I. Introduction

A number of prior studies analyze the evolution of CEO compensation around acquisitions and generally report increases in CEO pay following acquisitions.Footnote 1 The predominant explanation for such increases is that they reflect an underlying agency problem between managers and shareholders. Consistent with this view, these studies report that postacquisition compensation increases tend to be uncorrelated with measures of acquisition performance. An alternative (though not mutually exclusive) explanation, however, is that compensation changes following acquisitions reflect an optimal recontracting between managers and shareholders in acquisitions that alter both the scale and risk profile of the acquirer.

To provide fresh evidence on how CEO compensation is altered following acquisitions, we reexamine this issue over an extended and more recent sample period (1993–2018). Our primary contribution is to document that the positive association between acquisitions and CEO compensation previously documented in the literature is limited to acquisitions in which common stock is used as the method of payment and the acquisition is subsequently completed. Moreover, the increases in compensation following all-stock acquisitions are driven primarily by changes in equity-based compensation. Although there is some evidence of changes in salary and bonus, these changes are much smaller economically and often statistically insignificant. We further find that in a reduced sample of 342 firms that make at least one all-stock acquisition and one acquisition in which the method of payment is not all stock over the sample time period, significant changes in CEO compensation following acquisitions continue to be driven by deals that use all stock as the method of payment.

Our descriptive evidence thus implies that in order to understand the factors driving changes in CEO compensation following acquisitions, we need to understand why such changes are specific to completed, all-stock acquisitions and why these compensation changes primarily take the form of increases in equity-based compensation. Toward that end, we explore two nonmutually exclusive possibilities.

First, under the standard agency explanation, entrenched managers pursue acquisitions to expand their empire and use the acquisition and their influence over the board to increase their compensation. This might be particularly effective in stock acquisitions because such acquisitions avoid the scrutiny of the capital market that is associated with raising cash through external financing.Footnote 2 We find little evidence for this explanation, however. Specifically, we find no evidence that changes in compensation following all-stock acquisitions are associated with measures of poor corporate governance. In fact, using one measure of corporate governance, board capture, we find the evidence goes in the opposite direction. Moreover, insofar as entrenched CEOs capture higher compensation, our additional finding that greater CEO compensation in all-stock acquisitions is concentrated in CEOs with low levels of compensation prior to the acquisition announcement is also inconsistent with this hypothesis.

Second, we investigate the possibility that the compensation dynamics that we observe surrounding all-stock acquisitions represent endogenous contracting solutions to frictions associated with adverse selection in the acquisition market. Prior studies dating back at least to Hansen (Reference Hansen1987) have recognized that acquirers face an adverse selection problem when targets possess superior information about their value. These studies predict that in this setting, acquirers offer stock as a contingent payment mechanism in which target shareholders receive smaller payments if the value of the target (and, therefore, the combined postacquisition company) subsequently declines. More recent studies have emphasized, however, that target shareholders also face an adverse selection problem when acquirers use their common stock as the method of payment in the acquisition because overvalued acquirers have an incentive to use their equity as a cheap currency in the transaction.Footnote 3 Because a shift in compensation toward greater equity-based pay for the acquiring firm CEO bonds the informed CEO to the stock price, the CEO’s willingness to accept this form of payment is one way for the acquirer to credibly signal that the acquirer’s stock is not overvalued as in Leland and Pyle (Reference Leland and Pyle1977).Footnote 4 Because the combination of the increase in risk associated with the acquisition and the greater equity-based pay increases the risk of the CEO’s overall compensation package, however, the CEO’s total compensation must increase to satisfy the CEO’s participation constraint (e.g., Hölmstrom (Reference Hölmstrom1979)).

We report a series of results consistent with this two-sided adverse selection argument. First, we find that changes in CEO compensation for all-stock acquisitions are greater for acquirers with a greater risk of overvaluation than for less risky acquirers. This association with acquirer risk is not present in either mixed payment acquisitions or all-cash acquisitions. Second, when the CEO’s exposure to the stock price is low prior to the acquisition (i.e., when the acquirer CEO is less bonded to the stock price), we find that increases in CEO pay are larger in all-stock acquisition years than in nonacquisition years, all-cash acquisition years, and mixed acquisition years. These two findings are consistent with acquirers in all-stock acquisitions using equity-based pay to bond the CEO to the stock price and mitigate target firm concerns about overvalued equity when i) there is more uncertainty about the acquirer’s value and ii) when the acquiring firm CEO is less bonded to the acquirer’s stock price prior to the acquisition. Moreover, consistent with the increase in equity-based compensation serving as a credible signal of acquirer value, we find that the acquirer’s abnormal stock returns from 1 month prior through 12 months following the acquisition announcement are positively associated with increases in the CEO’s equity-based compensation, but only for acquisitions involving acquirer stock.

With respect to the acquirer’s concern about the value of the acquisition, we find that increases in CEO compensation following all-stock acquisitions are significantly greater in acquisitions with above-median risk. Moreover, this increase is paid predominately in equity-based compensation. For acquisitions with below-median risk, there is no evidence of increases in either fixed or equity-based compensation. Furthermore, there is no evidence of compensation changes for high-risk acquisitions that are either all-cash or mixed payment.

Although each of these findings is consistent with the dual adverse selection hypothesis, an important caveat is that we do not observe the timing of when the target becomes aware of the changes in acquirer CEO compensation. In order for the changes in equity-based pay to bond the acquirer CEO to the stock price and, therefore, mitigate target firm concerns about overvalued equity, it is critical that the acquirer can credibly commit to the target that the compensation changes will take place. Lacking direct evidence on when the target learns this information, we conduct two additional tests that provide indirect evidence on this issue. Although both tests have limitations and, thus, cannot be viewed as conclusive on their own, both are consistent with dual adverse selection issues contributing to the compensation dynamics that we observe.

First, based on our observation that most compensation grants are awarded in the first 2 months of the fiscal year, we conjecture that the likelihood of the target knowing about the planned postacquisition changes in compensation is substantially greater if the acquisition is announced after the first 2 months of the fiscal year. Thus, if postacquisition changes in compensation for stock acquisitions are a response to dual adverse selection concerns, they should be greater for acquisitions announced after the first 2 months of the year. Consistent with this view, we find no evidence of significant changes in compensation following stock acquisitions announced in the first 2 months of the fiscal year. By contrast, stock acquisitions announced after the first 2 months of the fiscal year are associated with significant increases in compensation. Notably, these differences across the fiscal year are not present in cash or mixed payment deals, nor are they present for withdrawn acquisitions.

Second, we hypothesize that when a CEO change is announced prior to or in conjunction with the acquisition, it is likely that the target is aware of the transition and, therefore, aware of planned postacquisition CEO compensation. Consistent with this view, we find that compensation changes following stock acquisitions are significantly larger in stock acquisitions in which there is a change in CEO. Moreover, the increase in compensation for stock acquisitions with CEO changes is limited to those acquisitions in which the CEO change is announced prior to the announcement of the acquisition. Again, these patterns are observed only in stock acquisitions; they are not observed in cash or mixed payment deals, nor in withdrawn acquisitions.

Taken together, our findings cast doubt on the view that compensation changes provide perverse incentives for CEOs to pursue acquisitions even if they are value reducing. Although we cannot completely rule out agency concerns, our evidence suggests that the changes in CEO compensation following acquisitions stem primarily from a desire to mitigate target firms’ adverse selection concerns about accepting bidder stock as a method of payment.

