The definition of a bubble we take to be an undertaking which is blown up into an appearance of splendour and solidity, without any probability of permanence, and the name, we take it, is derived from the specious products of puffing and soapy water, with which the most of the ingenious youth of this realm have been long familiar.1

We have to turn the page on the bubble-and-bust mentality that created this mess.2

What is the difference between the great composer George Frideric Handel and Shane Filan, the lead singer of Irish boyband Westlife? To those of a musical bent, the answer is obvious: Handel is one of the most respected classical musicians of all time, having composed several famous operas. Filan, on the other hand, largely specialised in saccharine cover versions of 1970’s pop songs. The difference that interests us, however, is that while one lost all of their wealth in a bubble, the other got out before a bubble burst, making a handsome profit as a result.

By the time he was 30 years old, Handel’s musical compositions had already made him a very wealthy man, and his patron, Queen Anne, provided him with a considerable annual income. In 1715 he invested some of his wealth in five shares of the South Sea Company, which would have cost about £440. Handel sold his shares before the end of June 1719 for a profit of about £145 – just before the huge bubble in the company’s shares.3 By the time Shane Filan was 30, Westlife was one of the most successful pop groups of all time and the net worth of the group’s four members was over £32 million. Along with his brother, Filan decided to become a property developer in the midst of the Irish housing bubble. In order to purchase as much housing as possible, he supplemented his own funds by borrowing large sums of money from banks. In 2012 he was declared bankrupt, owing his creditors £18 million.

Shane Filan was not the only loser when the housing bubble collapsed. In Northern Ireland, where we both live, house prices more than trebled between 2002 and 2007; by 2012, they had collapsed to less than half their peak.4 We thus observed at close quarters the economic destruction that a bubble can wreak. Bubbles can encourage overinvestment, overemployment and overbuilding, which ends up being inefficient for both businesses and society.5 In other words, bubbles waste resources, as clearly illustrated by the half-built houses and ghost housing estates that stood across Ireland when the housing bubble burst. Other inefficiencies are in the realm of labour markets, as people train or retrain for a bubble industry. When the bubble bursts, they become unemployed and part of their investment in education has been wasted. After the collapse of the housing bubble, many of our friends, neighbours and students who had trained as architects, property developers, builders, plumbers and lawyers were either unemployed, in a new industry, or travelling overseas to find work.

The most severe economic effects usually occur when the bursting of a bubble reduces the value of collateral backing bank loans. This, coupled with the inability of bubble investors to repay loans, can result in a banking crisis. The collapse in house prices after 2007 was followed by the global financial crisis and we witnessed the downfall of American, British, Irish and other European banks. This resulted in major long-lasting damage to the economy. Financial crises are astonishingly economically destructive: estimates of the losses in economic output for post-1970 banking crises range from 15 to 25 per cent of annual GDP.6 These estimates, however, conceal the large costs that financial crises have on psychological and human well-being.7 They also ignore the human costs associated with the imposition of austerity measures once the crisis is over. We both experienced and witnessed cuts in real pay, decreased levels of public service provision and cuts in welfare payments to family members.

Not all bubbles, however, are as economically destructive as the housing bubble of the 2000s, and some may even have positive social consequences.8 There are at least three ways in which bubbles can be useful. First, the bubble may facilitate innovation and encourage more people to become entrepreneurs, which ultimately feeds into future economic growth.9 Second, the new technology developed by bubble companies may help stimulate future innovations, and bubble companies may themselves use the technology developed during the bubble to move into a different industry. Third, bubbles may provide capital for technological projects that would not be financed to the same extent in a fully efficient financial market. Many historical bubbles have been associated with transformative technologies, such as railways, bicycles, automobiles, fibre optics and the Internet. William Janeway, who was a highly successful venture capitalist during the Dot-Com Bubble, argues that several economically beneficial technologies would not have been developed without the assistance of bubbles.10

