16.1 Introduction

The East of England (EE) is considered the ‘bread basket’ of the UK thanks to its fertile flat lands producing a variety of high-yielding crops. Cereals, especially wheat and barley, are by far the most important crops covering almost half of the farmed area. Sugar beet is grown in rotation with cereals, with the region producing more than two thirds of England’s total sugar beet crop. Other prominent crops include carrots, potatoes, oilseed rape, fruit, salad crops and pulses. The region is also important for pig and poultry production. With all these productive farming activities, the region contributes more to the UK’s agricultural gross value added than any other in the UK, directly employing around 19,000 full-time equivalent farmers and workers (2013 farm structure data) and contributing £1.7 billion (about 1 per cent) to local Gross Value Added (GVA) in 2018. The contribution of the EE to domestic food security is therefore important. The majority of farms are capital intensive with an average size exceeding 100 ha and are mostly family or corporate driven. Farmers are mainly landowners and are highly market-oriented with high levels of specialization, investing heavily in seeds and chemicals.

The high-yielding and high-quality staple crops produced in EE are not only supplying the domestic food market but are also exported all over the world. In particular, the UK is a net exporter of wheat grains and flour to many countries in North Africa (e.g. Morocco, Algeria and Tunisia) and South Asia (e.g. Thailand and the Philippines), significantly contributing to global food security and safety, also thanks to the strong integration of the EE farming system into global supply chains and the high-quality standards.

Despite its strengths and global importance, this farming system is under considerable pressure from trade and policy realignment and environmental challenges, with Brexit, market volatility, the Covid-19 pandemic and climate change impacting on its long-term viability. In order to assess and ensure the sustainable continuation of the EE’s agricultural sector, it is important to understand its resilience to internal and external shocks and to investigate the coping strategies and responding capacity of its various operators, starting from the perspective of farmers as the primary producers on which the farming system is based.

This chapter provides a full description of the EE farming system in terms of its challenges, functions, resilience and future strategies, which were elaborated during the SURE-Farm project and are summarized in Annex 16.1. It uses results of a mixed-method research approach based on a quantitative survey, semi-structured interviews and narratives to analyse the challenges faced by the farming system and the risk management and coping strategies adopted by farmers and other actors. In doing so, the chapter distinguishes between strategies that can lead to the robustness, adaptability or transformation of the farming system (see Chapter 1). In addition, the chapter investigates in detail the important role of knowledge networks and farmer learning for the development of resilience strategies. Key policy lessons derived from the SURE-Farm project are then summarized in the concluding section of the chapter.

Figure 16.1 A crop of rape in the East of England.

16.2 Risks, Challenges and Their Management

In order to understand what challenges, coping strategies and type of resilience are prevalent in the EE farming sector, a large-scale survey was conducted in November–December 2018. Survey data were collected through telephone interviews for a sample of 200 arable farms located in the EE counties, namely: Bedfordshire, Hertfordshire, Essex, Cambridgeshire, Norfolk and Suffolk. The sample was stratified to ensure representativeness in terms of the geographical distribution of farms and farm size. In what follows, the results of the survey are analysed in combination with the results of semi-structured farmer interviews conducted to investigate the role of farmer learning for risk management and biographical narratives conducted to explore family farm histories (Coopmans et al., Reference Coopmans, Draganova and Fowler2019; Urquhart et al., Reference Urquhart, Accatino and Appel2019; Nicholas et al., Reference Nicholas, Fowler and Midmore2020).

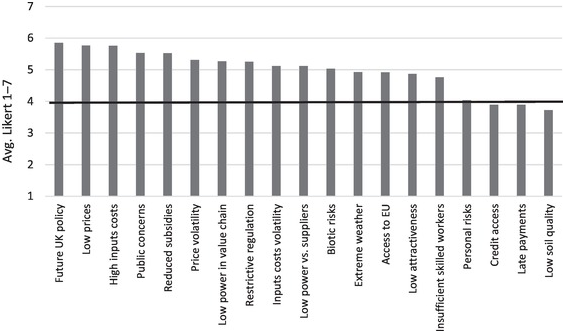

Figure 16.2 shows the survey results in terms of the challenges projected to face EE agriculture over the next twenty years. Farmers answers were recorded on a Likert scale from 1 (not at all challenging) to 7 (very challenging), where a value of 4 indicated neutrality. As one can see, the most worrisome challenges for EE farmers are uncertainty about the future of agricultural policy in the UK, persistently low market prices and persistently high input prices (e.g. fertilizer, feed, seed).