II. Related Literature

Previous studies of the evolution of CEO compensation around acquisitions find that CEOs benefit from acquisitions. Examining the period 1993–1999, Grinstein and Hribar (Reference Grinstein and Hribar2004) find that CEO bonus compensation for completed acquisitions is positively related to CEO power and these increases are not related to acquisition performance. They conclude, “Managerial power is the primary driver of M&A bonuses.” Examining the period 1993–2000, Harford and Li (Reference Harford and Li2007) find acquisitions insulate the CEOs from downside risk. The value of the CEO’s portfolio after an acquisition is positively related to long-term stock returns for positive returns, but unrelated to stock returns for negative returns.Footnote 5 Similarly, Fu, Lin, and Officer (Reference Fu, Lin and Officer2013) suggest CEOs in firms with overvalued stock pursue stock financed acquisitions in order to receive large equity grants. In the study most closely related to our study, Yim (Reference Yim2013) investigates the period 1993–2007. She finds CEO compensation increases are greater in years in which firms announce an acquisition. Yim further finds the positive relation between acquisitions and CEO compensation increases is driven by young CEOs. Such findings are broadly consistent with Jensen (Reference Jensen1986), Jensen and Murphy (Reference Jensen and Murphy1990), and Stulz (Reference Stulz1990), who highlight managers’ agency-based motivations to increase the size of the firm, such as increased managerial power and compensation.

Other studies have analyzed the consequences of acquirers using their stock as the method of payment in acquisitions. Although neoclassical theory suggests that mergers should increase the value of both the target and acquiring firm, studies find that average returns for acquirers around the announcement of the acquisition of a public target are indistinguishable from zero, on average, and negative in the case of acquisitions financed by stock (e.g., Travlos (Reference Travlos1987), Loughran and Vijh (Reference Loughran and Vijh1997)).Footnote 6 One interpretation of this finding is that the market interprets the choice to pay with stock as a potential signal of overvaluation of the acquirer and decreases the acquirer stock price accordingly. Indeed, Golubov, Petmezas, and Travlos (Reference Golubov, Petmezas and Travlos2016) conclude that the negative announcement returns for stock financed acquisitions come entirely from the negative signal associated with issuing stock.

The possibility that the acquirer’s stock is overvalued when used as a method of payment has been explored further in another set of studies. Some studies offer explanations for why stock-swap transactions might be completed even if the acquirer’s stock is overvalued. For example, Shleifer and Vishny (Reference Shleifer and Vishny2003) speculate that target managers might accept overvalued equity as a means of payment either because i) they have short horizons and can sell the overvalued shares when the transaction is consummated or ii) they receive side payments from acquirers. In Rhodes-Kropf and Vishnawathan (Reference Rhodes-Kropf and Vishnawathan2004), targets rationally accept overvalued acquirer stock as a method of payment because of correlated misinformation. By contrast, in Fu, Lin, and Officer (Reference Fu, Lin and Officer2013), target firms rationally incorporate the perceived overvaluation of the acquirer into the negotiated exchange ratio and offer premium.

Other studies explore the use of acquirer stock as the method of payment as a function of the potential degree of overvaluation. For example, Eckbo, Makaew, and Thorburn (Reference Eckbo, Makaew and Thorburn2018) provide evidence that acquisition bids are more likely to include acquirer equity as the method of payment when targets are more informed about bidders. Absent this information, targets would rationally discount the value of the bidder’s shares, thereby reducing the bidder’s incentive to use this method of payment. We extend this logic and that of the Leland and Pyle (Reference Leland and Pyle1977) model to conjecture that one potential solution to this adverse selection problem is for the bidder to offer a credible signal through changes in its compensation contract with the CEO.

Two recent papers explore the sharp drop in the proportion of acquirers paying exclusively with stock. Boone, Lie, and Liu (Reference Boone, Lie and Liu2014) document the decreased frequency of stock financed acquisitions since the early to mid-2000s in their sample of acquisitions with public acquirers and public targets and find that only a portion of the time series variation in methods of payment is due to variation in their measures of adverse selection, taxation, and contracting costs. de Bodt, Cousin, and Roll (Reference de Bodt, Cousin and Roll2018) note that the percentage of stock financed acquisitions drops from around 50% before 2001 to around 10% after 2010 and that the beginning of the decline in 2001 coincides with the abolishment of the pooling method of accounting.

Our primary contribution is to extend the previous literature by documenting novel evidence on how CEO compensation changes following acquisitions are strongly linked to the method of payment and come primarily in the form of increased equity-linked pay. Having established these two primary stylized facts, we then build on the prior literature to develop and test two main hypotheses for the cross-sectional variation in compensation changes following acquisitions: the Agency Hypothesis and the Dual Adverse Selection Hypothesis.

III. Sample Selection and Data Description

We begin with the Compustat universe of firms between 1993 and 2018 and merge this data set with data from a variety of sources. The acquisition data come from Thomson Reuters SDC Platinum database (SDC). We include acquisitions by U.S. public acquirers and require the acquisition to be a merger, acquisition, acquisition of majority interest, or acquisition of assets. Similar to Yim (Reference Yim2013), we further require the acquisition value to be at least 5% of the market value of equity of the acquiring firm as of the previous fiscal year end. The CEO compensation data comes from the Execucomp database. Return data are from the Center for Research in Security Prices (CRSP) and implied volatility data are from the Optionmetrics database. We also use governance data from the Institutional Shareholder Services’ Governance database. Variable definitions are detailed in the Appendix.

Panel A of Table 1 reports summary statistics for characteristics of the sample acquisitions. We also partition the sample into two equal subperiods—1993–2005 and 2006–2018—and report summary statistics for these subperiods as well. Over our sample period, 11.4% of firm-years have a 5% acquisition. This percentage decreases from 12.1% of firm-years in the early period to 10.8% in the late period. We define an acquisition as being All Stock if the consideration paid is at least 95% stock. Using this definition, the method of payment is all stock in 14% of the acquisitions, all cash in 33% of the acquisitions, and mixed payment in 53% of the acquisitions. Consistent with prior literature (e.g., Boone, Lie, and Liu (Reference Boone, Lie and Liu2014), de Bodt, Cousin, and Roll (Reference de Bodt, Cousin and Roll2018)), the method of payment for the acquisitions changes sharply across the periods. The frequency of acquisitions in which the consideration is composed of at least 95% stock (All stock) drops from 22.5% in the early period to 6.1% in the late period. Making up for most of the drop in all-stock acquisitions, the frequency of acquisitions in which the consideration is composed of at least 95% cash (All cash) jumps from 27.4% to 39.0%. The frequency of all other acquisitions, designated Mixed acquisitions, increases slightly from 50.1% to 54.9%.

TABLE 1 Summary Statistics

In Panel B of Table 1, we compare firm characteristics for the nonacquiring firm-years with those of the subset of firm-years with an acquisition announcement. Chg CEO Comp is the change in total CEO compensation from the year prior to acquisition announcement divided by the prior year compensation and is winsorized at the 1st and 99th percentiles. Assets is the prior year assets for the firm (denoted in $millions). Firm age is the number of years since the firm was listed on CRSP. Market-to-Book is the prior fiscal year end ratio of the market value of assets to the book value of assets and is winsorized at the 1st and 99th percentiles. Prior year return is the buy and hold return for the stock over the prior fiscal year. ROA is the return on assets at the end of the prior fiscal year and is winsorized at the 1st and 99th percentiles. Change in CEO is an indicator variable equal to 1 if there was a change in CEO. CEO age is the age of the CEO. CEO compensation is the total compensation for the CEO of the firm in the prior year. We use these variables throughout the article. We will discuss the variables that are specific to the second part of the analysis later in the article when we examine cross-sectional variation in the relation between increases in CEO compensation and method of payment in acquisitions.

Consistent with Yim (Reference Yim2013), the univariate comparisons in Panel B indicate that increases in total CEO compensation are higher in acquisition firm-years than in nonacquisition firm-years by 4.0% (p = 0.045). In addition, acquisition firm-years are characterized by fewer assets, younger firms, higher prior year returns, higher ROA, are less likely to replace the CEO, and have younger CEOs. We find no significant differences in prior year CEO total compensation between the acquisition and nonacquisition firm-years.

