Fish is important for human health – fish consumption is associated with a decreased risk of CVD and dementia(1–Reference Xun, Qin and Song3), and nutrients in fish, including n-3 fatty acids, play an important role in cognitive development and immune regulation(Reference Assisi, Banzi and Buonocore4,Reference Kumar, Chandan and Gupta5) . Fish is also a valuable contributor to the reference nutrient intakes for a range of micronutrients, including vitamins D and B12, Fe, Se, Zn and Ca, and therefore, fish consumption may contribute to alleviating prevalent micronutrient deficiencies, especially in developing countries(Reference De Roos, Roos and Ara6,Reference Bogard, Farook and Marks7) . Furthermore, fish is considered an important element of more sustainable diets(Reference Willett, Rockström and Loken8). Greenhouse gas emissions linked to fish consumption are significantly lower than those linked to consumption of red meat and pork(Reference MacLeod, Hasan and Robb9,Reference Golden, Koehn and Shepon10) .

Despite the country being a significant fish producer and having food-based dietary guidelines for fish, consumption in the UK is low and has not changed in the past decades(Reference Stewart, Piernas and Cook11). Per-person weekly seafood consumption in the UK in 2019, at home and away from home, was 152·8 g, marking a 3·9 percent decrease compared with 2 years prior(12), and translating to just over one portion of fish, or 140 g, per person per week. This decline in UK seafood purchases has been primarily attributed to a 25 percent reduction in retail purchases over the past decade, resulting in approximately $7·7 billion lost in retail seafood sales(12). Previous demand analysis in the UK suggested that the quantity of fish demanded by consumers determines retail prices rather than the other way around(Reference Burton13). Also, retail demand for fourteen relevant UK fish products, measured between 1992 and 2001, indicated that haddock, salmon, flatfish, shellfish and smoked fish were expenditure elastic, whilst most of the fourteen species were own-price inelastic, indicating that the percentage change in quantity demanded increases or falls by less than the percentage change in price. This means that demand for these five fish species is decreasing if household expenditure or household income is decreasing, whilst price changes have less of an impact on demand(Reference Fousekis and Revell14). Another study(Reference Jaffry and Brown15) found that all canned tuna products had negative and inelastic price elasticities, again suggesting that demand remains relatively unaffected by price changes.

In a departure from the previous studies, we set out to compare fish demand patterns across different household groups in Great Britain, as household structure plays a significant role in shaping dietary choices. Studies in high-income countries consistently show how household composition, including factors like the presence of children and the life stage of family members, influences food consumption, reflecting diverse family needs and preferences. Moreover, variations in resources (household budget and time) and food expenditure relative to household composition affect food availability at home(Reference Groth, Fagt and Brøndsted16–Reference Rodrigues, Monteiro and Cunha18). We also set out to decompose changes in consumer demand for fish from 2013 to 2021 into income, relative price and change in taste and seasonality. This would allow us to identify specific drivers of demand changes for different fish product groups since changes in demand frequently arise from simultaneous shifts in commodity prices, total expenditure, tastes and seasonal influences(Reference Nelson19–Reference Rathnayaka, Selvanathan and Selvanathan22). Analysing the responses of fish demand to changes in prices and income is paramount when assessing how technological advancements, infrastructure development or economic policies could shape the future landscape of fish production, consumption and trade across diverse fisheries and aquaculture products. Furthermore, understanding fish demand across various fish product categories can highlight which are most promising for capturing expanded market shares or for interventions that could enhance fish consumption and therefore public health outcomes.

Methodology

Data

The data used for our analysis were drawn from the Kantar Worldpanel dataset, containing weekly acquisition data of food and drink purchases for consumption at home for 12 492 Great Britain households, covering the period January 2013 to December 2021 (the dataset does not cover Northern Ireland). Participating households were asked to record all purchases using barcode scanners and send digital images of cash register receipts. The till receipts were used to provide information on prices and place of purchase. The Kantar dataset contains information on purchases, including price, quantity purchased, the supermarket from which the product was purchased and the type of promotion used.

