., Diadema Argentina SA de Petróleo and Shell Mex Argentina entered the 200 ranking in 1930.Footnote 21

Table 2. Sectorial distribution of the top 200 firms by nationality: Argentina, 1913-1944

Source: Base de datos de Grandes empresas en Argentina—BDGEA/BCAD (19131971) BID PICT 20153273.

We also note that in the first global period, until the Second World War, foreign firms dominated transport and storage (H), public utilities (D, E) and the exploitation of natural resources. These activities required high investment in fixed assets and were closely related to the technologies of the First Industrial Revolution.

3.2.1 From the great depression to the second world war

Despite increasing political risks in the global economy, Argentina did not introduce restrictive regulations on the entry of foreign capital.Footnote 22 It constituted a low-risk country for foreign companies, especially for European ones that sought to avoid confiscations and controls in their countries of origin, as in the German case, or the increase in tax pressure, as in the British case. Until the end of the Second World War, the security of investments in Argentina guaranteed acceptable returns and the preservation of assets, and the country became a safe destination for European companies affected by exchange rate devaluations, the European recession, and finally, the outbreak of the war.

In the world crisis of 1930, government policies to face external restrictions and the decline of the value of exportations gave new impetus to the industry. The state assumed an active role in the economy by introducing fiscal and monetary policies. After the exit from the gold standard regime, the currency was depreciated, import tariffs were raised, and exchange controls were established. To encourage local and foreign manufacturing companies, tariffs on fuels and raw materials were reduced (Phelps Reference Phelps1938, p. 204).

Exchange controls and the differential exchange rate for imports favoured the substitution of inputs and intermediate goods produced by national and foreign companies. Consequently, chemical, metallurgical and textile companies increased their share in the top 200. Among the local industrial firms, milling, sugar, wine and food companies continued to stand out. The entry of new companies into the 1937-1938 ranking was mainly associated with the growth of the textile and cement industries (Table 4). Other national firms such as Loma Negra and Maquinarias Di Tella expanded, starting a new generation of business groups. Those created during the first global economy, such as Bunge y Born, Tornquist, Bemberg and Italo (known as the Fabril group since 1930), deepened their diversification towards industrial activities in the 1930s.Footnote 23

Industrial growth also induced the entry of new foreign industrial firms into the corporate leaders, mainly from the United States. The growth of the woollen and cotton textile industry brought several American firms to the top 200 (Belini Reference Belini2017; Lluch Reference Lluch2019). Several of those investments were planned before the Great Depression and worsened economic conditions did not change the companies' plans. Based on previous commitments, 23 U.S. firms built factories or established their commercial branches in Argentina between 1931 and 1933 (Wilkins Reference Wilkins1974, p. 167; Lluch Reference Lluch2019).

German firms also increased their presence, especially in the metallurgical sector with Thyssen Lametal, Sociedad Electrometalúrgica Argentina (SEMA) and Tubos Mannesmann. The peak of German companies was reached in 1944-1945. After the German defeat in World War II, this presence declined. The adhesion of the Argentinian State to the Treaty of Chapultepec enabled the confiscation of thirty German firms under the title of enemy property, which was transferred to the National Directorate of State Industries (DiNIE) in 1947 (Belini Reference Belini2006).

In the 1930s, the number of foreign companies in the top 200 increased, but their practices changed, including the trend towards «Argentinisation.» For example, under the «transfer of business» category, Pan American Oil Export Co. (formerly Tide Water Oil Export Co.) transferred its business to Pan American, Compañía Argentina de Petróleo SA, in 1937. West India Oil Co. (a subsidiary of Standard Oil) transferred its business to the West India Oil Company, Sociedad Anónima Petrolera Argentina.Footnote 24 The strategy of changing their country of incorporation showed the adaptation to the new legal environments worldwide but, most importantly, attempted to elude taxes in their home countries. International Harvester (IH), the agricultural machinery manufacturer, did not change its legal status during the 1930s. Still, it evaluated the reorganisation and studied the advantages and disadvantages of maintaining its foreign status or forming a new Argentinian-incorporated company in a context where fiscal and political issues acquired greater significance.Footnote 25

The transformations described above did not have a linear impact on corporate leadership, where opposing trends converged. Even considering the more significant role of the industrial sector in the corporate elite after 1930 and the gradual displacement of British companies by U.S. companies, there is a remarkable continuity in the list of top companies from 1913 on. In 1944, 77 per cent of the leading companies had been created—or reorganised—before the 1930s.