Why do we refer to a boom and bust in asset prices as a bubble? The word ‘bubble’, in its present spelling, appears to have originated with William Shakespeare at the beginning of the seventeenth century. In the famous ‘All the world’s a stage’ speech from his comedy As You Like It, he uses the word bubble as an adjective meaning fragile, empty or worthless, just like a soap bubble. Over the following century, ‘bubble’ was widely used as a verb, meaning ‘to deceive’. The application of the term to financial markets began in 1719 with writers such as Daniel Defoe and Jonathan Swift, who viewed many of the new companies being incorporated as not only worthless and empty, but deceptive.11 The bubble metaphor stuck, but over time its use has become somewhat less pejorative.

Nowadays the word ‘bubble’ is used by commentators and news media to describe any instance in which the price of an asset appears to be slightly too high. Among academic economists, however, using the word at all can be deeply controversial. One school of thought sees a bubble as a non-explanation of a financial phenomenon, a label applied only to episodes for which we have no better explanation.12 Eugene Fama, the father of modern empirical finance, goes further than this, calling the term ‘treacherous’ and complaining that ‘the word “bubble” drives me nuts’.13 In Fama’s view the word ‘bubble’ is devoid of meaning, having never been formally defined.14

In this book, we borrow the definition of Charles Kindleberger, the MIT economic historian and bubble scholar, who describes a bubble as an ‘upward price movement over an extended range that then implodes’. In other words, a bubble is a steep increase in the price of an asset such as a share over a period of time, followed by a steep decrease in its price.15 Others have suggested that, for an episode to constitute a bubble, prices must have become disconnected from the ‘fundamental value’ of the asset.16 However, this definition makes bubbles much more difficult to identify with any certainty, which can lead to lengthy discussions about whether a particular episode was a ‘real’ bubble or not. It is also divorced from the historical usage of the term. The beauty of Kindleberger’s definition for us is that, because the definition makes no claims about the underlying causes of bubbles, we can investigate these causes for ourselves. One implication of this definition is that a bubble can only be identified with 100 per cent certainty after the event. However, this does not mean that bubbles are wholly unpredictable and random events. In this book, we propose a new metaphor and analytical framework which describes their causes, explains what determines their consequences, and – we hope – will help predict them in the future.