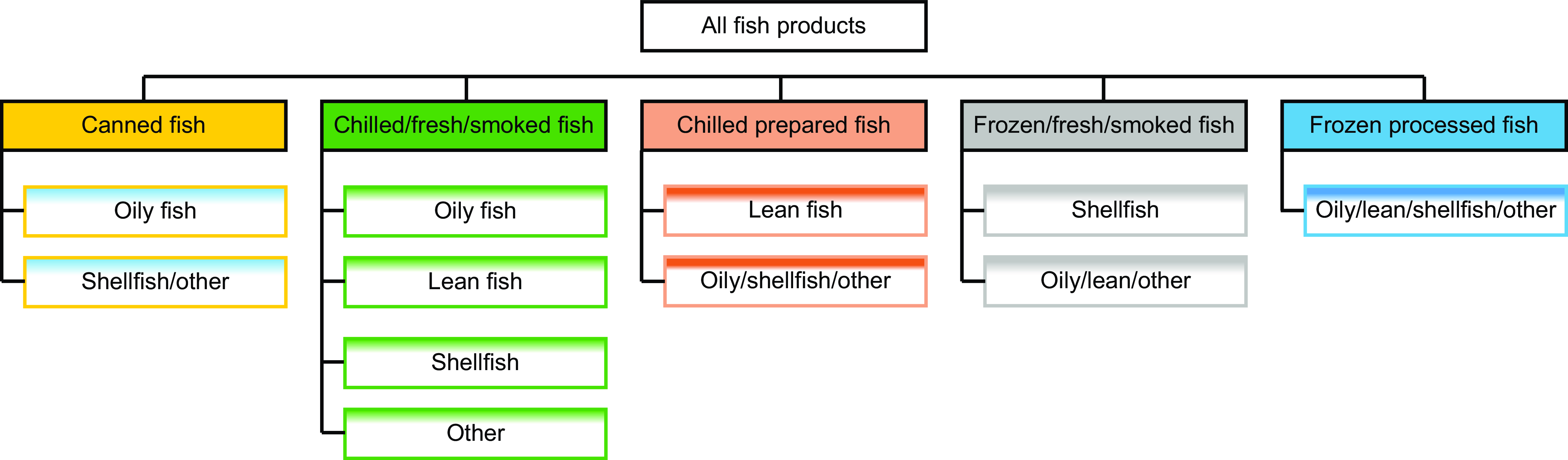

For our time series analysis, we aggregated the weekly data into ‘statistical months’, each comprising 4-week periods, resulting in 13 periods per year, or 117 total observations over the study period. This aggregation was conducted at the population level for each of the seven Kantar-predefined household groups(23), allowing us to examine aggregate consumption and expenditure patterns for each group over time. We systematically categorised all fish products into five main categories: canned fish, chilled or fresh smoked fish, chilled prepared fish, frozen fresh or smoked and frozen processed. Each category was further subdivided into four distinct groups: oily fish products, lean fish products, shellfish products and other fish products, resulting in a total of twenty fish subgroups. Subgroups were aggregated to accommodate zero consumption levels, ultimately arriving at eleven distinct fish and seafood groups (Figure 1). Moreover, based on classification by Kantar, seven household groups were considered: pre-family (< 45 years, no children), young family (any age, children aged 0–4 years), middle family (any age, children aged 5–9 years), older family (any age, children aged 10+), older dependents (age 45+ years, no children, 3+ adults), empty nest (age 45–65 years, no children, 1–2 adults) and retired (age 65+ years, no children, 1–2 adults). The basis for this classification was the age of the household wife and the number of adults and children in the family.

Figure 1. Categorisation of fish products into five main and twenty subgroups. Subgroups were aggregated to accommodate zero consumption levels, resulting in eleven distinct fish subgroups.

Model specification

In this study, we opted for the Rotterdam demand model(Reference Barten24,Reference Theil25) because it aligns with demand theory(Reference Theil26), exhibits excellent aggregate properties(Reference Selvanathan27), can be interpreted as approximations to the true unknown ones(Reference Mountain28) and is characterised by simplicity, making it easy to estimate and interpret parameter values. This model also permits the incorporation of external factors influencing demand, either with or without imposing theoretical constraints(Reference Clements and Gao29). Given the presence of autocorrelation in time series data, employing a differential model is advantageous for mitigating this issue and enhancing the robustness of parameter estimation and interpretation.

Considering the basic specification of the Rotterdam demand model, i th equation of our estimated model is given by

$$\eqalign {{\bar w_{it}}dln{q_{it}} & = {\alpha _i} + \;{\theta _i}dln{Q_t} + \mathop \sum \nolimits_{j = 1}^n {\pi _{ij}}dln{p_{jt}} + \mathop \sum \nolimits_{k = 1}^{12} {\beta _{ik}}{D_k} + {\varepsilon _{it}}\cr & \ \ \ \ i,j = 1,2, \ldots, n}$$

$$\eqalign {{\bar w_{it}}dln{q_{it}} & = {\alpha _i} + \;{\theta _i}dln{Q_t} + \mathop \sum \nolimits_{j = 1}^n {\pi _{ij}}dln{p_{jt}} + \mathop \sum \nolimits_{k = 1}^{12} {\beta _{ik}}{D_k} + {\varepsilon _{it}}\cr & \ \ \ \ i,j = 1,2, \ldots, n}$$

In equation (1)

${\bar w_{it}}$

is the arithmetic average of the budget shares in period t and t-1,

${\bar w_{it}}$

is the arithmetic average of the budget shares in period t and t-1,

${p_i}$

and

${p_i}$

and

${q_i}$

, are the price and the quantity, respectively,

${q_i}$

, are the price and the quantity, respectively,

$dln{p_{it}}\;$

and

$dln{p_{it}}\;$

and

$dln{q_{it}}$

are the time rates of change of p and q, and

$dln{q_{it}}$

are the time rates of change of p and q, and

$dln{Q_t} = \mathop \sum \nolimits_{i = 1}^n {\bar w_{it}}dln{q_{it}}$

is the Divisia volume index of the aggregate quantity demanded.

$dln{Q_t} = \mathop \sum \nolimits_{i = 1}^n {\bar w_{it}}dln{q_{it}}$

is the Divisia volume index of the aggregate quantity demanded.

${D_k}$

represents a seasonal dummy variable included to capture monthly effects, with twelve dummies accounting for seasonality in the thirteen statistical months per year. The parameter satisfies the constraint

${D_k}$

represents a seasonal dummy variable included to capture monthly effects, with twelve dummies accounting for seasonality in the thirteen statistical months per year. The parameter satisfies the constraint

$\;\mathop \sum \nolimits_{j = 1}^n {\beta _{ik}} = 0$

.

$\;\mathop \sum \nolimits_{j = 1}^n {\beta _{ik}} = 0$

.

${\alpha _i}$

is the constant term of the i

th demand equation satisfying the adding up restriction

${\alpha _i}$

is the constant term of the i

th demand equation satisfying the adding up restriction

$\mathop \sum \nolimits_{i = 1}^n {\alpha _i} = 0$

. The use of the constant term in the demand equations is to take into account any trend-like changes in tastes, etc. The parameter

$\mathop \sum \nolimits_{i = 1}^n {\alpha _i} = 0$

. The use of the constant term in the demand equations is to take into account any trend-like changes in tastes, etc. The parameter

${\theta _i}\;$

is the marginal share which satisfies

${\theta _i}\;$

is the marginal share which satisfies

$\mathop \sum \nolimits_i {\theta _i} = 1$

. This marginal share

$\mathop \sum \nolimits_i {\theta _i} = 1$

. This marginal share

${\theta _i}$

answers the question, ‘‘if income increases by one dollar, how much of this increase will be allocated to commodity i?’’ The

${\theta _i}$

answers the question, ‘‘if income increases by one dollar, how much of this increase will be allocated to commodity i?’’ The

${\pi _{ij}}$

are the price coefficients in (1), which satisfies the adding-up restrictions

${\pi _{ij}}$

are the price coefficients in (1), which satisfies the adding-up restrictions

$\mathop \sum \nolimits_{i = 1}^n {\pi _{ij}} = 0$

.