Another element of continuity is that the relative decline of British investment did not change the fact that companies from this country continued to be the majority in the top 200 until the end of the second war. In 1944, British capital represented 40 per cent of the total capital of the 200 big firms, which is explained by its high investment in fixed assets during the first globalisation. Transport and public utility companies, mostly from Britain, continued to lead. Although the profitability of British railway and tramway companies declined due to competition with motor transport after 1930, economic growth continued to ensure satisfactory profits for financial, mortgage and utility companies (Lanciotti Reference Lanciotti2021).

To sum up, the sectoral distribution of the top 200 firms in 1913 demonstrates that the largest companies were concentrated in the agricultural sector (A), industry (C), transport and storage (H) and represented 64 per cent of the top 200. Other significant sectors were those of real estate (L) and export and import trade (G), both associated with the agricultural expansion. This structure was relatively stable until the 1930s, although national firms led the increase in the participation of industrial companies as of the 1920s (Table 3).

Table 3. Top 200 firms by activity, Argentina 1913-1971

Source: Base de datos de Grandes empresas en Argentina—BDGEA/BCAD (19131971) BID PICT 20153273.

From 1930 to 1944, the expansion of the domestic market gradually changed the sectoral distribution of the largest companies from activities associated with the production and marketing of raw materials, exploitation of natural resources and real estate companies (A, G and L) in favour of industrial activities (C) (see Table 2). Around 1944, the shift from agricultural (A) to industrial (C) activities marked the end of a cycle. This change is also detected, as in other countries, in the decline of transport and storage companies (H) and the real estate sector (L). On the other hand, large commercial companies (G) were quite unstable, and this was attributed to their high heterogeneity and the impact of external shocks on the Argentinian economy.

As Table 3 shows, the presence of large industrial companies (C) at the top started early and reached its peak in 1971, with 76 per cent of the total. As mentioned above, the importance of the industrial sector as a consequence of population growth and urban expansion driven by European immigration consolidated the domestic market. This trend converged with the increase in industry participation in Argentina's GDP, which became the highest in Latin America in the first post-war period (Belini Reference Belini2017, p. 67). In the 1930s, industry grew more due to the external restrictions imposed by the crisis. A decade later, government policies promoted industrialisation, as explained in the next section. However, we found that industrial firms represented the majority from 1913 onward.

3.3 The state-led industrialisation period

The end of Second World War constituted a turning point in Argentina's corporate leadership. The promotion of industry was the basis of the economic policies applied from 1943 to 1974, which materialised through customs protection, public credit, regulation of interest rates, multiple exchange rates, refunds to exports, sectoral and regional industries promotion schemes and purchases from national companies by the state.Footnote 26 This implied an expansion of the state's role and public management of companies in strategic activities. Decree 14630/44 granted incentives to a wide range of industries declared to be of national interest and its scope was deepened by Decree 3347/48. The National Commission for the Establishment of Industries was then created to promote the establishment of targeted industries and the automotive, machinery and implements industries were declared to be of «national interest.» (Altimir et al. Reference Altimir, Santamaría and Sourrouille1966, pp. 99-102; 114-118; Reference Altimir, Santamaría and Sourrouille1967, p. 363).

Systematic state intervention in the business sector began during the Peronist government (1946-1955). The nationalisation of the railway and public services companies determined the absolute decline of British investment in the country and the withdrawal of U.S. and British interests in public utilities. Nationalisations had a high impact because these companies had been at the top of the rankings since 1913.Footnote 27 Other measures, such as the nationalisation of foreign trade led by the creation of the Argentinian Institute for the Promotion of Exchange (IAPI, its acronym in Spanish)—which, in addition to monopolising the export of cereals and meat, controlled the import of supplies and machinery for agriculture and industry—the banking reform and the expansion of public credit for the industrial sector, implied the transfer of resources from the agricultural to the industrial sector.

These changes should not be read as a way to increase regulation affecting the activity of foreign firms since no contrary or discriminatory legislation towards these companies had been approved.Footnote 28 Instead, the government introduced customs, exchange and credit incentives that benefited certain foreign corporations. For example, in 1950, the requirement to include dividends in income tax returns was eliminated, which exempted shareholders of Argentinian and foreign companies. That same year, oil producers were exempted from the sales tax (Sánchez Román Reference Sánchez Román2013, pp. 132, 149).