Figure 16.2 Challenges of the EE farming system over the next twenty years as perceived by farmers.

Many of the higher-ranking challenges are related to regulations and to the UK’s exit from the EU, the impacts of which are still largely unknown. The UK agricultural policy is currently being developed, with a new Environmental Land Management Scheme (ELMS) at its core based on the principle of ‘public money for public goods’. Currently farmers are uncertain as to what this will mean in practice, but they are concerned about a reduction in direct payments (i.e. the Basic Farm Payment, BPS), access to EU markets, competition from new markets (such as the USA) and a reduction in skilled farm workers (many of which come from other EU countries). All of these elements have potentially critical impacts in terms of how the EE farming system will look in the next twenty years.

Farmers also shared concerns about policies and regulations beyond Brexit. A progressive reduction of direct subsidies is planned under the EU’s Common Agricultural Policy, therefore EE farmers would have faced this challenge regardless of Brexit. According to interview results, the BPS is viewed as being crucial to making a profit most years and essential for paying interest due on the substantial bank loans secured against farmland. Moreover, farmers consider some regulations overly restrictive and inflexible. For example, the current crop protection regulations are perceived as a risk in terms of enabling or constraining what products a farmer can use, and thus what crops are viable to grow. The recent ban on neonicotinoids was seen by farmers as a barrier to growing oilseed rape and sugar beet, because of dramatically reducing yields.

A second key challenge is related to markets. On the one hand, some of the market challenges are linked to inputs and output prices and their volatility. This is not surprising given the intensive nature of the EE farming system that relies on inputs, with key products such as wheat globally traded. On the other hand, there are key challenges in the supply chain, especially in terms of imbalanced market power and the limited bargaining capacity farmers have with buyers and suppliers, that are often multinational holdings with large global market shares.

Weather was also cited as a major risk by the survey respondents. Although interview respondents feel that the climate is becoming slightly warmer, it is the extremes of cold (severe winters), heat (summer droughts) and severe storms and flooding that are difficult to manage. The EE is particularly prone to spells of dry weather during the summer months.

The lack of appeal of farming as a profession is an important challenge for the future of the EE farming system, as shown in Figure 16.2. Many farms’ employees are approaching retirement age but working on a farm might not be an attractive career choice for many young people today, as they do not like the unsociable hours it requires. Therefore, there are concerns about succession of farms and how to replace the retiring and experienced farm workers.

Narratives collected from nine EE farmers at different career stages (three each of early, mid- and late career) explored the key turning points in their family farming histories, what drove those turning points and the response to them (Nicholas et al., Reference Nicholas, Fowler and Midmore2020). Internal factors such as death, illness and intergenerational change were identified as being the greatest challenges to family farm business sustainability, with external factors (e.g. Figure 16.2) such as extreme weather events, price fluctuations and policy changes being viewed as something that they had to deal with in the day-to-day running of their businesses.

EE’s farmers adopt a variety of strategies to cope with the aforementioned challenges and risks (see Chapter 2). These strategies are reported in Table 16.1. The most frequently adopted strategy consists in implementing measures to prevent pests or diseases. Arable farmers have to deal mainly with black rust (Puccinia graminis), blackgrass (Alopecurus myosuroides), the cabbage stem flea beetle (Psylliodes chrysocephalus), small mammals (rabbits) and birds (e.g. pigeons), which eat and damage crops.