IV. Changes in CEO Compensation Following Acquisitions

In this section, we present our primary descriptive findings on changes in CEO compensation following the sample acquisitions and the link between such compensation changes and the method of payment.

A. Changes in Total Compensation

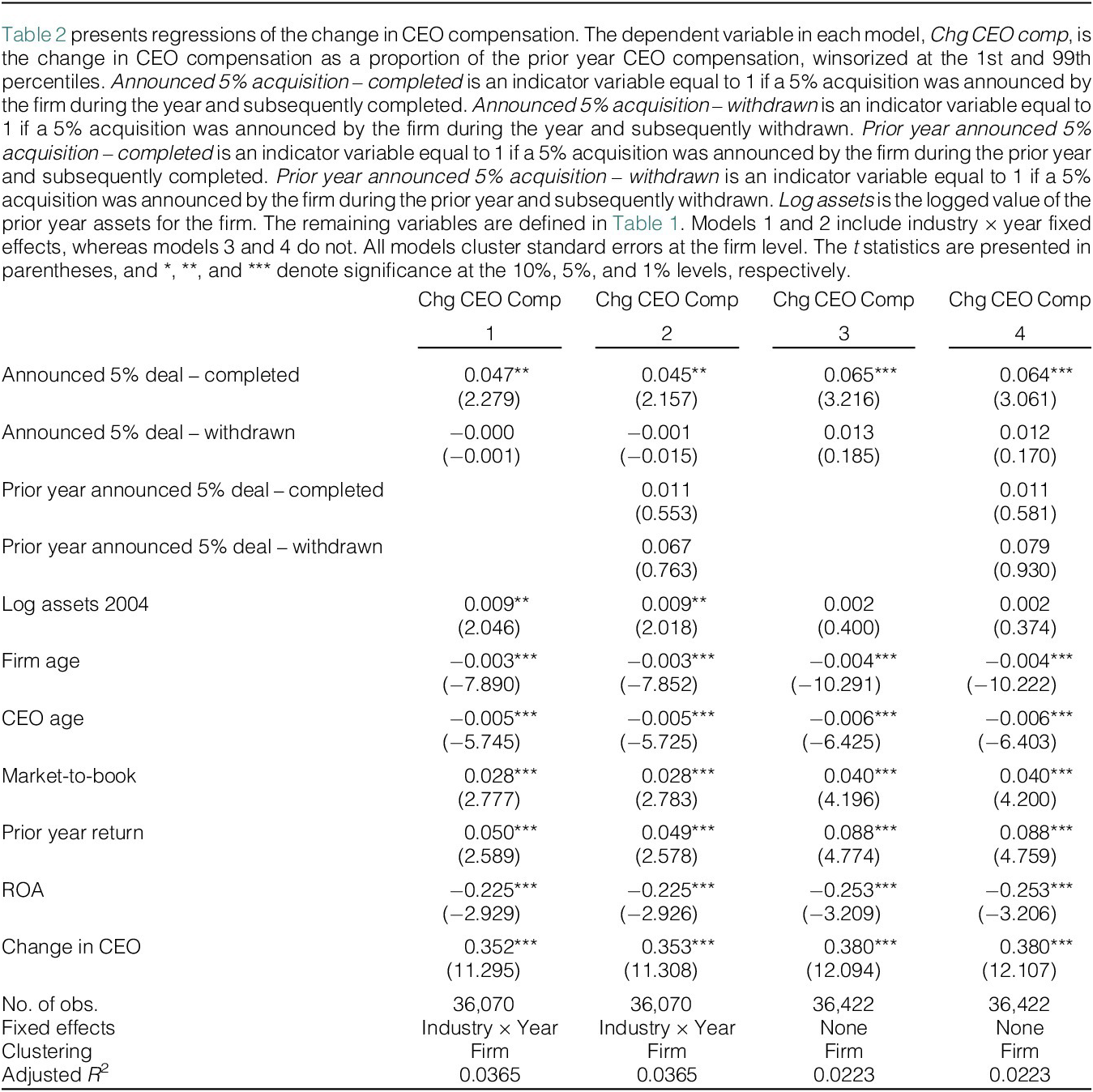

Table 2 reports coefficient estimates and t-statistics from regressions that test for differences in the change in CEO compensation for firm-years in which a 5% acquisition is announced during the year and nonacquiring firm-years. The model is based on those estimated in Yim (Reference Yim2013) in which the dependent variable is the change in total compensation from the prior year divided by the prior year’s total compensation (winsorized at the 1st and 99th percentiles). The independent variable of interest (Announced 5% deal – completed) is an indicator equal to 1 if the firm announced a 5% acquisition during the year and that acquisition was subsequently completed. We also include the variable (Announced 5% deal – withdrawn) indicating the firm announced a 5% acquisition during the year that was subsequently withdrawn. All models control for log of assets, firm age, market-to-book, prior year return, ROA, and an indicator for a change in the CEO. Models 1 and 2 include industry-year fixed effects and models 3 and 4 do not. All models cluster standard errors by firm.

TABLE 2 Multivariate Analysis of CEO Compensation

Consistent with Yim (Reference Yim2013), we find that changes in CEO compensation are significantly greater in firm-years in which a firm announces a 5% acquisition that is subsequently completed than in firm-years for which there is no 5% acquisition announcement. Specifically, our point estimates in models 1 and 2 suggest that the change in compensation is approximately 5 percentage points higher in acquisition firm-years than in nonacquisition firm-years, but only if the acquisition is completed.

One concern is that because there are few withdrawn acquisitions, our use of industry-year fixed effects might lead our findings to be driven by outliers. To address this concern, models 3 and 4 estimate the regressions without fixed effects. The results are slightly stronger. Completed acquisition firm-years are associated with significantly greater increases in CEO pay, but withdrawn acquisition firm-years are not.