The economic crisis of 1951-1952 encouraged the entry of additional foreign capital. A set of reforms assigned foreign capital a complementary role to national private investment and state investment in «industrial activities intensive in technologies not available in the country.» (Azpiazu and Kosacoff Reference Azpiazu and Kosacoff1985, p. 12). In 1953, the first legal regime for the establishment of foreign capital in Argentina was introduced. Law 14222 established that investments in the production of goods and services that save foreign exchange should be prioritised. The promotion of foreign investments deepened later, when the military dictatorship that overthrew Peronism in 1955 revoked Law 14222 and replaced it with more flexible regulations for the repatriation of profits (Decrees 13403 and 16640). There was no other comprehensive legislation until the new foreign investment law (Law 14780) was approved by the government of Arturo Frondizi (1958-1962), as we will see later (Altimir et al. Reference Altimir, Santamaría and Sourrouille1967; Belini Reference Belini2014).

The Peronist government also encouraged the creation of joint ventures to promote the local manufacture of agricultural machinery and automobiles as a response to the currency crisis provoked by the increase in imports of industrial inputs. Decree 14630/44 promoted the agreements between the state and German and Italian multinationals (such as Deutz, Hanomag, Mercedes Benz and Fiat) to manufacture motor vehicles and the association of the state company IAME with Kaiser Motors to create IKA (Industrias Kaiser Argentina). This policy implied the entry of new foreign direct investment and the increase of capital associations in the top 200.Footnote 29

The impulse to industrial production was also the result of the Peronist government's macroeconomic policies, which set maximum prices for exportable goods and introduced salary improvements that implied a substantial redistribution of income in favour of the working class and the subsequent expansion of the domestic market. Consequently, industrial activity grew simultaneously as a transition from the less capital-intensive industries to the most dynamic sectors.

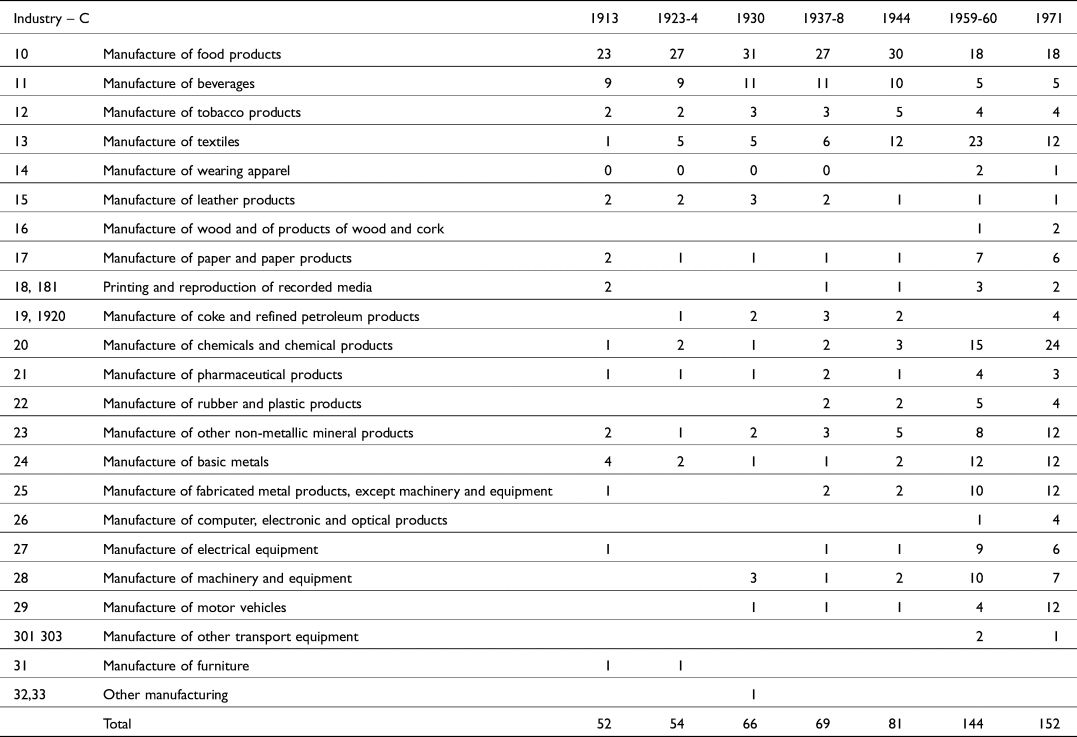

In fact, before Peron's government, large industrial companies were concentrated in the food, tobacco and textiles sectors (Table 4). The companies that produced sugar, wine, beer, flour and derivatives, and to a lesser extent, milk and derivatives and yerba mate were the majority from 1913 to 1944. They constituted a relatively enduring group within the 200 largest firms. As a result of government policies, which promoted the scale growth of the chemical (C20), metallurgical and machinery (C24, C25 and C28) industries, these industrial companies were strengthened in the 1950s (Table 4).