Table 16.1. Frequency of adoption of different types of risk management and coping strategies of EE farmers

| On-farm risk management strategies | % adoption | |

|---|---|---|

| Measures to prevent pests or diseases | 88 | |

| Market information to plan my farm activities for the next season | 84 | |

| Worked harder to secure production in hard times | 83 | |

| Flexibility in the timing of my production to deal with seasonality | 73 | |

| Invested in technologies to control environmental risks | 72 | |

| Diversified in other activities [e.g. agri-tourism, renewable energies] | 72 | |

| Maintained financial savings for hard times | 70 | |

| Low debts or no debts at all to prevent financial risks | 70 | |

| Cost flexibility [e.g. temporal labour contracts instead of permanent contracts] | 61 | |

| Diversified in production [e.g. mixed livestock and crop farming] | 56 | |

| Had an off-farm job [either myself or a family member] | 33 | |

| Opened up my farm to the public [e.g. open farm days] | 16 | |

| Off-farm risk management strategies | ||

| Learned about challenges [e.g. from a consultant or agricultural training] | 70 | |

| Had access to a variety of input suppliers | 68 | |

| Member of a producer organization, cooperative or credit union | 65 | |

| Hedged production with futures contracts | 58 | |

| Used production or marketing contracts | 57 | |

| Cooperated with other farmers to secure inputs or production | 55 | |

| Bought any type of agricultural insurance | 39 | |

| Member of an organization [e.g. collaborate with processors, retailers] | 36 | |

| Insurances | ||

| Field crop insurance [e.g. hailstorms, flood, drought] | 24 | |

| Grain in store insurance [e.g. fire, flood of storage] | 18 | |

| Income/price insurance [e.g. volatile prices, drop in income] | 8 | |

| Other type of insurance | 7 | |

Having updated market information is also a key strategy, especially with respect to wheat which is traded on the global market and subject to the volatility of global wheat prices. Therefore, farmers must manage these fluctuations and endeavour to sell their grain when prices are high and exchange rates favourable, keeping a check on global markets and events that may impact on grain prices for the coming season (e.g. droughts in key grain growing areas of the world). Forward contracts are an important tool to manage global market risks. As emerged from the interviews, in EE 70 per cent of the grain is sold up to two years in advance, which helps with budgeting and cash flow. Against low prices, there is also the possibility to store the harvest to sell when prices are highest.

The interviewed farmers explain that the adoption of innovation and technological developments are opportunities for reducing labour costs and improving the efficiency of input use. Regarding climate change, having machinery capacity available (even via contractors) can help overcome climate variability to a certain extent. For example, operations such as harvesting that used to take a week can be done in a day or two now, reducing the negative effects of bad weather.

Regarding Brexit, farmers are adopting two main strategies: some are holding back on further investments in the farm until they have a clearer picture of what the future of British farming will look like, while others are investing in expensive machinery now while they still have the BPS.

With respect to intergenerational transfer, there is evidence (e.g. Zagata and Sutherland, Reference Zagata and Sutherland2015) that policies for installing young farmers and pensioning off others later on in their careers has only very weak impact on facilitating intergenerational transfer. The narratives work within the SURE-Farm project indicated that other factors, mostly taxation and welfare, have a more significant impact. Here is a need for greater advisory support for succession planning if the risks associated with this challenging period are to be reduced.

During the survey, farmers were also asked to provide a self-assessment of their farms’ resilience, based on how much they agree with the statements in Table 16.2 on a Likert scale from 1 (strongly disagree) to 7 (strongly agree). On average, the survey’s results suggest that EE farmers perceived themselves to be adaptable to challenges. This is mainly due to their personal capacity of being good at adapting and the possibility of adopting new practices and technologies in response to shocks. On the contrary, their perceived level of robustness is relatively lower mainly due to difficulties in bouncing back to a pre-shock state. In other words, EE farmers feel that they could adapt and eventually transform as a reaction to a shock, which implies certain degrees of change, but they would not be able to withstand a shock without taking measures that can lead to a change, suggesting a certain level of vulnerability of their current status. From interviews and narratives conducted with farmers, it emerged that, predominantly, it was shocks such as disease outbreak or fire which resulted in higher transformations of their farm businesses.