$\mathop \sum \nolimits_{i = 1}^n {\pi _{ij}} = 0$

.

These price coefficients also satisfy the following constraints:

$$\mathop \sum \nolimits_{j = 1}^n {\pi _{ij}} = 0\,\,\ \ \ \ \ \ \ i = 1,2, \ldots, n$$

$$\mathop \sum \nolimits_{j = 1}^n {\pi _{ij}} = 0\,\,\ \ \ \ \ \ \ i = 1,2, \ldots, n$$

The above equation (2) reflects the homogeneity property of the demand system, which postulates that an equi-proportionate change in all prices does not affect the demand for any good under the condition that real income is constant.

The price coefficients are symmetric, that is:

$${\pi _{ij}} = {\pi _{ji}}\;\ \ \ \ \ \ \ i,j = 1,2, \ldots, n$$

$${\pi _{ij}} = {\pi _{ji}}\;\ \ \ \ \ \ \ i,j = 1,2, \ldots, n$$

This means that an increase in the price of any good j will cause an increase in the compensated quantity demanded of i equal to the increase in the compensated quantity demanded of j caused by an increase in the price of i. Also, the Slutsky matrix

$[{\pi _{ij}}]$

is symmetric and negative semi-definite with rank (n-1).

$[{\pi _{ij}}]$

is symmetric and negative semi-definite with rank (n-1).

The term

${\varepsilon _{ij}}$

is the disturbance term of the i

th equation. It is assumed that the disturbance terms, ε

it

, i =1,…,n, are serially independent and normally distributed with zero means and with a contemporaneous covariance matrix. The income (total expenditure) elasticity implied by the demand system in equation (1) is given by

${\varepsilon _{ij}}$

is the disturbance term of the i

th equation. It is assumed that the disturbance terms, ε

it

, i =1,…,n, are serially independent and normally distributed with zero means and with a contemporaneous covariance matrix. The income (total expenditure) elasticity implied by the demand system in equation (1) is given by

$${\eta _{it}} = {{{\theta _i}} \over {{{\bar w}_{it}}}}$$

$${\eta _{it}} = {{{\theta _i}} \over {{{\bar w}_{it}}}}$$

The compensated price elasticities associated with equation (1) are given by

$${\eta _{ijt}} = {{{\pi _{ij}}} \over {{{\bar w}_{it}}}}$$

$${\eta _{ijt}} = {{{\pi _{ij}}} \over {{{\bar w}_{it}}}}$$

The uncompensated price elasticities are given by:

$${\eta _{ijt}} = {{{\pi _{ij}}} \over {{{\bar w}_{it}}}}{\bar w_{jt}}{{{\theta _{it}}} \over {{{\bar w}_{it}}}}$$

$${\eta _{ijt}} = {{{\pi _{ij}}} \over {{{\bar w}_{it}}}}{\bar w_{jt}}{{{\theta _{it}}} \over {{{\bar w}_{it}}}}$$

In equations (4), (5) and (6),

${{{\bar w}_{it}}}$

represents the arithmetic average of the budget shares in period t and t − 1 as aforementioned. As previously defined in the Rotterdam model specification, this term reflects the average share of expenditure allocated to the specific fish category under analysis. Although elasticity estimates are useful for measuring how consumer demand shifts in response to income and price changes, it is also important to understand the level of contribution of income and prices to consumption changes. Following the previous studies in the literature(Reference Nelson19,Reference Rathnayaka, Selvanathan and Selvanathan21,Reference Rathnayaka, Selvanathan and Selvanathan22) , we used the estimation results for demand elasticities to decompose the growth in fish demand in terms of autonomous trend, effects of income, own-price and cross-price and seasonal effects.

${{{\bar w}_{it}}}$

represents the arithmetic average of the budget shares in period t and t − 1 as aforementioned. As previously defined in the Rotterdam model specification, this term reflects the average share of expenditure allocated to the specific fish category under analysis. Although elasticity estimates are useful for measuring how consumer demand shifts in response to income and price changes, it is also important to understand the level of contribution of income and prices to consumption changes. Following the previous studies in the literature(Reference Nelson19,Reference Rathnayaka, Selvanathan and Selvanathan21,Reference Rathnayaka, Selvanathan and Selvanathan22) , we used the estimation results for demand elasticities to decompose the growth in fish demand in terms of autonomous trend, effects of income, own-price and cross-price and seasonal effects.

Dividing both sides of the demand system in equation (1) by the budget share

${\bar w_{it}}$

gives

${\bar w_{it}}$

gives

$$dln{q_i} = \alpha _{it}^* + \;{\eta _i}dln{Q_t} + {\eta _{ii}}dln{p_{it}} + \mathop \sum \nolimits_{j = 1}^n {\eta _{ij}}dln{p_{jt}} $$$$+ \mathop \sum \nolimits_k^{12} \;\beta _{ik}^*{D_k} + \varepsilon _{it}^* i $$$= 1, \ldots, n;t = 1, \ldots .,T$

$$dln{q_i} = \alpha _{it}^* + \;{\eta _i}dln{Q_t} + {\eta _{ii}}dln{p_{it}} + \mathop \sum \nolimits_{j = 1}^n {\eta _{ij}}dln{p_{jt}} $$$$+ \mathop \sum \nolimits_k^{12} \;\beta _{ik}^*{D_k} + \varepsilon _{it}^* i $$$= 1, \ldots, n;t = 1, \ldots .,T$

where

$\alpha _{it}^* = {\alpha _i}/{\bar w_{it}}$

is the autonomous trend in consumption of item i, which measures the proportionate change in consumption of food item i in year t in the absence of changes in prices and income. The constant terms in differential demand systems represent trends, and the coefficients of seasonal dummies represent seasonal deviations from these trends(Reference Fousekis and Revell30). Therefore,

$\alpha _{it}^* = {\alpha _i}/{\bar w_{it}}$

is the autonomous trend in consumption of item i, which measures the proportionate change in consumption of food item i in year t in the absence of changes in prices and income. The constant terms in differential demand systems represent trends, and the coefficients of seasonal dummies represent seasonal deviations from these trends(Reference Fousekis and Revell30). Therefore,