B. Changes in Individual Components of Compensation

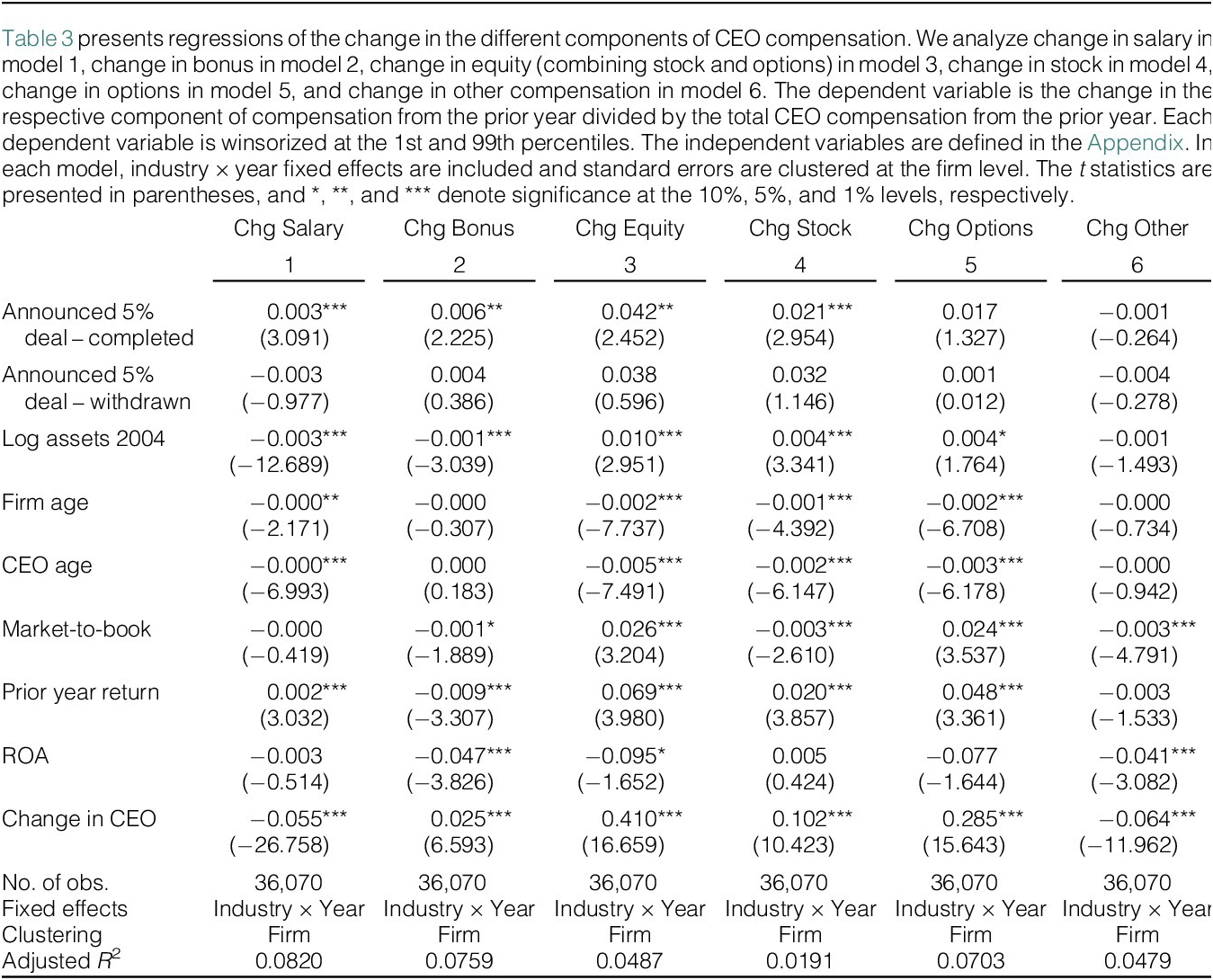

Table 3 breaks down the changes in compensation into their component parts: salary, bonus, equity (stock plus options), stock, option, and other. For each component of compensation, the dependent variable is defined as the change in the component (value in the current year minus the value in the prior year) divided by the prior year total compensation. We include the same control variables as in Table 2, include industry-year fixed effects, and cluster standard errors at the firm level.

TABLE 3 Change in the Components of CEO Compensation

The results suggest that the increase in compensation associated with acquisitions is predominately coming from equity-based compensation. Acquisition firm-years are associated with an additional 4.2% increase in CEO compensation through equity grants (restricted stock and options). Salary and bonus increases are also larger for acquirers, but the economic magnitudes are only 0.3% and 0.6% of prior compensation, respectively.

C. Changes in Compensation by Method of Payment

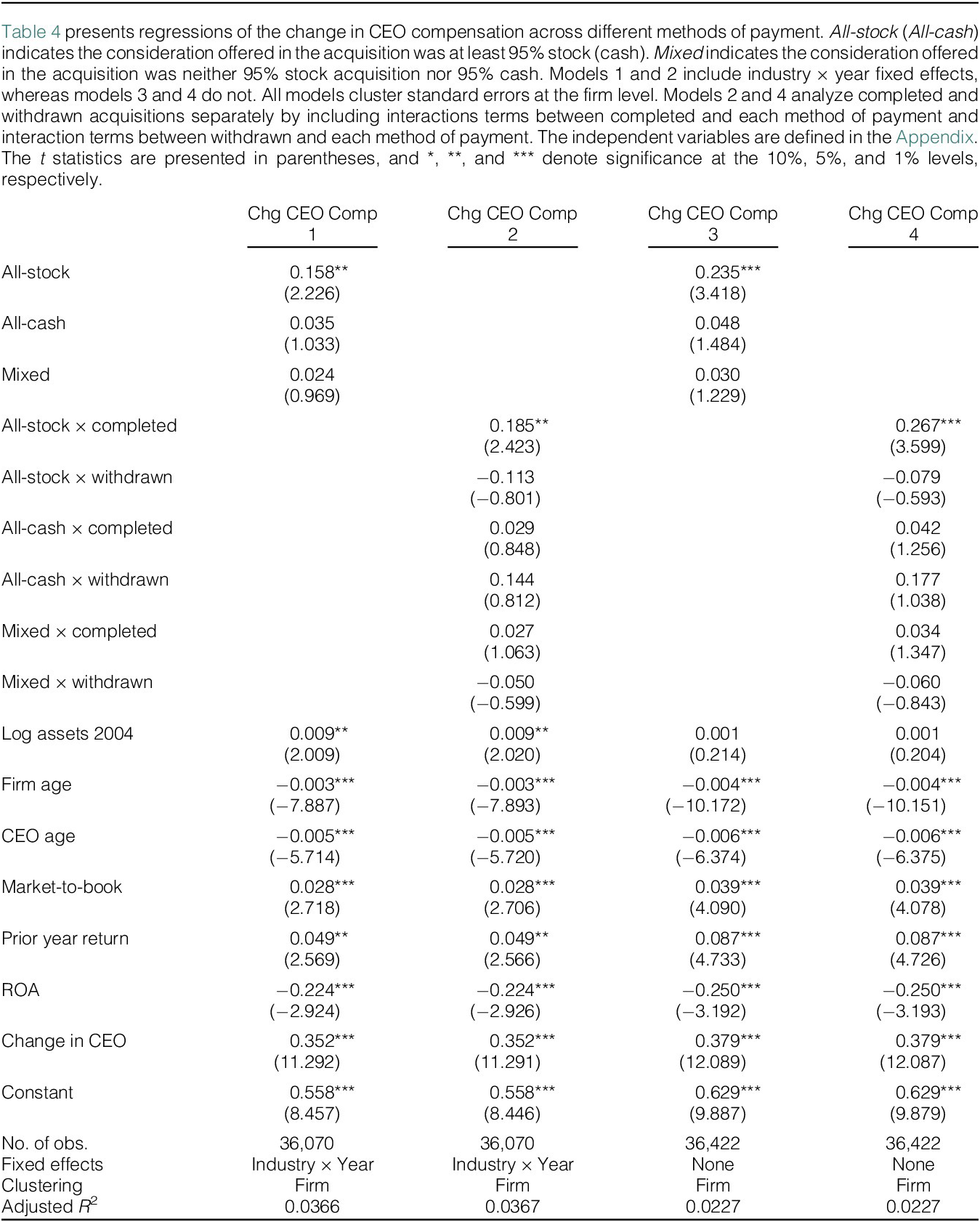

To further understand acquisition related changes in CEO compensation, we separate acquisitions based on the method of payment in the acquisition, specifically all-stock, all-cash, and mixed acquisitions, and reestimate the change in compensation regressions. We include the same control variables as in the previous regressions, and cluster standard errors at the firm level. Because the regressions include all firm-years, the coefficients on the method-of-payment variables measure the difference in compensation for that subset acquisition firm-years relative to nonacquisition firm-years.

The results when industry fixed effects are included, presented in models 1 and 2 of Table 4, indicate that all-stock acquisitions overwhelmingly drive the acquisition related increase in CEO compensation. In model 1, all-stock acquisitions are associated with an additional 16 percentage point increase in CEO compensation, whereas changes in compensation for all-cash and mixed acquisitions are no different than comparable nonacquisition firm-years. In model 2, we further divide the announced acquisitions into those that are subsequently completed and those that are eventually withdrawn. These findings indicate that compensation increases following acquisition announcements are driven exclusively by the set of all-stock acquisitions that are completed.Footnote 7 Neither all-cash acquisitions nor mixed acquisitions are associated with statistically significant CEO compensation increases, regardless of whether they are completed or not.

TABLE 4 Change in CEO Compensation by Method of Payment

In models 3 and 4, we again estimate the change in compensation regression without fixed effects and find qualitatively identical results. Completed all-stock acquisitions are associated with significant increases in pay relative to nonacquisition firm-years, while withdrawn all-stock acquisitions, all-cash acquisitions (completed and withdrawn), and mixed payment acquisitions (completed and withdrawn) are not.