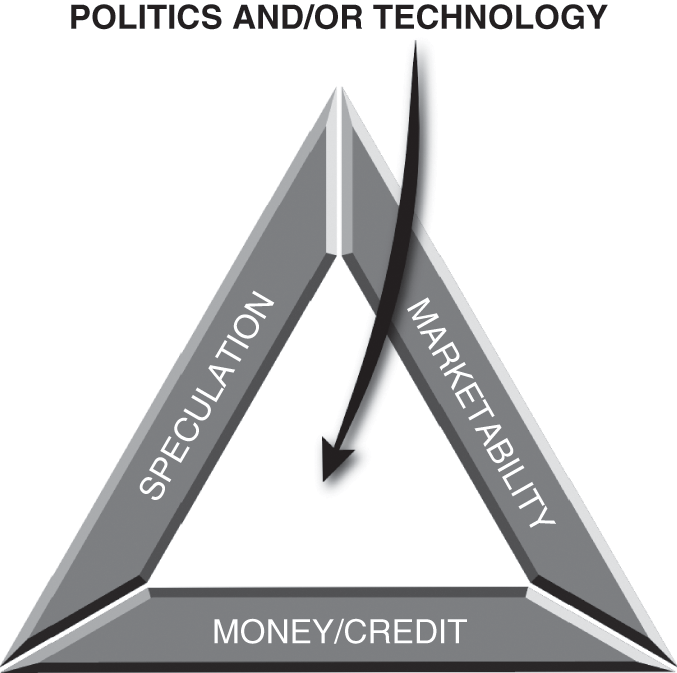

The Bubble Triangle

The starting point of our metaphor is to think of a financial bubble as a fire: tangible and destructive, self-perpetuating and difficult to control once it begins. While fires can cause serious damage, they can also be useful in certain ecosystems, contributing, for example, to the renewal of savannas, prairies and coniferous forests. The same is true of bubbles. Taking this metaphor further, the formation of a fire can be described in simple terms using the fire triangle, which consists of oxygen, fuel and heat. Given sufficient levels of these three components, a fire can be started by a simple spark. Once the fire has begun, it can then be extinguished by the removal of any one of the components. We propose that an analogous structure can be used to describe how bubbles are formed: the bubble triangle, summarised in Figure 1.1.

The first side of our bubble triangle, the oxygen for the boom, is marketability: the ease with which an asset can be freely bought and sold. Marketability has many dimensions. The legality of an asset fundamentally affects its marketability. Banning the trading of an asset does not always make it wholly unmarketable, as demonstrated by the abundance of black markets around the world. But it does usually make buying and selling it more difficult, and bubbles are often preceded by the legalisation of certain types of financial assets. Another factor is divisibility: if it is possible to buy only a small proportion of the asset, that makes it more marketable. Public companies, for example, are more marketable than houses, because it is possible to trade tiny proportions of the public company by buying and selling its shares. Bubbles sometimes follow financial innovations, such as mortgage-backed securities, that make previously indivisible assets – in this case, mortgage loans – divisible.

Another dimension of marketability is the ease of finding a buyer or seller. One of the least marketable investment assets is art, for example, because the pool of potential buyers is very small in comparison to assets like gold and government bonds. Bubbles are often characterised by increased participation in the market for the bubble asset, expanding the potential pool of buyers and sellers. Finally, it matters how easily the asset can be transported. Assets which can be transferred digitally can now be bought and sold multiple times a day without the buyer or seller leaving home, whereas more tangible assets like cars or books need to be moved to a new location. Some bubbles are made possible by financial innovations that allow transportable assets to be used in lieu of immobile ones – trading the deeds to a house, for example, instead of the house itself. Like oxygen, marketability is always present to some extent, and is essential for an economy to function. However, just as one would not keep oxygen tanks beside an open fire, there are times and places where too much marketability can be dangerous.17

The fuel for the bubble is money and credit. A bubble can form only when the public has sufficient capital to invest in the asset, and is therefore much more likely to occur when there is abundant money and credit in the economy. Low interest rates and loose credit conditions stimulate the growth of bubbles in two ways. First, the bubble assets themselves may be purchased with borrowed money, driving up their prices. Because banks are lending other people’s money and borrowers are borrowing other people’s money, neither are fully on the hook for losses if an investment in a bubble asset fails.18 The greater the expansion of bank lending, the greater the amount of funds available to invest in the bubble, and the higher the price of bubble assets will rise. When investors start selling their bubble assets in order to repay loans, the price of these assets is likely to collapse. Financial bubbles can thus be directly connected to banking crises.19

Second, low interest rates on traditionally safe assets, such as government debt or bank deposits, can push investors to ‘reach for yield’ by investing in risky assets instead. As a result, funds flow into riskier assets, where a bubble is much more likely to occur. The propensity of investors to reach for yield has a long history. Walter Bagehot, the famous editor of The Economist, observed in 1852 that ‘John Bull can stand a great deal, but he cannot stand two per cent … Instead of that dreadful event, they invest their careful savings in something impossible – a canal to Kamchatka, a railway to Watchet, a plan for animating the Dead Sea.’20 In Bagehot’s experience, investors would often rather invest in something ridiculous than accept a low interest rate on a safe asset.