$\alpha _{it}^*$

is generally interpreted as a trend effect due to the effect of changes in tastes and preferences. The coefficients

$\alpha _{it}^*$

is generally interpreted as a trend effect due to the effect of changes in tastes and preferences. The coefficients

${\eta _i}$

and

${\eta _i}$

and

${\eta _{ij}}$

are expenditure and price elasticities. Therefore, growth in consumption of item i

${\eta _{ij}}$

are expenditure and price elasticities. Therefore, growth in consumption of item i

$\left( {dln{q_i}} \right)\;$

in each year can be decomposed into the following six components: (1) autonomous trend component (

$\left( {dln{q_i}} \right)\;$

in each year can be decomposed into the following six components: (1) autonomous trend component (

$\alpha _{it}^*)$

, (2) income component

$\alpha _{it}^*)$

, (2) income component

$\;\left( {{\eta _i}dln{Q_t}} \right)$

, (3) Own-price component

$\;\left( {{\eta _i}dln{Q_t}} \right)$

, (3) Own-price component

$\;\left( {{\eta _{ii}}dln{p_{it}}} \right)$

, (4) cross-price component

$\;\left( {{\eta _{ii}}dln{p_{it}}} \right)$

, (4) cross-price component

$\;\left( {\mathop \sum \nolimits_{j = 1}^n {\eta _{ij}}dln{p_{jt}}\;} \right)$

, (5) seasonal component (

$\;\left( {\mathop \sum \nolimits_{j = 1}^n {\eta _{ij}}dln{p_{jt}}\;} \right)$

, (5) seasonal component (

$\mathop \sum \nolimits_k^{12} \;\beta _{ik}^*{D_k})$

and (6) residual component

$\mathop \sum \nolimits_k^{12} \;\beta _{ik}^*{D_k})$

and (6) residual component

$\left( {\varepsilon _{it}^*} \right)$

.

$\left( {\varepsilon _{it}^*} \right)$

.

Estimation approach and separability assumptions

Before estimating demand equations, we examined the stationarity of all variables in the demand systems to prevent spurious results. While first-differencing the data generally mitigates non-stationarity, we conducted the Augmented Dickey-Fuller unit root test(Reference Dickey and Fuller31) as a precautionary measure given the extended time period covered in our analysis, which may include underlying trends. The test confirmed that all variables used in the demand systems were stationary*. We estimated separate demand systems for each of the above-mentioned seven household categories. This allowed us to capture the unique consumption patterns and preferences of different household types, leading to the calculation of distinct elasticities for each group. We subsequently assessed the homogeneity and symmetry of the demand theory hypotheses to ascertain their compatibility with the data. We used the sample size-corrected statistic(Reference Court32,Reference Deaton33) (Appendix 1A) to test homogeneity and Slutsky symmetry. This statistical measure has been widely applied in empirical studies, as evidenced by various works in the literature(Reference Chambers34–Reference Selvanathan, Jayasinghe and Selvanathan36). According to the test results (Appendix 1B), we can infer that all the household groups, homogeneity and Slutsky symmetry at the 5 % significance level are consistent with the data. Therefore, the homogeneity and symmetry-restricted version of the Rotterdam demand equation (1) was estimated using the seemingly unrelated regression for each household group.

To clarify our assumptions regarding separability, we applied a multi-stage budgeting approach. This approach allows us to treat fish products as a distinct, separable category within the broader food expenditure group. We further decomposed demand into various types of fish products within this category, such as canned, fresh and frozen fish. The separability assumption implies that consumers first decide on an allocation of their budget to food and, within that, specifically to fish. The expenditure on fish is then allocated across different types of fish products without assuming additional separability between individual fish subgroups. This ensures that our demand elasticities are conditional on the initial budgetary decision to allocate expenditure to fish, providing a more precise understanding of substitution effects within the fish category.Footnote *