Table 5 provides further evidence by comparing changes in compensation across stock and nonstock acquisitions for the same acquirer. Specifically, we reestimate the Table 4 regressions using a reduced sample of 342 firms that make at least one all-stock acquisition and one acquisition in which the method of payment is not all stock over the sample time period. This allows us to control for firm-level unobservable variables that might be correlated with firms proposing to use stock as the method of payment.

TABLE 5 Repeat Acquirers

In column 1, we replicate model 3 of Table 4 excluding fixed effects and show that we continue to find a statistically significant increase in CEO compensation following all-stock acquisitions in the reduced sample.Footnote 8 In column 2, we exclude firm-level controls but add firm-fixed effects so that now the coefficient on the All-Stock variable measures the within-firm difference in the change in CEO compensation for all-stock acquisitions versus the cash and mixed acquisitions made by the same firm. The results continue to indicate that all-stock acquisitions result in significantly larger changes in CEO compensation following all-stock acquisitions. Finally, in column 3, we add firm-level controls in addition to the firm fixed effects and observe little difference in the All-Stock coefficient. The evidence from repeat acquirers in Table 5 thus provides further evidence that significant changes in CEO compensation following acquisitions are driven by deals that use all stock as the method of payment.

D. Changes in Components of Compensation by Method of Payment

To investigate which components of CEO compensation increases around acquisitions for each method of payment, Table 6 breaks down the changes in compensation into their component parts for each type of acquisition consideration. These results indicate that changes in CEO compensation are driven by changes in equity-based pay for all-stock completed acquisitions. There is little evidence of changes in pay otherwise, except for some evidence of increases in equity-based pay with mixed methods of payment. In other words, the increase in CEO compensation associated with all-stock acquisitions is paid primarily in the form of equity-based compensation.Footnote 9

TABLE 6 Change in the Components of CEO Compensation by Method of Payment

E. Robustness Tests and Extensions

In this section, we report on two robustness tests of our main findings. We provide only a brief summary of the findings here, but detailed results can be found in the Supplementary Material of the article.

1. Definition of All-Stock and Mixed Payment Acquisitions

We define an acquisition as being “all stock” if at least 95% of the consideration being paid is the common stock of the acquirer. Mixed payment acquisitions are those in which either some stock is used in the acquisition or if no method of payment is listed in SDC. If our main findings on compensation changes following acquisitions are due to companies using stock as a method of payment, it seems plausible that mixed payment acquisitions for which a large proportion of the payment is stock might also exhibit compensation increases.

To test this conjecture, we divide mixed acquisitions into three sets: those for which the proportion of stock used is between 75% and 95% of the total consideration paid, those for which the proportion of stock used is between 5% and 75%, and those for which the proportion of stock used is unknown. For the 75%–95% group, we find coefficient estimates that indicate increases in CEO compensation that are similar to what we find in Table 4 for the subsample of all-stock acquisitions, and are significant at the 0.10 level in one of the specifications (Table IA1 in the Supplementary Material). By contrast, for the 5%–75% and “unknown” groups, we find changes in pay that are statistically insignificant and economically small. We conclude, therefore, that increases in CEO compensation associated with acquisitions are limited to acquisitions in which the large majority of payment comes in the form of acquirer stock.

2. Execucomp Reporting of Total Compensation

Because Execucomp changed the manner in which it reported compensation data in 2006, the changes in compensation for the 2006 period could reflect the reporting change rather than an actual change in compensation. We show in the Supplementary Material (Table IA2), however, that our findings are robust to excluding acquisitions announced in 2006.

V. Why Are Changes in Compensation Unique to Stock Acquisitions?

In this section, we introduce two broad hypotheses that can explain why significant changes in CEO compensation following acquisitions are limited to acquisitions in which common stock is used as the primary method of payment and why the changes in compensation are driven primarily by changes in equity-based compensation. We then derive additional testable implications of each hypothesis and empirically analyze these predictions.

A. The Agency and Dual Adverse Selection Hypotheses

The Agency Hypothesis posits that an entrenched CEO pursues an acquisition to increase the size of her empire. The empire building CEO avoids using debt to bypass market scrutiny of the acquisition, evade additional monitoring, and preserve flexibility in the allocation of future cash flows (e.g., Jensen (Reference Jensen1986)). In addition, the entrenched CEO takes advantage of the transition event by leveraging her influence over the board of directors to increase her own compensation (Grinstein and Hribar (Reference Grinstein and Hribar2004)).Footnote 10 Under this hypothesis, therefore, we first expect greater CEO compensation increases in all-stock acquisitions with entrenched CEOs and weak board oversight. Second, insofar as the empire building CEO knows the acquisition is value destroying, we expect the compensation increase to come in the form of nonequity compensation. In general, it is not clear whether entrenched CEOs would prefer cash or stock compensation. On the one hand, stock compensation allows CEOs to consolidate their control and more readily participate in positive stock price movements. However, in the context of the Agency Hypothesis, the acquisitions pursued by entrenched CEOs that are labeled as agency motivated are, by definition, value reducing. Thus, entrenched CEOs receiving stock compensation would be financially worse off than if they received cash compensation. Even if entrenched CEOs desired more stock (perhaps for control reasons), they would be better off receiving cash compensation, then using the cash to purchase shares following completion of the acquisition. Third, we expect these entrenched CEOs to have used their power to capture abnormally high compensation prior to an acquisition (Bebchuk and Fried (Reference Bebchuk and Fried2003)).Footnote 11

The Dual Adverse Selection Hypothesis posits that observed changes in compensation represent a contracting solution to frictions from potential adverse selection concerns in the target and acquiring firms. The acquirer can mitigate the adverse selection concern of overpaying for the target firm by using stock as the method of payment (Hansen (Reference Hansen1987), Eckbo, Giammarino, and Heinkel (Reference Eckbo, Giammarino and Heinkel1990)). However, stock payment creates an adverse selection concern for target shareholders of accepting overvalued equity from the acquirer (Shleifer and Vishny (Reference Shleifer and Vishny2003)). To reduce the target firm’s overvaluation concerns, the CEO of the acquirer can bond herself to the accuracy of the acquirer stock price by increasing her stock-based compensation. That is, the privately informed CEO credibly signals the acquirer is not overvalued by increasing her exposure to the firm’s stock price.Footnote 12 The resulting increase in the acquiring CEO’s exposure to firm risk increases her participation constraint, requiring an increase in overall CEO compensation (Hölmstrom (Reference Hölmstrom1979)).

The fact that announced all-stock acquisitions that are withdrawn do not exhibit increases in CEO equity-based compensation supports the Dual Adverse Selection hypothesis in that it suggests that in the absence of expected changes in compensation, all-stock acquisitions are likely to be withdrawn. In addition, the Dual Adverse Selection Hypothesis further predicts that in stock financed acquisitions, greater increases in CEO compensation are related to greater concerns about target firm adverse selection and acquirer firm overvaluation. It also predicts greater increases in equity-based CEO compensation in acquisitions using stock as the form of payment. The required increase in CEO bonding through an increase in equity compensation is greater when the CEO’s exposure to the stock price before the acquisition is low.Footnote 13

It is important to note that the Agency and Dual Adverse Selection hypotheses are not mutually exclusive. Both effects may be present in the data and, if so, observed compensation structures may reflect the impact of both agency and adverse selection considerations. Accordingly, our tests are designed to uncover the extent to which cross-sectional differences in compensation changes are consistent with predictions from each of our two main hypotheses.