The third side of our bubble triangle, analogous to heat, is speculation. Speculation is the purchase (or sale) of an asset with a view to selling (or repurchasing) the asset at a later date with the sole motivation of generating a capital gain.21 Speculation is always present to an extent; there are always some investors who buy assets in the expectation of future price increases. However, during bubbles, large numbers of novices become speculators, many of whom trade purely on momentum, buying when prices are rising and selling when prices are falling. Just as a fire produces its own heat once it starts, speculative investment is self-perpetuating: early speculators make large profits, attracting more speculative money, which in turn results in further price increases and higher returns to speculators. The amount of speculation required to start the process is only a small fraction of that which occurs at its peak.

Once a bubble is under way, professional speculators may purchase an asset they know to be overpriced, planning to re-sell the asset to ‘a greater fool’ to make a capital gain.22 This practice is commonly referred to as ‘riding the bubble’.23 However, it is often difficult to distinguish investors who rode the bubble from those who were lucky enough to sell at the right time. Speculation is also much more widespread when many investors have limited exposure to downside risk. This may be the case when defaulting on debts incurs few costs, when institutional investors are faced with poorly designed incentive structures or when bank owners have limited liability. In these circumstances, the prospect of buying a risky asset in the hope of short-term gains is much more appealing.

Of course, investors can also speculate ‘for the fall’: selling assets in the hope of buying them back later for a lower price. If the speculator does not own the asset, they can speculate for the fall by short selling: borrowing the asset, selling it, buying it back later for a lower price, then returning it to the lender. The short seller is hoping that the asset’s price will fall in the intervening period so that they can make a profit from the trade. In practice, however, short selling is often much more difficult and risky than simply buying an asset. When an investor buys a stock, the potential losses are limited, but the potential gains are unlimited; when an investor short sells a stock, the opposite is true. Short selling even the most clearly overvalued asset can thus completely ruin an investor if its price continues to rise. Often there are legal or regulatory restrictions on short selling, coupled with social opprobrium against short sellers. At other times it can be extremely expensive to borrow the asset in the first instance.24 In less regulated markets, short selling can leave investors exposed to market manipulators who engineer corners on the short-sold stock.25

What is the spark that sets the bubble fire ablaze? Economic models of bubbles struggle to explain when and why bubbles start – according to Vernon Smith, a Nobel Laureate, the sparks that initiate bubbles are a mystery.26 In this book, we argue that the spark can come from two sources: technological innovation, or government policy.

Technological innovation can spark a bubble by generating abnormal profits at firms that use the new technology, leading to large capital gains in their shares. These capital gains then attract the attention of momentum traders, who begin to buy shares in the firms because their price has risen. At this stage, many new companies that use (or purport to use) the new technology often go public to take advantage of the high valuations. While valuations may appear unreasonably high to experienced observers, they often persist for two reasons. First, the technology is new, and its economic impact is highly uncertain. This means that there is limited information with which to value the shares accurately. Second, excitement surrounding technology leads to high levels of media attention, drawing in further investors. This is often accompanied by the emergence of a ‘new era’ narrative, in which the world-changing magic of the new technology renders old valuation metrics obsolete, justifying very high prices.27

Alternatively, the spark can be provided by government policies that cause asset prices to rise.28 Usually, but not always, the rise in asset prices is engineered deliberately in the pursuit of a particular goal. This goal could be the enrichment of a politically important group, or of politicians themselves. It might be part of an attempt to reshape society in a way that the government deems desirable – several housing bubbles, for example, have been sparked by the desire of governments to increase levels of homeownership. The first major financial bubbles, described in Chapter 2, were engineered as part of elaborate schemes to reduce the public debt.

As well as creating the spark through their policy decisions, governments can pull other policy levers which affect one or more of the sides of the bubble triangle. For example, governments can lower interest rates or increase the money supply, thus ensuring that the public have sufficient funds to invest in the bubble. They may pursue financial deregulation, allowing banks to lend more money on less restrictive terms, thereby increasing the amount of credit. An extension of credit can allow more investors to buy into the bubble on leverage, encouraging them to engage in more speculation. Financial deregulation may also make it easier to buy and sell the assets involved in the bubble, increasing their marketability.