Results

Fish consumption patterns

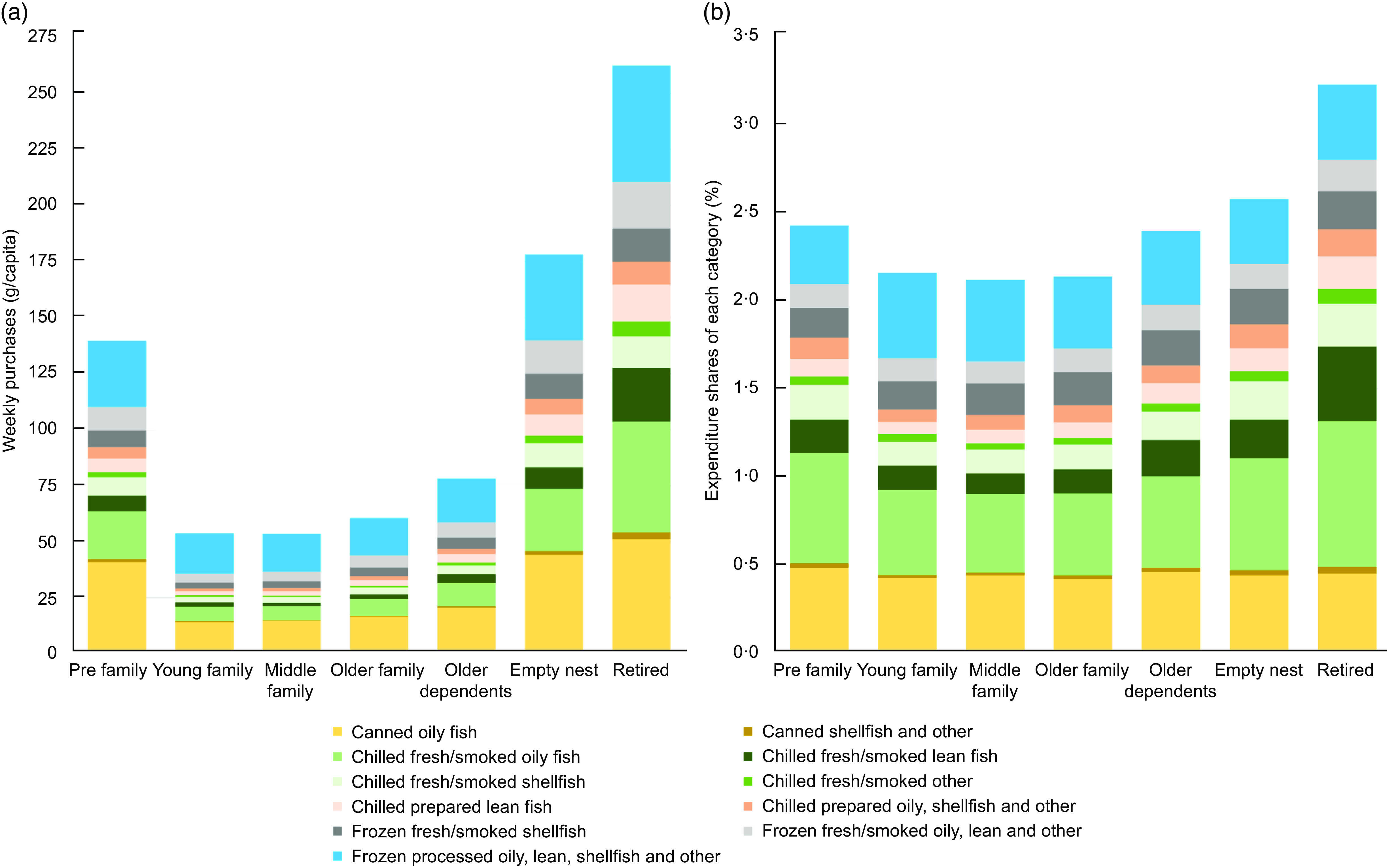

Analysis of weekly fish purchasing behaviours highlighted distinct patterns among British consumers, notably with the highest mean values observed in the empty nest (178 g/capita) and retired groups (262 g/capita) (Figure 2(a)). Moreover, those in the empty nest and retired groups purchased more chilled fresh/smoked oily fish, indicating a desire for higher-quality, less processed fish options. Conversely, young and middle family categories purchased lower quantities of fish (54 g/capita), indicative of a much lower fish consumption. Among families with children, canned fish and frozen processed fish products were more popular than other fish groups. However, the popularity of canned oily fish, such as tuna or mackerel, was apparent across various household groups.

Figure 2. Analysis of weekly fish purchases (a) and expenditure shares (b) for each of the eleven fish subgroups.

Retired households allocated the highest percentage of their grocery expenditure to fish purchases (3·23 %). Families with children consistently allocated a lower percentage of their total grocery expenditure to fish purchases, ranging from 2·12 % to 2·16 %. In contrast, households without children tended to allocate a slightly higher percentage on fish purchases, ranging from 2·40 % to 3·23 % (Figure 2(b)). Expenditure shares for canned oily fish and frozen processed fish items ranked second only to chilled fresh/smoked oily fish among the eleven fish categories.

Demand elasticities

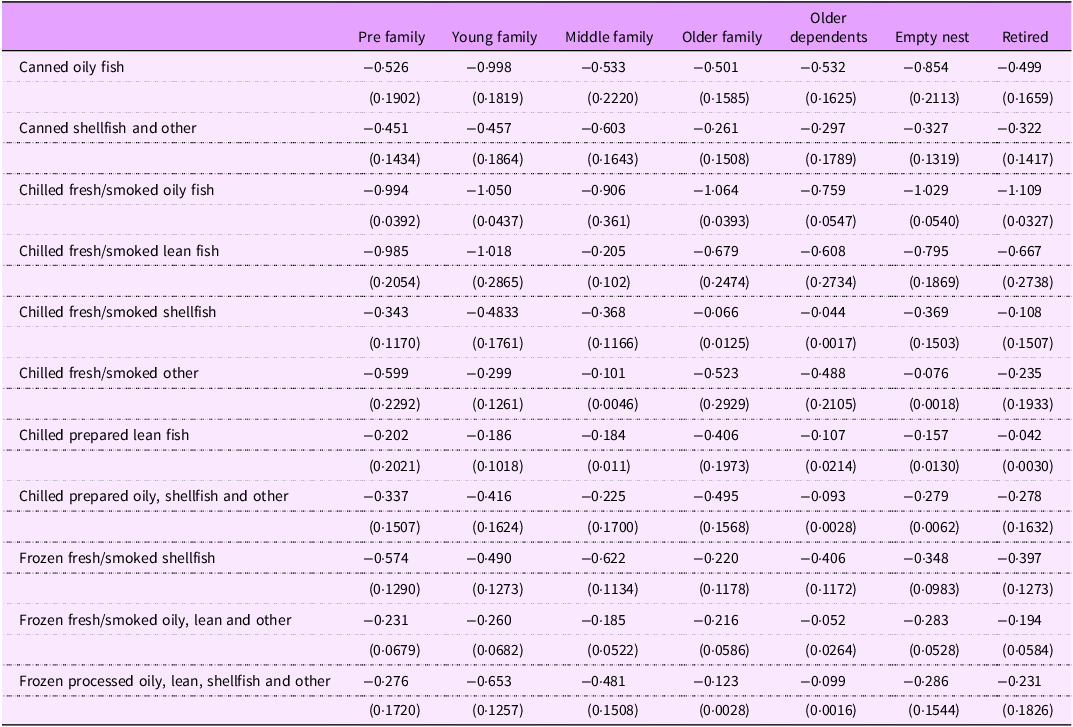

All own-price elasticities, e.g. the percentage change in the quantity demanded in response to a 1 % increase in price, for the eleven fish categories in the seven household groups, were negative. Most of these own-price elasticities were statistically significant at the 5 % level (Table 1). The demand for the chilled fresh/smoked oily was the most price-responsive, whereas demand for frozen fresh/smoked oily, lean and other fish was least responsive to price. However, most own-price elasticities were less than one in absolute values, indicating that the demand for fish products was inelastic in response to price changes. The magnitude of cross-price elasticities varied considerably across household groups but not in any systematic pattern (Appendix 2).