B. Cross-Sectional Variation in Changes in CEO Compensation

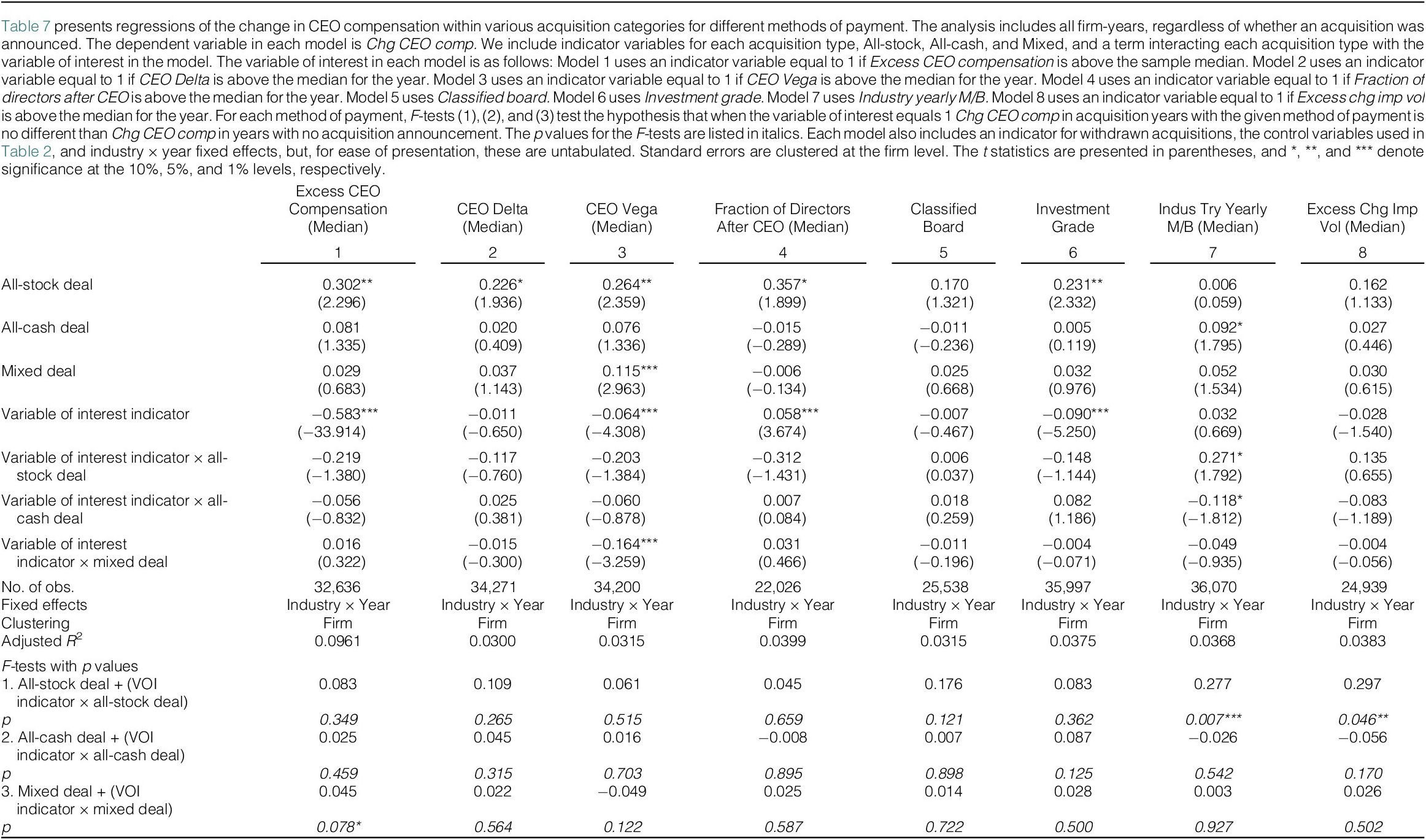

To provide direct evidence on the Agency and Dual Adverse Selection hypotheses, we extend the Table 4 regressions to test for cross-sectional differences in postacquisition changes in CEO compensation between acquisitions with different firm and acquisition characteristics that proxy for Agency and Dual Adverse Selection considerations. More specifically, we test whether the increases in compensation following all-stock deals are greater when there appear to be greater ex ante agency problems or when there appear to be greater dual adverse selection concerns (or both).

In Table 7, we present the results of regression models in which the dependent variable is change in CEO compensation. The regressions augment our specification in Table 4 by including an indicator variable for a high value of the proxy variable of interest and interactions of that indicator with indicators for each of the three acquisition types (all-stock, mixed, and all-cash).Footnote 14 To the extent that each proxy variable captures the extent of agency or dual adverse selection concerns, these regressions allow us to home in on the types of all-stock acquisitions driving the large increases in CEO compensation and, therefore, provide more direct evidence on the Agency and Dual Adverse Selection hypotheses. These proxy variables fall into two general categories: i) compensation and board variables that are meant primarily to measure the extent of agency concerns and ii) acquirer and deal risk variables that are meant primarily to measure the extent of dual adverse selection concerns.Footnote 15

TABLE 7 Change in CEO Compensation Within Acquisition Categories by Method of Payment

1. Compensation and Board Variables

We first consider a set of variables related to the acquirer’s compensation and board structures. Three variables quantify past CEO compensation and the associated incentives: Excess CEO compensation is an indicator variable equal to 1 if the CEO’s excess compensation in the prior year was above the median across all firms in the year.Footnote 16 CEO delta and CEO vega are estimates of the sensitivity of the CEO’s pay to changes in the firm’s stock price and volatility. They are calculated based on the methodology in Core and Guay (Reference Core and Guay2002).Footnote 17 Under the Agency Hypothesis, we expect compensation changes following acquisitions to be greater in firms with high excess compensation and low sensitivity of compensation to performance. Note that we also expect greater changes in CEO compensation following all-stock acquisitions when the sensitivity of the CEO’s prior compensation to stock price is low under the Dual Adverse Selection Hypothesis.

Our findings, reported in columns 1–3 of Table 7, indicate that for CEOs with low levels of excess CEO compensation, the increase in CEO compensation is greater in all-stock acquisition years than in nonacquisition years, all-cash acquisition years, and mixed acquisition years; however, this does not hold for CEOs with high levels of excess CEO compensation. Footnote 18 These results are inconsistent with the Agency Hypothesis in which entrenched CEOs and weak boards use stock acquisitions to increase CEO compensation because we expect high, not low, levels of excess CEO compensation before the acquisition for entrenched CEOs and weak boards. Although one potential explanation for this finding might be that firms with low excess compensation are simply reverting to the mean, such an explanation is inconsistent with the fact that we observe this result only in all-stock deals, but not in all-cash or mixed deals.

For CEOs with low levels of CEO delta (CEO vega), we find that the increase in CEO compensation is greater in all-stock acquisition years than in nonacquisition years and all-cash acquisition years; again, however, this does not hold for CEOs with high levels of CEO delta (CEO vega). These results suggest CEOs with low exposure to firm stock price and volatility receive greater increases in compensation for all-stock acquisitions. Combining these results with the earlier finding that the increase in CEO compensation related to all-stock acquisitions comes primarily through equity-based compensation, this is consistent with acquiring firms bonding the CEO to the acquisition when CEOs with low exposure to firm risk pursue all-stock acquisitions. These findings support the Dual Adverse Selection hypothesis.

We provide further evidence on the Agency Hypothesis by analyzing two variables that are commonly used measures of board monitoring and CEO entrenchment: Fraction of directors after CEO is the fraction of directors that were appointed to the board during the CEO’s tenure (co-opted directors). The data, from Coles, Daniel, and Naveen (Reference Coles, Daniel and Naveen2014), span 1996 to 2014. Classified board is an indicator variable equal to 1 if elections to board seats are staggered across years. The variable is downloaded from the Institutional Shareholder Services governance database.