Why do bubbles end? One obvious reason is that they run out of fuel. There is a finite amount of money and credit to be invested in the bubble asset, and increases in the market interest rate or central bank tightening can cause the amount of credit to fall. This makes borrowing to invest in an asset more difficult for speculators, which can in turn trigger a sell-off in the bubble asset as investors look to raise capital. Alternatively, the tightening of credit markets can make it impossible for those who invested in the bubble with borrowed money to extend the duration of their loans, forcing them to sell the asset.

The number of speculators is also finite, and can eventually reach an upper limit. Speculators may be spooked and exit the market when new information arrives which changes their expectations about future prices. For example, a bubble might burst in response to news announcements suggesting that the future cash flows associated with the bubble assets will be lower than expected. Since speculative investors typically buy an asset because its price is rising, even a slight reversal can dramatically reduce the asset’s appeal. The effect of momentum trading is reversed: investors sell the asset because its price is falling, and the belief that prices will continue to fall becomes self-fulfilling.

Why do some bubbles cause widespread economic damage, whereas others have little effect on the macroeconomy? There are two important variables: the size of the bubble and its centrality within the wider economy. The most damaging bubbles are those where substantial wealth is invested in an asset that is deeply integrated with the rest of the economy. This integration may be in the form of supply chains; for example, the failure of a bubble company may also bankrupt its suppliers, who in turn default on payments to another firm. However, a more common route for the damage to spread is via the banking system. To extend the fire metaphor, banks are the equivalent of a combustible oil rig in the middle of a busy town. When banks fail, often as a result of the bank or its borrowers holding too much of a bubble asset, it can set off a chain of bankruptcies and defaults that destroys businesses, jobs and livelihoods. In the worst-case scenario, the failure of one bank exposes several others, with similarly devastating effects. Banks also tend to service a wide array of customers, many of whom would otherwise have no connection to the bubble. The exposure of banks to a crash can thus cause a regional or industry-specific bust to develop into an economy-wide recession.

In summary, our bubble triangle describes the necessary conditions for a bubble – marketability, money and credit, and speculation. They become sufficient conditions for a bubble only with the addition of a suitable technological or political spark. We believe the bubble triangle is a powerful framework for understanding why bubbles happen when they do, as well as their severity or societal usefulness. Since it describes the circumstances in which a bubble is likely to occur, it is also useful as a predictive tool. However, since the various elements of the framework cannot be reduced to a neat set of metrics, the application of the framework for predictive purposes requires the use of judgement.

The most long-standing existing explanation for bubbles is irrationality (or madness) on the part of individuals and concomitant mania on the part of society. One of the earliest expressions of this explanation came from Charles Mackay, a Scottish journalist and writer, who first published his Memoirs of Extraordinary Popular Delusions and the Madness of Crowds in 1841. This book has been so popular that it is still in print today. Mackay was a great storyteller, and his theory was supported by a series of colourful anecdotes that supposedly illustrated how insane societies could become. His tales covered witches, relics, the Crusades, fortune telling, pseudoscience, alchemy, hairstyles and even facial hair. Having demonstrated the near universality of madness, he then had chapters on the South Sea Bubble, the Mississippi Bubble, and the Dutch Tulipmania, all of which argued that bubbles occur because of the psychological failings of investors.

Mackay was not the first to associate bubbles with madness and irrationality. Sir Isaac Newton, one of the most brilliant and influential scientists in all of history, lost a fortune by investing in the South Sea Bubble. When questioned about his losses, he is reputed to have said ‘that he could not calculate the madness of the people’.29

This madness-of-crowds hypothesis has been refined and expanded by the likes of Kindleberger, John Kenneth Galbraith and, most recently, Nobel Laureate Robert Shiller.30 Shiller and other economists argue that bubbles can largely be explained by behavioural economics, with cognitive failings and psychological biases on the part of investors causing prices to rise beyond their objective value.31 A subset of investors, for example, may suffer from an overconfidence bias, whereby they overestimate the future performance of a company stock, or they may have a representativeness bias, whereby they incorrectly extrapolate from a series of good news announcements and overreact.32 Other investors may simply follow or emulate this subset of investors simply because of herd behaviour and naivety on their part.33