Table 1. Average uncompensated own-price elasticities, 2013–2021

Note: Standard errors are in parentheses.

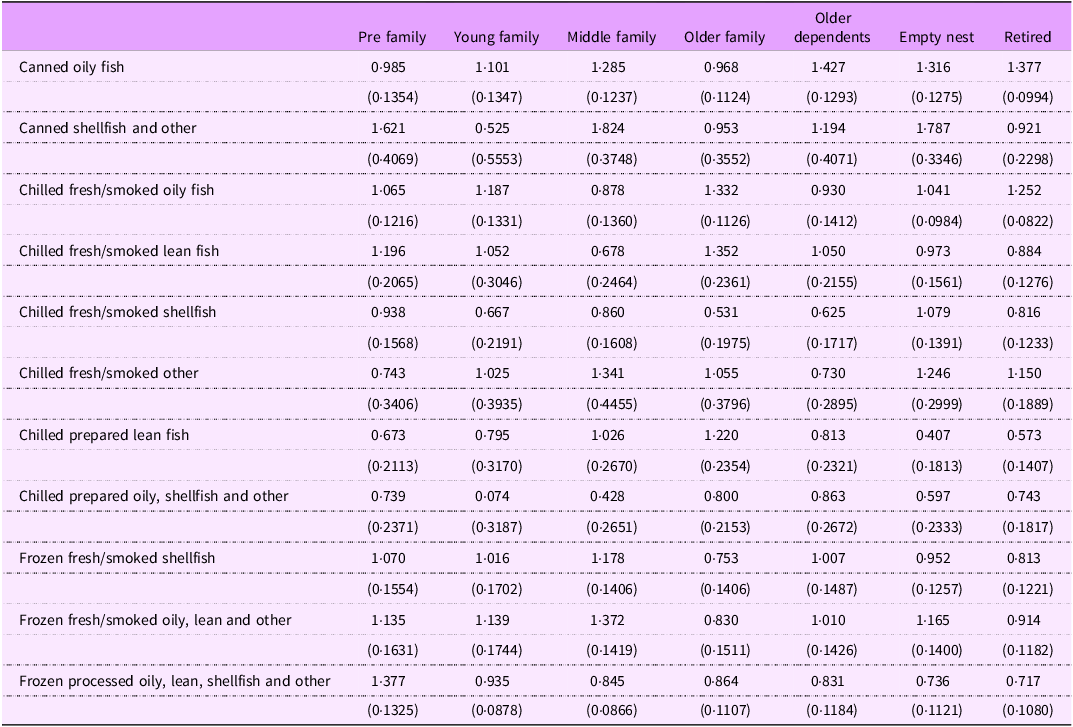

All expenditure elasticities, e.g. the percentage change in quantity demanded of fish groups in response to a 1 % change in total household grocery expenditure, for all household groups, were positive and significant, except for that of canned shellfish and other and chilled prepared oily, shellfish and other in young families, which were positive but non-significant (Table 2). This implies the appeal of, and affordability for, fish for those in higher-income brackets. The varied expenditure elasticities for different product categories within family groups emphasise the varied nature of consumer choices. In all household groups, chilled prepared oily and shellfish and other products display relatively inelastic responses to income changes, indicating a consistent demand regardless of income fluctuations.

Table 2. Average expenditure elasticities, 2013–2021

Note: Standard errors are in parentheses.