Under the Agency Hypothesis, we expect greater increases in CEO compensation following all-stock acquisitions when the fraction of co-opted directors is high and if the acquirer has a classified board. Contrary to these predictions, however, our findings in columns 4 and 5 of Table 7 indicate that for firms with low levels of fraction of directors after CEO the increase in CEO compensation is greater in all-stock acquisition years than in nonacquisition years, all-cash acquisition years, and mixed acquisition years; however, this does not hold for CEOs with high levels of fraction of directors after CEO. The finding that the increases in CEO compensation for all-stock acquisitions is focused in firms with low board capture is not consistent with the Agency hypothesis, which predicts captured boards are more likely to acquiesce to CEO demands for higher compensation. Further inconsistent with the Agency Hypothesis, we find no evidence that CEO compensation changes are greater in firms with Classified boards regardless of the method of payment. The bottom line, therefore, is that proxy variables for potential agency problems have little explanatory power for postacquisition changes in CEO compensation.

2. Acquirer and Deal Risk Variables

To provide evidence on the Dual Adverse Selection hypothesis, we test whether changes in CEO compensation following all-stock acquisitions are greater in deals in which we expect greater adverse selection concerns. To proxy for the risk of acquirer overvaluation, we use two variables. The first is an indicator variable, Investment grade, that is equal to 1 if the firm has an investment grade rating and zero if the acquirer’s debt is either unrated or it has a noninvestment grade rating.Footnote 19 The variable is downloaded from the Institutional Shareholder Services governance database. Following the logic of prior studies that analyze the impact of financial constraints (see, for example, Whited (Reference Whited1992), Almeida, Campello, and Weisbach (Reference Almeida, Campello and Weisbach2004), and Denis and Sibilkov (Reference Denis and Sibilkov2010)), we assume that noninvestment grade and unrated firms are riskier than investment grade firms and have greater asymmetric information. The second is an indicator variable that is equal to 1 when the industry median market-to-book ratio for a given year is greater than the median market-to-book for that industry across all sample years. We define industry using the Fama–French 48 classifications. We assume that the risk of acquirer overvaluation is greater when the industry market-to-book ratio is above median than when it is below median.

Under the Dual Adverse Selection Hypothesis, we expect greater increases in CEO compensation following all-stock acquisitions when acquirer risk is high. Our findings in columns 6 and 7 of Table 7 are consistent with this prediction. Changes in CEO compensation following all-stock acquisitions are significantly larger in acquisitions for which the acquirer has either unrated or noninvestment grade debt than in deals with acquirers with investment grade debt, and in years in which the industry median market-to-book ratio is above the median for that industry. Also consistent with the Dual Adverse Selection hypothesis, the impact of acquirer risk on the postacquisition change in CEO compensation is only observed in all-stock acquisitions.

To proxy for the riskiness of the acquisition, excess change implied volatility measures the market’s perception of the change in the expected risk of the acquiring firm over the fiscal year. It is calculated as the market adjusted change in the implied volatility of the 1-year at-the-money option (the average of the call and put option) from the end of the fiscal year just prior to the acquisition to the end of the current fiscal year following the acquisition.Footnote 20 Under the Dual Adverse Selection Hypothesis, we expect greater increases in CEO compensation following stock acquisitions when the riskiness of the acquisition is high. Footnote 21 Consistent with this prediction, our findings in column 8 of Table 7 indicate that the postacquisition change in CEO compensation in all-stock deals is significantly larger for acquirers with an above-median value of excess change implied volatility. Again, this result is not observed for all-cash or mixed deals.

3. Alternate Specifications

Our analysis in Table 7 covers all firm-years and compares changes in compensation in acquisition firm-years with nonacquisition firm-years across different methods of payment. As a result, the explanatory variables that we use are limited to variables that can be computed for both acquisition and nonacquisition firm-years. In Table IA6 in the Supplementary Material, we consider an alternative specification in which we limit the analysis to acquisition firm-years only and test whether the difference in postacquisition changes in CEO compensation between all-stock and cash/mixed acquisitions is related to variables that proxy for agency and dual adverse selection concerns.

While this approach reduces our sample size, it allows us to test the robustness of our inferences from Table 7 to the alternate specification and alternative proxy variables. Specifically, in addition to the proxy variables used in Table 7, we consider one additional measure of acquirer risk, Stdev mkt-adj return, and two additional measures of deal risk, Abs(DGTW abret) and Change stdev. Stdev mkt-adj return is the standard deviation of the difference between the daily firm return and the market return calculated over the 1-year period prior to the acquisition announcement. Abs(DGTW abret), an ex post measure of the realized uncertainty in the acquisition, is the absolute value of the DGTW-adjusted buy and hold return for the acquirer in the 12-month period after the acquisition announcement using the technique of Daniel, Grinblatt, Titman, and Wermers (Reference Daniel, Grinblatt, Titman and Wermers1997). Abs(DGTW abret) is thus a proxy for the magnitude of the change in the market’s perception of the acquisition’s value during the 1-year period after the initial announcement of the acquisition. Change stdev is the difference in the daily standard deviation of returns of the acquirer from the 1-year period prior to the announcement to the 1-year period after the acquisition announcement.

As shown in Table IA6 in the Supplementary Material, our results are largely robust to this alternative specification and to the use of different proxy variables for acquirer and acquisition risk.Footnote 22 First, the difference in postacquisition changes in CEO compensation between all-stock and cash/mixed deals are not greater in deals for which the acquirer has above-median measures of agency concerns (see models 1–5 of Table IA6 in the Supplementary Material), but the difference is greater for deals with low CEO exposure to the stock price and volatility. Second, greater acquiring firm risk is associated with greater increases in CEO compensation for all-stock acquisitions (models 6–8). Finally, we observe greater increases in CEO compensation for all-stock acquisitions when the risk of the acquisition is greater (models 9–11).Footnote 23

4. Cross-Sectional Variation in Changes in the Components of CEO Compensation

Recall that in our earlier findings, we find that postacquisition changes in CEO compensation are driven primarily by changes in equity-based compensation, whereas there is little change in salary and bonus. In this section, we further extend our analysis of the reduced sample of acquisition firm-years to test whether this finding is related to variables that proxy for agency and dual adverse selection concerns. These findings are reported in Table IA7 in the Supplementary Material.

Using the alternative proxy variables that measure agency concerns described earlier, we continue to find little support for the Agency Cost Hypothesis in that there is little evidence that postacquisition changes in compensation (particularly equity-based compensation) are greater in acquisitions for which there are likely to be greater agency concerns. By contrast, there is strong support for the Dual Adverse Selection Hypothesis in that, for all three measures of acquisition risk and two of the three measures of acquirer overvaluation risk, we find increases in CEO equity compensation are greater in all-stock acquisitions. Moreover, the results indicate the increase in equity compensation is exclusive to acquisitions with above median risk. Notably, this is not the case for changes in salary and bonus. Collectively, therefore, our findings indicate that all-stock acquisitions are associated with greater compensation, particularly in high-risk acquisitions, and the greater compensation in high-risk acquisitions comes in the form of equity compensation.

C. Are Targets Aware of Compensation Changes When They Approve Acquisitions?

The Dual Adverse Selection Hypothesis posits that increases in equity-based pay bond the CEO to the postacquisition stock price and, therefore, mitigate target firm concerns about overvalued equity. In order for this to be true, it is critical that the acquirer is able to make a credible commitment to the target that the postclosing compensation changes will take place. Unfortunately, we do not observe when the target learns of the compensation changes so we have no direct evidence that this credible commitment occurs.Footnote 24 Therefore, in the Supplementary Material, we report the results of two additional tests that provide indirect evidence on this issue by identifying subsamples of our data in which it is more likely that targets are aware of the changes in acquirer CEO compensation.