The view that bubbles are largely a product of irrationality has been contradicted by economists who, like Nobel Laureate Eugene Fama, believe investors to be rational and markets to be efficient.34 Much recent research on the subject has thus focused on establishing whether a particular bubble was ‘rational’ or not.35 This is unfortunate, because the rational/irrational framework is almost useless for understanding bubbles. Partly this is because the word ‘rational’ is so loosely defined that many common investor behaviours can be classed as either ‘rational’ or ‘irrational’, depending on the preferences of the economist.36 But more fundamentally, the framework is too reductive. Asset prices in a bubble are determined by the actions of a wide range of investors with different information, different worldviews and investment philosophies and different personalities. They often also face different incentives. Simply dividing these investors into categories labelled ‘rational’ and ‘irrational’ does not do justice to the complexity of the phenomenon, and as a result, we try to avoid these terms altogether.

Historical Bubbles

We approach the historical bubbles in this book as if we were fire scene investigators, sifting through the ashes of historical bubbles in an effort to understand their causes. We then attempt to use this knowledge to become like fire-safety advisers, devising policies which may prevent bubbles from happening or being socially destructive in the future. First, however, we need to decide which fires to investigate. We have two selection criteria. Consistent with our definition of a bubble, we are interested only in bubbles where there was a large rise and then fall in asset prices. How large is large? We require a rise in asset prices of at least 100 per cent over less than 3 years, followed by at least a 50 per cent collapse in prices over a 3-year period or less.37 For stock market bubbles, we do not require the entire market to have experienced a reversal; rather, the reversal may have taken place in specific sectors or industries.38 This set of criteria means that those bubbles included in our catalogue are major ones. However, it also means that we may have overlooked some bubbles simply because we or previous scholars have been unable to find and collate price data.

The second criterion is that the asset price reversal must have been accompanied by a promotional boom, with new companies or financial securities being floated on financial markets. This ensures that the bubbles we select are those which had an impact on the economy beyond the effects of the price reversal. One implication of this criterion is that we exclude bubbles in commodities or collectables, such as comics, beany babies and baseball cards. Real estate or property bubbles are excluded unless they were accompanied by bubbles in stocks or facilitated by the issuance of newly created financial securities.

Table 1.1 contains a list of the major historical bubbles which meet these criteria, and which are studied in detail in this book. This list is by no means exhaustive. However, there are at least five things about our bubble catalogue which are of note. First, our selection of bubbles extends from the birth of stock markets through to the present day. Second, our catalogue is global in scope, covering four continents and nine countries. Third, although Table 1.1 contains many famous bubbles, there are also some which are less well known: the first emerging market bubble of 1824–6; the Australian Land Boom, which burst in the 1890s; the British Bicycle Mania of the 1890s; and the Chinese bubbles in 2007 and 2015. Fourth, six of our twelve bubbles were followed by financial crises, and at least five were followed by severe economic downturns. Fifth, several of the bubbles listed in Table 1.1 were explicitly connected to the development of new technology – railways in the 1840s, bicycles in the 1890s, automobiles, radio, aeroplanes and electrification in the 1920s and the Internet and telecommunications in the 1990s.