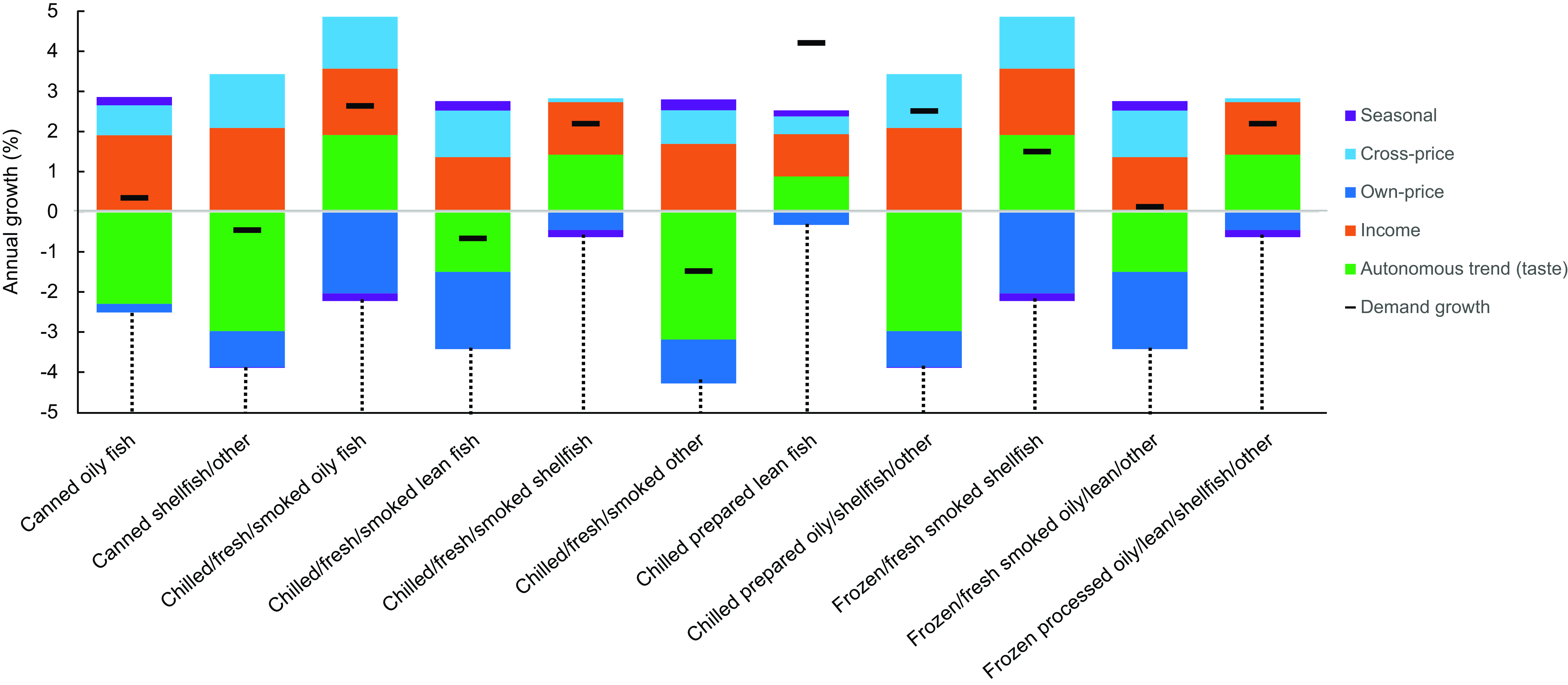

Figure 3 shows the average annual growth in demand and its components for eleven fish groups from 2013 to 2021. Among the eleven fish groups examined, distinct trends emerged. Notably, there was a positive growth trend observed in demand for chilled fresh/smoked oily fish, chilled fresh/smoked shellfish, chilled prepared lean fish and chilled prepared oily, shellfish and other varieties, with growth rates ranging from 2·19 % to 4·20 % annually. Conversely, certain categories experienced a decline in demand, such as canned shellfish and other (–0·46 %), chilled fresh/smoked lean fish (–0·67 %) and chilled fresh/smoked other (–1·48 %). Our analysis of expenditure shares, as illustrated in Figure 2(b), indicates that chilled fresh/smoked oily fish, canned oily fish and frozen processed fish products dominate spending across all demographic groups. However, the annual demand growth rate of canned oily fish remains below one percent in most household groups, suggesting a nuanced interplay of factors influencing consumer behaviour. Despite the current popularity and widespread consumption of canned oily fish, the sluggish growth rates may imply a potential stagnation or saturation in demand over time. For all fish groups, income and autonomous trends (changes in consumer taste) were the most important factors that affected changes in demand for fish. However, price played a comparatively dominant role in the consumption growth of the chilled fresh/smoked oily fish group, chilled fresh/smoked lean fish and frozen fresh fish products (Figure 3). The autonomous trend effects indicate that changes in consumer preferences have reoriented demand away from canned oily fish, canned shellfish and other group, chilled fresh/smoked lean fish, chilled fresh/smoked other fish, chilled prepared oily, shellfish and other, frozen fresh/smoked oily lean and other group, toward chilled fresh smoked oily fish, chilled fresh/smoked shellfish, chilled prepared lean fish and frozen fresh/smoked shellfish, frozen processed oily, lean, shellfish and other.

Figure 3. Average annual growth in demand and its components (seasonal, cross-price, own-price, income and autonomous trend) for the eleven fish subgroups from 2013 to 2021.

Discussion

This study analysed the demand for fish for consumption at home across different household groups in Great Britain between 2013 and 2021. The analysis reveals several consumption behaviours. Notably, empty nesters and retirees purchase more fish compared with younger families. Additionally, this group also prefers higher quality, less processed options like chilled fresh/smoked oily fish. This finding is consistent with previous research showing age-related preferences for fish consumption with older people preferring fresh fish over processed varieties(Reference Manrique and Jensen37–Reference Saidi, Cavallo and Del Giudice39). Families with children consistently allocate a lower share of their grocery spending on whole fish compared with households without children. These results suggest a link between age, household composition and seafood consumption habits. This aligns with prior studies indicating that older individuals tend to consume higher quantities of seafood(Reference Jahns, Raatz and Johnson40–Reference Govzman, Looby and Wang42). Moreover, our observations complement existing research highlighting the health considerations driving seafood consumption among older demographics. With advancing age comes an increased risk of health issues such as cognitive decline and CVD, prompting dietary choices that prioritise nutrient-rich options like seafood(Reference Marushka, Kenny and Batal41,43,44) . In addition, we found that households with children who purchase fish preferred ready-to-use and convenient options, such as canned oily fish and frozen processed fish products. These findings are aligned with previous research indicating that changes in the perceived value of women’s time positively influence demand for processed fish and seafood products(Reference Manrique and Jensen37). Canned oily fish, and frozen processed fish, rank second in expenditure shares among the eleven fish categories, following chilled fresh/smoked oily fish. This is also consistent with previous research showing a preference for ready-to-cook seafood products over whole or round-cut fish in European countries such as France, Germany, Italy and the UK(Reference Menozzi, Nguyen and Sogari45).

Our findings confirm that most fish categories are own-price inelastic, meaning that demand for these categories shows little response to price changes, a pattern also observed in previous studies(Reference Fousekis and Revell14,Reference Jaffry and Brown15,Reference Burton and Young46) . At the same time, our study found positive and significant expenditure elasticities across household groups, indicating a consistent increase in demand in response to increases in total household grocery expenditure (Table 2). However, the magnitudes and patterns differ from those found by Burton & Young(Reference Burton and Young46), who found a unit expenditure elasticity (i.e. when income increases, people do not necessarily spend proportionally more on the same items). Notably, our analysis emphasises the appeal and affordability of certain fish products in higher-income brackets, such as canned shellfish and other for pre-family, middle family and empty nests and chilled fresh/smoked oily fish for young family, older family and retired groups, which corresponds to the observation by Burton(Reference Burton13) about the expenditure elasticity of specific fish types, including white fish and flatfish despite the temporal gap of over three decades. Differences in applied methodologies, sample scope and product aggregation highlight the importance of the need for a nuanced interpretation of results when comparing studies based on economic data.