Table 16.2. Farmers’ perceived resilience of their farm (1 ‘strongly disagree’ to 7 ‘strongly agree’)

| Robustness | Average | |

|---|---|---|

| After a shock, it is easy for my farm to bounce back to its current profitability | 4.20 | |

| It is hard to manage my farm in such a way that it recovers quickly from shocks | 4.18 | |

| I find it easy to get back to normal after a setback | 4.28 | |

| A big shock will not heavily affect my farm, as I have enough options to deal with shocks | 4.17 | |

| Robustness Avg. | 4.21 | |

| Adaptability | ||

| My farm can adopt new activities, varieties or technologies in response to shocks | 4.61 | |

| As a farmer, I can easily adapt myself to challenging situations | 4.94 | |

| I am good at adapting myself and facing up to agricultural challenges | 5.01 | |

| My farm is not flexible and can hardly be adjusted to deal with a changing environment | 3.28 | |

| Adaptability Avg. | 4.46 | |

| Transformability | ||

| For me, it is easy to make decisions that result in a transformation | 4.52 | |

| It is hard to reorganize my farm if external circumstances drastically change | 3.97 | |

| I still have the ability to radically reorganize my farm after a challenging period | 4.43 | |

| I can easily make major changes that would transform my farm | 4.17 | |

| Transformability Avg. | 4.27 | |

Finally, the current Covid-19 pandemic is an important challenge for the overall UK food system, and its impact on the resilience of the EE arable farming system was investigated through semi-structured interviews with different stakeholders in June–July 2020 (Meuwissen et al., Reference Meuwissen, Feindt and Spiegel2021). From the resilience perspective, Covid-19 has highlighted a problem in that many farms are specialized into providing for either the food service industry or retail, making them less adaptable and resilient to external shocks. The farming system revealed its fragility with this pandemic, partly due to the dominance of too few food distributors with long food supply chains in the retail and food service sectors. Moreover, while supply contracts between farmers and buyers provide stability and robustness in normal times, they may limit the flexibility for farmers to find alternative markets for produce if the need arises, revealing a weak adaptability of the food supply chain.

Overall, the Covid-19 crisis is having a relatively small impact on the EE arable sector. However, some critical situations have been identified. For example, the potato supply chain was badly hit due to the closure of restaurants, pubs and fish and chip shops. Similarly, the closing of pubs and restaurants strongly reduced the demand for beer and, therefore, for malting barley, which raised issues for storing greater amounts of the cereal. The increased demand for flour in supermarkets resulted in temporary shortages because the supply chain needed to redirect the bulk flour to retailers in a packet format. Specialized horticulture farms suffered from labour shortages during the picking season as most pickers are migrant workers from Eastern Europe who were unable to travel to the UK. Moreover, the interruption of several business activities provoked slight delays with machinery parts.

Some actors of the farming system have been able to develop successful responses and coping strategies against the risks of the pandemic. For example, the businesses who maintained diversity in their markets were better able to adapt and the more entrepreneurial have been able to switch quickly and take advantage of the increased retail demand. Vegetable growers were the most rapid in redirecting from the food service sector to supermarkets and farm shops. Potato growers have shifted from chipping to bulk bags for consumers. However, such a shift was not always possible as not all potato varieties are suitable for retail, and stored potatoes treated with two applications of chlorpropham cannot be sold as fresh potatoes. Longer-term impacts include changes in potato contracts for the next year as a surplus from this year’s harvest is expected, prompting growers to change to growing supermarket varieties.

16.3 Knowledge Networks and Learning

Within the EE arable farming system, the various operators do not act in isolation; on the contrary the farming system is composed of networks enhancing the sharing of resources, knowledge and experience, leading to mutual learning processes between actors. As a result, the farming system can effectively take advantage of collaborations and knowledge sharing in dealing with challenges and risks in a more efficient way than dealing with these issues individually.