Table 4. Industrial firms by sector, Argentina 1913-1971

Source: Base de datos de Grandes empresas en Argentina—BDGEA/BCAD (19131971) BID PICT 20153273.

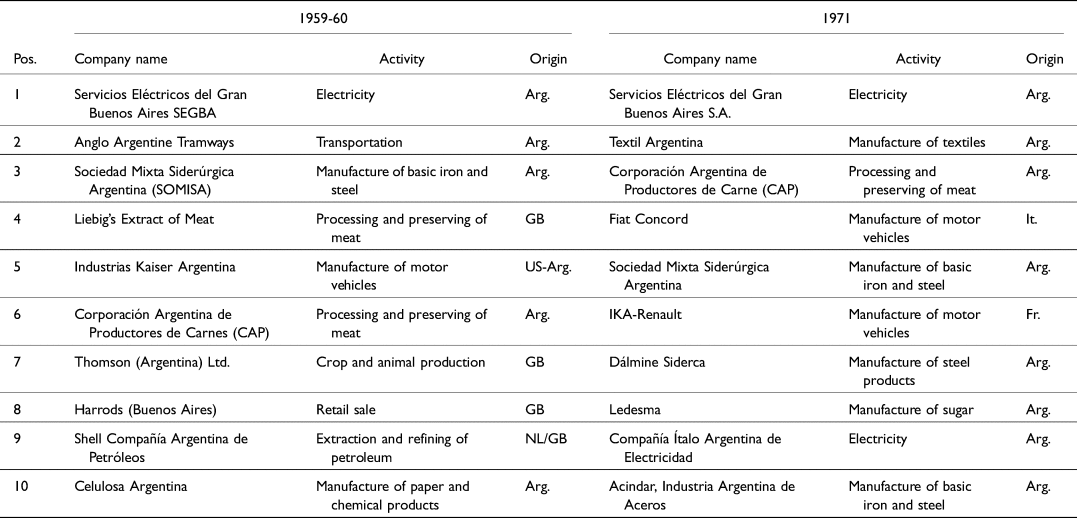

By 1960, the transformation of the largest corporations was evident. Firstly, a significant proportion of the top of the ranking was represented by new firms; 84 of the 200 companies were created after 1950. Secondly, industrial firms represented 72 per cent of these. In third place, as shown in Figure 1, Argentinian companies reached their highest participation, and 76 per cent of them carried out industrial activities. This resulted from the creation and expansion of national companies to provide consumer goods for the domestic market, both as supplies and capital goods, to reduce the external dependence on local industry.Footnote 30 Fourth, in 1960, a new cycle of foreign investment was led by U.S. multinationals, representing 13 per cent of the top 200 firms and 38 per cent of foreign firms. In that year's ranking, 85 per cent of the largest companies carried out industrial activities; the remaining 15 per cent were in the oil and mining sector. The changes in the top 200 indicate an industrial-based productive diversification in the steel, automotive, chemical and oil industries.

Among the largest locally-controlled companies, those oriented to the production of basic industrial inputs (production of steel and iron, cellulose, paper and chemicals) dominated, showing the impacts of the post-war industrial promotion policies. The presence of SOMISA (a joint venture created by the state in 1947), Acindar, Dálmine, TAMET, Compañía Química and Celulosa in the top positions confirms the impact of these new investments in strategic sectors of the economy (Table 5). This signalled a contrast with the most capitalised Argentinian firms of the 1944 ranking, primarily in the food, beverage and textile industries.

Table 5. Top 10 firms, Argentina: 1959, 1960 and 1971

Source: Base de datos de Grandes empresas en Argentina—BDGEA/BCAD (19131971) BID PICT 20153273.