In all fish categories, income and the autonomous trend (shifts in consumer preferences) were key factors influencing changes in fish demand. This finding is consistent with previous behavioural studies on fish consumption, indicating that taste preferences towards fish and seafood play a pivotal role in shaping fish consumption behaviour(Reference Verbeke, Sioen and Pieniak47,Reference Carlucci, Nocella and De Devitiis48) . Additionally, studies exploring the influence of socio-demographic factors on seafood consumption further support our findings, highlighting that income is a significant determinant of seafood consumption patterns(Reference Jahns, Raatz and Johnson40–Reference Govzman, Looby and Wang42). Thus, contrary to the belief that low fish consumption is primarily due to affordability(Reference Govzman, Looby and Wang42,Reference Love, Thorne-Lyman and Conrad49) , our findings, based on recent data and employing a demand system approach, suggest that the demand for most fish products across household groups is price inelastic. This indicates that while price does play a role, growth in demand is more significantly driven by household income and changes in consumer tastes.

With price having a limited effect on the demand for most fish products, increasing fish consumption, particularly among lower-income groups who do not usually consume much fish, may require more intervention than simply making fish more affordable, for example, through income support programmes such as cash transfers or food vouchers for lower-income households. Given that families with children consistently devote a smaller portion of their grocery budget to purchasing fish, which is in contrast to families without children, policymakers might consider targeted support or promotions for whole fish products for families with children. Such initiatives may include educational programmes focused on the nutritional benefits of whole fish, in-store tastings and special price promotions aimed at incentivising the trial and purchase of whole fish products at the point of sale(Reference Carlucci, Nocella and De Devitiis48,Reference Marushka, Batal and Sadik50) . To double fish consumption in households in Great Britain in order to meet dietary recommendations, policies should prioritise aligning offerings with consumer preferences(Reference Witter, Murray and Sumaila51).

Strengths of this study include the use of the Kantar Worldpanel dataset, which holds data on fish purchases from well over twelve thousand households in Great Britain. The data we used for our analysis were collected over an extensive period of 9 years, providing longer-term information on the price and quantities purchased and the type of promotion used. One limitation of this study is that we performed demand analysis within the fish food group, and therefore, this study does not consider how price changes in other food groups may have affected demand for fish. Additionally, to simplify the analysis and ensure robust estimates, we aggregated fish subgroups, which reduced noise caused by infrequent consumption in certain subcategories. However, this approach may obscure zero consumption levels at more granular subgroup levels, representing a trade-off inherent in using aggregate data. Finally, the classification of the seven household groups follows Kantar’s categorisation of data, and therefore, we were not able to fully capture the diversity of consumers within each of these household groups.

In conclusion, we show that the demand for most fish products across household groups was less dependent on price and more dependent on income and change in taste. Thus, increasing the demand for fish and increasing fish consumption, especially in groups for which the potential health benefits matter most, such as those in lower-income groups who do not usually consume much fish, may require more than simply making fish more affordable. However, addressing the need for increased fish demand must be accompanied by a parallel focus on sustainable expansion of fish supplies, particularly targeting fish species with a high n-3 fatty acid, micronutrient and vitamin content, which are recognised for their health benefits. This approach ensures a balanced alignment between fish supply expansion and consumer preferences, particularly those demonstrating elasticity to income and price changes. Moreover, it mitigates the risk of upward pressure on fish prices, thereby preventing unintended consequences. The success of the above policy suggestions relies on collaborative efforts between government entities, the fish and seafood industry, retailers and consumer advocacy groups. By working together, these stakeholders can ensure a holistic and effective approach to sustainable fish market growth, thereby safeguarding public health and promoting access to nutritious seafood options for all consumers.

Acknowledgments

The authors thank Anneli Lofstedt, Magaly Aceves Martins and Cathrine Baungaard for their helpful comments and suggestions.

Authorship

SDR: conceptualisation, data preparation, investigation, visualisation, formal analysis, writing – original draft, writing – review, and editing. CR-G: data preparation, investigation, visualisation, formal analysis, writing – review, and editing. BdR: investigation, visualisation, formal analysis, writing – review and editing.

Financial support

This research was funded by the Rural and Environment Science and Analytical Services Division (RESAS) of the Scottish Government, project RI-B5–04

Competing interests

There are no conflicts of interest.

Ethics of human subject participation

Not applicable.

Appendices

Appendix 1A

The calculation of the test statistic follows the approach outlined in Court (1968) and Deaton (1974);

$$F = {{{{tr{{\left( {{\Omega ^R}} \right)}^{ - 1}}\left( {{\Omega ^R} - {\Omega ^U}} \right)} \mathord{\big/ {\vphantom {{tr{{\left( {{\Omega ^R}} \right)}^{ - 1}}\left( {{\Omega ^R} - {\Omega ^U}} \right)} q}} } q}} \over {{{tr{{\left( {{\Omega ^R}} \right)}^{ - 1}}{\Omega ^U}} \mathord{\big/ {\vphantom {{tr{{\left( {{\Omega ^R}} \right)}^{ - 1}}{\Omega ^U}} {\left( {n - 1} \right)\left( {T - k} \right)}}} } {\left( {n - 1} \right)\left( {T - k} \right)}}}}$$

$$F = {{{{tr{{\left( {{\Omega ^R}} \right)}^{ - 1}}\left( {{\Omega ^R} - {\Omega ^U}} \right)} \mathord{\big/ {\vphantom {{tr{{\left( {{\Omega ^R}} \right)}^{ - 1}}\left( {{\Omega ^R} - {\Omega ^U}} \right)} q}} } q}} \over {{{tr{{\left( {{\Omega ^R}} \right)}^{ - 1}}{\Omega ^U}} \mathord{\big/ {\vphantom {{tr{{\left( {{\Omega ^R}} \right)}^{ - 1}}{\Omega ^U}} {\left( {n - 1} \right)\left( {T - k} \right)}}} } {\left( {n - 1} \right)\left( {T - k} \right)}}}}$$

where Ω R and Ω U denote the estimated residual covariance matrices with and without restrictions imposed, respectively, T is the number of observations, n is the number of equations in the system, k is the number of estimated parameters in each equation and q is the number of restrictions. The test statistic F follows an approximate distribution as F[q, (n-1)(T–k)].

Appendix 1B Testing demand homogeneity and Slutsky symmetry

* denotes critical value and conclusion at α = 0·01.

Appendix 2 Uncompensated price elasticities

Note: Standard errors are in parentheses. Own-price elasticities are shown in bold for ease of identification.

Open access

Open access