While the farmer, or the farm manager, can be considered the central decision-maker of the business, the strategies to be resilient against shocks involve a number of actors participating in the wider farming system. First of all, the decision of adopting certain strategies and the intensity of changes needed to ensure that the farming business can overcome shocks depends on several factors, such as the farmer’s/manager’s perception and attitude towards risks, managerial skills and farm tenure (whether the farmer owns or rents land can affect attitudes and decision-making). Secondly, bankers, lenders, funders and business advisors can influence farmers strategies providing the financial means for investments and advising considering the farms’ history and characteristics (Soriano et al., Reference Soriano, Bardají and Bertolozzi2020). Moreover, traders provide market information and data sharing services which are critical for timely decision-making; cooperatives can contribute through collaboration, resource sharing and group-buying; collaboration with neighbours can involve machinery and land sharing, more land to farm, greater labour flexibility and reduced machinery costs; agronomists can provide advice and information on new crop varieties, crop trials, disease monitoring, biosecurity and crop rotation; research institutes can provide training, education and skills to support farming and diversification activities and may also be able to facilitate funding or collaborate on grant applications.

Our analysis revealed that, in most cases, the farms are family farms with several family members having a role in the farm management, so decision-making is shared. Hence, the most important influencers for the farmers interviewed were family members, who help develop confidence and provide support and joint decision-making. Agronomists were also influential, and their role has evolved from advice on plant protection products to broader knowledge of the agri-environmental scheme landscape. Financial advisors were also considered important, as was learning from other farmers. Other individual influencers identified were business partners, employees, landowners and contractors.

Different types of organizations can also significantly influence the managerial behaviour of farmers. For instance, public research organizations were considered influential, although respondents felt that there was a lack of government-funded research. Seed companies and brokers were moderately influential, and government departments were either perceived as highly influential (as they provide the boundaries within which farmers operate) or moderately influential. Some respondents indicated that supermarkets, environmental non-governmental organizations (NGOs), the National Farmers’ Union (NFU), buying groups, the Agriculture and Horticulture Development Board (AHDB), the farming press and social media are somewhat influential.

Networks and learning were also investigated through the survey and Table 16.3 reports results about the farmers’ self-assessment about their networking and learning capacity, measured on a Likert scale from 1 (strongly disagree) to 7 (strongly agree). As one can see, on average EE farmers have a relatively high level of networking (values >5), in particular between each other by developing farmer-to-farmer networks, but also with agricultural experts and value chain operators. Farmers feel a relatively high level of support from these networks, especially from neighbouring farmers.

Table 16.3. Farmers’ self-assessment of networking and learning (1 ‘strongly disagree’ to 7 ‘strongly agree’)

| Networking | Average | |

|---|---|---|

| I know a lot of other farmers in my region | 5.55 | |

| I know a lot of agricultural professionals, experts or value chain actors | 5.39 | |

| I feel I can receive support from agricultural network | 5.34 | |

| Farmers in my region tend to support each other when there is a problem | 5.30 | |

| Concerning farming, I often interact with neighbouring farmers | 5.29 | |

| When I attend agricultural events and meetings, I interact a lot with participants | 5.16 | |

| Learning | ||

| Before making a change on my farm I seek out as much information as possible | 5.86 | |

| I get a lot of information and ideas from talking to others in the sector | 5.40 | |

| I learn a lot from observing what other farmers do on their farms | 5.10 | |

| Over the years, my beliefs about how I should farm have changed | 5.02 | |

| My most important source of information is my own past experience of farming | 4.42 | |

| I am wary of new ideas and technologies in farming | 3.89 | |

| I am too busy to find out about how I might improve my farm | 3.28 | |

| I don’t reflect much on whether I can improve the way I manage my farm | 3.22 | |

| I learn a lot from other farmers via social media | 2.84 | |

The great importance of networks and collaboration across the farming system emerged during the current Covid-19 pandemic. As illustrated by farmer interviews, during the pandemic farms faced labour shortages and have advertised picking jobs. A big recruitment campaign started in EE, driven by individual companies but also by the NFU, the Country Land and Business Association (CLA) and the Department for Environment, Food and Rural Affairs (Defra). Initiatives such as ‘Pick for Britain’ by the government and ‘Student Land Army’ also started and social media has been used heavily for recruitment. As a result, those farms located nearer to urban centres had a good response, although those in more remote rural locations did not benefit as much because of difficulties in travelling to the farm and potential issues of accommodation.