In 1960, the companies controlled by the first generation of diversified business groups (Bunge and Born, Italo/Fabril) reached the highest positions. These firms maintained a dominant role in agricultural and industrial activities until the end of the period. In addition, companies associated with a new generation of groups driven by post-war industrial development, Dálmine Siderca (Techint); Siam Di Tella Automotores and Siambretta (Di Tella), entered the top 200.

Among the foreign firms, U.S. companies dominated the ranking for the first time (27 over 19 British), after the gradual penetration that began in the 1920s. Only six U.S. companies present in the 1960 ranking—mostly chemical and pharmaceutical companies—were created after 1944: Lepetit, Williams Química y Técnica, Pfizer Argentina, Monsanto Argentina, Dow Química Argentina and John Deere Argentina. This also marked the outset of a new cycle of FDI based on the exclusive competitive advantages of the U.S. multinationals, which produced chemicals, motor vehicles, machinery and equipment.

During the government of Arturo Frondizi (1958-1962), import substitution deepened. Coinciding with the new expansive wave of multinationals in the global economy, a new foreign investment law (Law 14780) was approved, whereby the limit on the remittance of profits and the repatriation of capital was eliminated. An investment guarantee law was also sanctioned to insure foreign investors against risks of exchange rate inconvertibility. Finally, different agreements on compensation amounts and terms of payment were signed with the expropriated foreign companies.Footnote 31

The Onganía government (1966-1970) reinforced the leadership of multinationals in the industrial sector. During this period, the foreign presence in the automotive sector increased through direct investment and shareholding in Argentinian companies of the auto parts sector. According to some estimates, this industry contributed more than 30 per cent of the increase in the manufacturing gross domestic product between 1958 and 1965, and its participation in the industrial product increased by 7 points (Heymann and Menéndez Reference Heymann and Menéndez1980, p. 34). The automotive branch absorbed 10.3 per cent of GDP in 1965, showing an annual growth rate of 24 per cent between 1958 and 1965 (Sourrouille Reference Sourrouille1976; Katz and Kosacoff Reference Katz and Kosacoff1989, p. 52). The presence of the multinationals Ford Motor, Bridgeport Argentina, Chrysler Fevre Argentina, General Motors Argentina, and Fate in the 1971 top 200 exemplifies this process. Some firms had already settled and others arrived in the country at this time. As for the firms of German origin, Mercedes Benz and Borgward and the producer of heavy trucks and agricultural machinery, DECA, all created in the 1950s, had joined in the ranking by this time.Footnote 32

The sectoral distribution showed the following trends: the percentage of industrial companies (C) increased even more around 1971. Their dominance was supported by some long-standing importers (G) and the leading firms in the oil sector (B). The remaining activities already had a sparse representation among the largest 200 in 1959 and 1971. Even the weight of primary activities (A) was reduced to a minimum, with only six firms in 1971 (Table 3 and Figure 3).

Figure 3. Main activities of the top 200 firms by nationality: Argentina, 1959-1971.

Source: Base de datos de Grandes empresas en Argentina—BDGEA/BCAD (19131971) BID PICT 20153273.

The displacement of the food industry in favour of the production of durable goods and inputs was strengthened. Although some sugar, meat and beverage companies remained at the top until 1971, they began to lose their positions. They were displaced by textile firms (C13) in 1959-1960, chemical-petrochemical (C20 and C19) and automotive (C29) companies in 1971 (Table 4). These firms expanded their facilities and diversified their production, leveraging on projects with state financial support and taking advantage of different promotional benefits.Footnote 33

Towards 1971, the number of national firms at the top decreased along with the entry of new foreign investment in the industry of durable consumer goods and industrial supplies for the Argentinian market (Figures 1 and 3). 46 per cent of the top foreign companies were set up after 1969. The entry of multinationals through brownfield and joint-venture strategies indicates the development of local industry in previous years and the interest of multinationals in accessing specific assets in peripheral countries that could expand their ownership advantages. The multinationals increased the scale of their investments (in many cases taking advantage of access to external credit and not through their assets), undertook the acquisition of national companies, and increased their shareholding in Argentinian companies.Footnote 34