| Bubble | Country | Years | Asset | Post-bubble financial crisis |

|---|---|---|---|---|

| Mississippi Bubble | France | 1719–20 | Mississippi Company stocks | No |

| South Sea Bubble | UK | 1719–20 | Company stocks (including stocks of the South Sea Company) | No |

| Windhandel Bubble | Netherlands | 1720 | Company stocks | No |

| First emerging market bubble | UK | 1824–6 | Company and mining stocks | Yes |

| Railway Mania | UK | 1844–6 | Railway stocks | Yes |

| Australian Land Boom | Australia | 1886–93 | Company stocks and real estate | Yes |

| Bicycle Mania | UK | 1895–8 | Stocks of bicycle companies | No |

| Roaring Twenties | USA | 1920–31 | Stocks of new technology companies | Yes |

| Japanese Bubble | Japan | 1985–92 | Company stocks and real estate | Yes |

| Dot-Com Bubble | USA | 1995–2001 | New technology stocks | No |

| Subprime Bubble | USA, UK, Ireland, Spain, | 2003–10 | Real estate and houses | Yes |

| Chinese bubbles | China | 2007, 2015 | Stocks | No |

Probably the most famous absentee from our study is the Dutch Tulipmania of 1636–7, which witnessed the rapid price appreciation of rare tulip bulbs in late 1636, followed by a 90 per cent depreciation in bulb prices in February 1637.39 This is excluded for the simple reason that the price reversal was exclusively confined to a thinly traded commodity, with no associated promotion boom and negligible economic impact.40 In other words, the Tulipmania was too unremarkable to merit inclusion. Although the wild fluctuations in price are striking, they are not unusual for markets in rare and unusual goods, particularly those predominantly used to signal status.41 In the case of the Tulipmania these fluctuations were compounded by legal ambiguity over the status of futures contracts, suggesting that the price movements may have had a somewhat mundane explanation.42

The infamy of the Tulipmania is largely the fault of Charles Mackay.43 Mackay painted the picture of a society overcome with collective insanity on the subject of tulips, where the value of some bulbs exceeded the value of luxury Amsterdam houses. He also stressed the universality of the trade, with the general populace of Amsterdam ‘investing’ in tulip bulbs at the various taverns dotted around the city. But Mackay’s work is unreliable. His sources are based on second-hand accounts, which are in turn based on contemporary pieces of propaganda criticising the trade in tulips.44 Very few of the claims Mackay makes can be substantiated. The popular narrative of the Tulipmania is thus largely fictional, ‘based almost solely on propaganda, cited as if it were fact’.45 Indeed, for several episodes in this book we can see a similar process of myth-making, whereby bubble anecdotes that were originally satire or propaganda are repeated years later as if they really happened.

Another notable set of absentees from our list are the property bubbles which occurred in Scandinavia in the 1980s and in South-East Asia in the 1990s.46 In both cases major credit booms had their roots in financial liberalisation, and in both cases the crash was followed by a banking crisis. Capital account liberalisation exacerbated the credit boom in South-East Asia, where substantial amounts of international capital flowed into the region, resulting in twin banking and currency crises.47 However, the only one of these housing bubbles that was accompanied by a major stock market boom was in Thailand. The scale of the Thai stock market bubble does not meet our criterion for inclusion, and there appears to have been no promotional boom.48

Having chosen our fires, how do we go about investigating them? A good place to start is usually the findings of previous investigators. We thus make extensive use of existing literature, much of which comes from fields far beyond history or economics.49 However, the memory of an event and the experience of an event are often very different, and we also want to understand the thoughts and actions of those who were on the scene at the time. We therefore also investigate the writings and speeches of contemporary journalists, politicians and commentators during each bubble. What were they saying while the fire was going on? Were they calling the fire brigade or fanning the flames? We do not want to focus exclusively on the powerful – we are also interested in so-called ordinary people who were caught up in the fire. Who suffered, and who, if anyone, benefited from it? Finally, as financial economists, we do not want our analyses to be purely descriptive – we want to be able to quantify the size of each fire and the scale of the damage it caused. For famous bubbles this was straightforward, but for lesser-known bubbles it involved painstakingly compiling our own data from old records in dusty archives. The overall result, we hope, is a comprehensive overview of the subject told over three centuries. Our story begins in 1720 with a seminal moment in financial history: the invention of the bubble.