Learning from peers and others in their network is a key strategy for EE farmers. Table 16.3 indicates that learning involves talking to farming neighbours, engaging in discussion groups, observing what other farmers are doing and seeking out advice from other farmers. This is particularly useful when farmers want to try out something new and engage in trials. Overall, farmers in the EE are more likely to seek as much information as possible before making changes on the farm. However, it is worth noting that social media does not seem to have a significant role in farmer learning, although a number of farmers explained that they find it useful for networking with farmers from other countries in terms of finding out about agricultural practices and innovations elsewhere that may have potential benefits to their own operations.

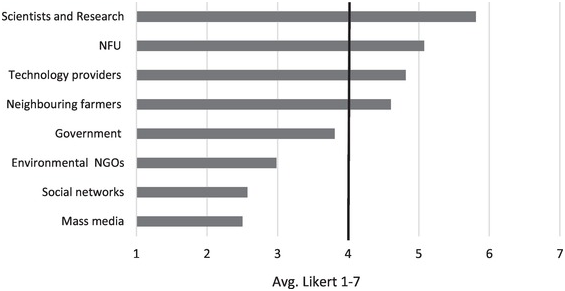

Finally, an important aspect driving learning is the degree to which farmers trust their sources. This is depicted in Figure 16.3, showing the average response of the farmers to the question ‘What sources of information can be trusted?’ during the survey (from 1 ‘do not trust at all’ to 7 ‘strongly trust’). Scientists, the NFU, technology providers and neighbouring farmers tend to be trusted more than politicians, environmental NGOs and the social and mass media.

Figure 16.3 Farmers perception of trust in different sources of information.

16.4 Conclusions and Lessons Learnt

From the analysis reported in this chapter, a number of important lessons have been learnt that can be useful for policymakers and stakeholders and that can inform future research. Firstly, the importance of policy and political changes as a source of uncertainty for farmers and actors of the farming system emerged. One could think that these challenges should be less worrisome than market and climate risks as they are under the responsibility of political institutions working for the benefit and not the disruption of economic activities. But our data showed a different picture, as Brexit, for example, became a long-term shock provoking uncertainty for the last four years which farmers have struggled to cope with. On top of this, the trade agreement to exit the EU market arrived with only a few days of notice but such critical policy changes should allow longer transition periods in which institutional support systems encourage more protracted incremental adaptation.

Second, strategies at the individual farm level can indicate the survival of single businesses, but the most effective solutions for both the resilience of the individual farm and of the farming sector are those that rely on the support of networks and collaborations, especially between farms that share similar goals. For example, peer-to-peer learning strategies proved to be important and effective in the EE arable sector, therefore these strategies could be more intensively promoted at the institutional level. Acting as a system inclusive of a variety of operators, the farming sector has more chances of long-term viability, therefore policy-makers could design solutions considering the relationships and power dynamics between actors instead of the interests of single groups. The role of farm advisors in this could be pivotal as they might have a wider perspective of the farming system.

From a broader perspective, the research conducted under the SURE-Farm project demonstrated how difficult it is to study the resilience of farming systems, in particular because of the difficulty in operationalizing the concept of resilience, which is inherently multidimensional, spanning the characteristics of farmers and associated actors, the sources and causality of shocks and the heterogeneity of effects. It is even more difficult to operationalize the resilience capacities of robustness, adaptability and transformability as their boundaries overlap – for example, there is a spectrum of successively stronger responses to drivers of change from robustness to transformation, and their application is relative to specific contexts. The narratives work also identified frequent small-scale changes, more significant than robustness but not enough to be characterized as adaptation of the farming system, but that cumulate eventually in a much broader overall change. This is an unexplored part of the resilience spectrum, and could be described as incremental change or ‘creeping change’.

The SURE-Farm project demonstrated the value of a resilience framework, and the mixed methods approach taken in the project allowed assessing the EE’s overall resilience. The case study showed low to moderate resilience capacities, with higher adaptability at the farm level and higher robustness at the system level. The Covid-19 pandemic highlighted how much resilience thinking is needed in order to react to crises, which points to a need to look beyond the farm and position the farm in a wider system perspective, such as the farming or the food system.

Open access

Open access