Another clear trend in 1971 was that 5 per cent of the firms were joint ventures (JEs), 19 per cent were Argentinian companies controlled by business groups, while stand-alone national companies and foreign firms represented 30 per cent and 46 per cent, respectively. In this regard, the companies owned by the so-called new business groups by Barbero (Reference Barbero, Jones and Lluch2015), such as Garovaglio/Roberts and Pérez Companc, were strengthened in a closed and regulated economy (Barbero Reference Barbero, Jones and Lluch2015; Barbero and Lluch Reference Barbero, Lluch, Fernández and Lluch2016). These business groups benefited from industrial policies, credits from the National Development Bank (BANADE), and access to international loans with government guarantees. However, unlike the specialised insertion in machinery and steel that the Di Tella and Techint groups showed, at the end of the 1960s, the companies of the new business groups led a pattern of diversification into unrelated low-technological activities, such as sugar, cement, transport, metallurgy and chemistry. The diversified investment of the new groups contrasts notably with the insertion of foreign multinationals in the most dynamic sectors (machinery, automotive and petrochemical), all based on the technology of the Second Industrial Revolution.

As proposed in the introduction, the greatest share of foreign companies is detected in 1913 but also in 1971; i.e., at the peak of the first globalisation and the end of the second cycle of foreign investment in Argentina. If in 1913 foreign firms represented 40 per cent of the top 200 while joint ventures reached 10.5 per cent, by 1971, multinationals represented 46 per cent while joint ventures decreased to 5 per cent. The differential share of the joint ventures in both benchmark years responded to the different penetration strategies of foreign capital in each cycle. In both cases, these strategies were based on the alliance between the First and Second Industrial Revolutions' technologies, imported from Europe and the United States, respectively, and local market knowledge offered by local partners. Unlike the association during the first global economy, in 1971, joint investments took place through the shareholding of foreign multinationals in formerly locally-owned industrial companies.

4. Final remarks: the transformations of corporate leadership in Argentina

From a business history perspective, our analysis of the corporate elite corroborates that the Argentinian economy gradually evolved from an export economy based on the exportation of primary products to a more diversified economy, with a turning point in the first post-war period. In the second post-war phase, public policies led to the dominance of industrial activities until 1971.Footnote 35

Particularly pronounced in the first rankings, a persistent feature of the top 200 was the large size of the ten most prominent firms. In 1913, the top 10 concentrated 80 per cent of the total paid-up capital. Between 1923 and 1960, the top 10 alone agglutinated approximately half of the capital of the 200 largest firms. A different phenomenon is identified only in 1971, when the top 10 represented 35 per cent of the total. This would indicate that a very small handful of companies—mostly foreign—maintained a central role in Argentina's economy.

Considering the ownership and management of the largest companies, the analysis has confirmed the relevant presence of foreign multinationals throughout the period. In 1913 and 1971, the participation of foreign firms was high, 40 per cent and 46 per cent respectively. In addition, the dominance of British companies in the top positions until the second post-war period marks the endurance of the initial conditions of Argentina's insertion in the world economy. As shown, the gradual entry of U.S. companies displaced the British in the 1950s, but their dominance was never as pronounced as that of the British. In addition, and from the 1920s onward, we noted the growing participation of a group of national stand-alone firms and firms controlled by business groups as the result of an early process of economic diversification, with a strong bias towards industrial activity focused on the domestic market.

The sectoral insertion of Argentinian business groups and stand-alone companies illustrated the convergence of the activities carried out by national firms with the productive pattern delimited by foreign multinationals. In the first global economy, Argentinian firms were involved in agricultural production, export of primary goods and industrial production for the domestic market. In contrast, foreign firms dominated finance, import trade, transport, storage and public utilities. At the end of the state-led industrialisation period, multinationals consolidated their presence in dynamic industries as locally-owned firms were displaced from producing durable consumer goods and industrial supplies by foreign firms.

In addition, the analysis of the sectoral distribution by origin of the capital showed that large foreign firms tended to group together in activities with high technological intensity, for which local firms had not developed competitive advantages, especially during the first globalisation, when the high investment capital in fixed assets required by the infrastructure and public utility sectors was not available to local firms.

The techno-economic paradigm promoted by the top foreign firms changed in the interwar period, from investment in transportation and public services to industry. The analysis of the top firms also showed that, with the exception of electricity and oil, the technology of the Second Industrial Revolution arrived late in Argentina, in comparison with other late-industrialised countries, such as Australia or Italy. Similar to other large Latin American countries, such as Brazil or Mexico, the technology of the Second Industrial Revolution entered Argentina during the state-led industrialisation period.Footnote 36

The top foreign firms showed a more diversified investment in the first globalisation compared to the end of the period, when they were concentrated in the industrial sector. The priority sectors in the first cycle were transport, storage, infrastructure and public utilities. We can see that there is indeed a cluster in activities that required technological expertise and high financing, which is not very accessible to local firms. The decline of the British presence in transport was slower than in other countries, where it began after the first war, while in Argentina, this happened after the Second World War. The greater survival of the British firms observed during the first globalisation can be explained by the fact that they depended to a lesser extent on the evolution of their national markets and had also developed high investments in fixed assets.

The share of foreign firms in the industrial sector grew gradually and it was not until the 1959-1960 break that it crystallised into an even more concentrated pattern in industrial activity. Studies of industrial history have identified a trend towards concentration in the manufacturing sector with a greater variation between 1959 and 1963, coinciding with the establishment of foreign companies. Our analysis shows that most foreign companies formed a cluster around automotive and associated production (tires), then metallurgy and chemistry. This grouping seems to be associated with market capturing strategies in a context of high protectionism.

National companies showed a more diversified pattern of investment between 1913 and 1937. From then on, they experimented a tendency toward concentration in the industrial sector. In the first globalisation, the insertion of large Argentinian companies in the agricultural sector was more marked and continued until the second post-war period and their participation in export trade and the real estate sector. In the second post-war period, the presence of large agricultural companies fell sharply among the top 200. The insertion of local companies in the industrial sector was much earlier and more consistent than that observed in foreign companies. The food sector was predominant, except in 1960, when textiles dominated the ranking, although, by 1971, this situation had changed.

To sum up, our analysis has measured and shown for the first time in the literature that the share of foreign firms among the 200 largest firms in Argentina is much higher than that identified in other countries. In Australia, foreign firms constituted 31 per cent of the top 100 in 1910 and dropped to 9 per cent in 1952 (Fleming et al. Reference Fleming, Merrett and Ville2004, pp. 16-18). In Italy, for example, foreign multinationals represented 25.5 per cent of the top 200 in 1972, a slightly higher percentage than in 1913. The foreign share was 15 and 20 points higher in the Argentinian case in both cuts (Colli Reference Colli, Colli and Vasta2010). Also, this data confirms our second proposition regarding the long-lasting presence of business groups from 1913 to 1960, given that it fluctuated around 20 per cent. As we have pointed out, in 1923 and 1959-1960, there was greater participation of stand-alone national companies; they reached 46 per cent in 1923, remained between 33 and 37 per cent between 1930 and 1944, rose to 45 per cent in 1959-1960 and finally dropped to 30 per cent in 1971. The state policies of industrial promotion of the second post-war period could explain the greater share of Argentinian firms in 1959-1960; however, its effect seems to have been insufficient to face the new inflow of foreign capital and technology that weakened the presence of Argentinian companies in favour of multinationals around 1971. The described evolution shows that the structural conditions behind the expansion of foreign companies and business groups had a persistent impact on Argentina's capitalism.

Primary sources

• The Argentine Yearbook 1913. Buenos Aires: Robert Grant & Co.

• Guía de Sociedades Anónimas. Anuario 1923-1924. Buenos Aires: A. Dorr Mansilla, 1924.

• Guía de Sociedades Anónimas, responsabilidad limitada y cooperativas, 1930. Buenos Aires: A. Dorr Mansilla, 1931.

• Guía de Sociedades Anónimas, responsabilidad limitada y cooperativas, 1937-1938. Buenos Aires: A. Dorr Mansilla, 1938.

• Guía de Sociedades Anónimas 1944/45, responsabilidad limitada y cooperativas. Buenos Aires: A. Dorr Mansilla, 1946.

• Guía del accionista de sociedades anónimas 1959-1960. Buenos Aires: El Accionista, 1960.

• Guía de sociedades anónimas. Buenos Aires: Cámara de Sociedades Anónimas, 1972.

• Banco Central de la República Argentina, Circular B 1150, Buenos Aires, 4 de setiembre de 1974. Empresas industriales con participación del capital extranjero, 1974. Listado elaborado sobre la base de Basualdo Eduardo, «La estructura de propiedad del capital extranjero en la Argentina.» Centro de Economía Transnacional, 1974.

Acknowledgement

We want to thank the anonymous reviewers for their comments on the earlier version of this article. Thanks to colleagues who also commented on the paper at conferences and workshops. We also thank to the Agencia Nacional de Promoción Científica y Tecnológica for financing our research project. As always, any remaining errors are our own.