First, for a random sample of 100 firms announcing acquisitions between 2006 and 2018, we manually collect the date on which the acquiring firm makes compensation grants to the CEO. We find that 63% of grants are made in the first 2 months of the fiscal year. Extrapolating this small sample evidence to our full sample, we conjecture that the likelihood of the target knowing about the planned postacquisition changes in compensation is substantially greater if the acquisition is announced after the first 2 months of the fiscal year. Thus, if postacquisition changes in compensation for stock acquisitions are a response to dual adverse selection concerns, they should be greater for acquisitions announced after the first 2 months of the year.Footnote 25 Consistent with this prediction, we find no evidence of significant changes in compensation following stock acquisitions announced in the first 2 months of the fiscal year (Table IA8 in the Supplementary Material). By contrast, stock acquisitions announced after the first 2 months of the fiscal year are associated with significant increases in compensation. Notably, these differences across the fiscal year are not present in cash or mixed payment deals, nor are they present for withdrawn acquisitions.Footnote 26

Second, we exploit the fact that a large number of acquisitions are accompanied by a change in acquirer CEO in the same year. We hypothesize that when the CEO change is announced prior to or in conjunction with the acquisition, it is more likely that the target is aware of the transition and, therefore, aware of planned postacquisition CEO compensation. Thus, if postacquisition changes in compensation for stock acquisitions are a response to dual adverse selection concerns, they should be greater for acquisitions in which there is a change in CEO, particularly if that change is announced prior to the acquisition.Footnote 27 Consistent with this prediction, we find that compensation changes following stock acquisitions are significantly larger in stock acquisitions in which there is a change in CEO than in stock acquisitions for which there is no change in CEO (Table IA9 in the Supplementary Material). Moreover, the increase in compensation for stock acquisitions with CEO changes is limited to those acquisitions in which the CEO change is announced prior to the announcement of the acquisition. Again, these patterns are observed only in stock acquisitions; they are not observed in cash or mixed payment deals, nor in withdrawn acquisitions.Footnote 28

D. Is the Certification of Acquirer Stock Value Credible?

The Dual Adverse Selection Hypothesis predicts that acquiring companies boost the equity-based component of CEO pay in order to credibly certify that the acquirer’s stock price is not overvalued. An alternative view, however, is that acquirers use all stock as the method of payment when they perceive their equity to be overvalued. The board then awards the acquiring firm CEO more equity-based compensation because their current holdings are likely to decline in value. Although this single-sided adverse selection argument cannot explain our cross-sectional findings, it potentially can explain the observed increase in equity-based pay for CEOs following acquisitions.

To provide evidence on these alternative views, we calculate abnormal returns over two event windows: i) the 3 days centered on the announcement of the acquisition and ii) the interval extending from 1 month prior to the acquisition announcement through 12 months following the acquisition. We compute standard abnormal returns over the short event window and DGTW abnormal returns over the long event window. We then estimate regressions of these abnormal returns on Increase in CEO equity compensation dummy, an indicator variable equal to 1 if CEO equity-based compensation increased and 0 otherwise, along with the interaction of this variable and indicators for All-stock acquisitions and Mixed acquisitions, respectively. We also add controls for the log of total assets, firm age, the market-to-book ratio, the prior year’s stock return, the acquirer’s return on assets, an indicator variable denoting a change in CEO, and the relative size of the acquisition.

Under the Dual Adverse Selection Hypothesis, we expect increased equity-based compensation to mitigate the negative stock price reaction typically associated with all-stock acquisitions. However, because it is unclear when the market learns of the changes in compensation due to the delay in public reporting until after the fiscal year end, we are agnostic as to whether this information will be incorporated into prices at the time of the acquisition announcement or sometime subsequent to the announcement. By contrast, the alternative hypothesis predicts that greater increases in equity-based pay will be associated with lower returns because they signal greater overvaluation.

The results, presented in Table 8, indicate that announcement period CARs are unrelated to changes in CEO compensation. However, we find that DGTW returns over months −1 to +12 are positively associated with an increase in equity-based pay for all-stock acquisitions (F-test 1), but not for all-cash acquisitions (coefficient on Increase in CEO equity compensation dummy). DGTW returns are also positively associated with an increase in equity-based pay for mixed acquisitions (F-test 2), but the estimate is less than half the size of the estimate for the all-stock acquisitions. These findings support the Dual Adverse Selection Hypothesis, but are counter to the hypothesis that firms boost the pay of CEOs to compensate them for expected declines in the value of their equity holdings.

TABLE 8 Returns and an Increase in CEO Equity-Based Compensation

E. Do Acquirers Use Increased Stock Compensation to Certify Acquisition Quality Prior to Shareholder Vote?

Although our findings consistently support the Dual Adverse Selection Hypothesis, an alternative explanation for the increase in equity-based compensation following stock acquisitions is that acquirers might seek to certify the quality of the proposed acquisition prior to a shareholder vote. For firms listed on the NYSE, AMEX, or NASDAQ exchanges, shareholders are required to vote their approval for acquisitions involving intended stock issuance that is greater than 20% of outstanding shares.Footnote 29 By increasing the CEO’s “skin-in-the-game” through increases in equity-based pay, the board of the acquirer provides shareholders with some assurance that the acquisition on which they are voting is value increasing. Under this explanation, therefore, increases in equity-based compensation following acquisitions will be concentrated in those acquisitions on which shareholders are required to vote—that is, those for which the increase in shares issued is greater than 20%.

To provide evidence on this alternative explanation, we replicate our findings from Tables 4 and 5 after separating the all-stock acquisitions into those for which the relative size of the acquisition is greater than 20% and those that are between 5% and 20%. The results, reported in the Supplementary Material (Table IA10), indicate that both changes in total compensation and changes in equity-based compensation following all-stock acquisitions are no greater in the >20% acquisitions than in the 5%–20% acquisitions. Thus, while we cannot rule out some role for prevote certification of acquisition quality in explaining increases in equity-based compensation following acquisitions, such certification does not appear to be a primary motivation.

VI. Conclusion

We report novel descriptive evidence about CEO compensation changes around acquisitions. Specifically, we find that previously documented increases in CEO compensation following acquisitions are limited to stock financed acquisitions and are driven by changes in equity-based compensation. Our further analysis of the cross-sectional variation in these compensation changes yields little support for traditional agency–cost explanations in which entrenched CEOs pursue stock financed acquisitions to bypass market scrutiny while building their empire. Our findings are broadly consistent, however, with postacquisition compensation increases representing an endogenous contracting solution to a two-sided adverse selection problem that is unique to stock deals.

We acknowledge several caveats to this interpretation. First, we lack direct evidence that acquirers purposefully make changes to CEO compensation to alleviate the target’s adverse selection concerns and that targets are aware of these changes when agreeing to the acquisition. However, we do report results from two independent tests that support the inference that compensation increases following stock acquisitions are substantially greater when it is more likely that the target is aware of the planned compensation changes.

Second, although the Dual Adverse Selection Hypothesis posits that acquirers in all-stock acquisitions credibly signal their lack of overvaluation by increasing the CEO’s exposure to the firm’s stock price, we do not observe the counterfactual of what the level and composition of CEO compensation would have been in the absence of the sample acquisitions. Thus, we cannot say with certainty that the motive for the observed shifts in compensation following stock acquisitions is to credibly bond the CEO to the acquirer’s stock price. However, the fact that increases in equity-based compensation are associated with higher acquirer abnormal returns provides indirect evidence that the market indeed views the signal of CEO bonding as credible.

Third, although we find little evidence in support of the Agency Hypothesis in the cross section, we cannot reject the possibility that agency considerations play some role in observed compensation changes following acquisitions and that our tests identify the net effect of agency and adverse selection considerations.

Finally, even if we can conclude that dual adverse selection considerations are the dominant influence on observed compensation changes following acquisitions, we cannot conclude that such changes necessarily represent the most efficient solution to the adverse selection problem. Our findings are conditioned on the choice of method of payment. It is possible that the method of payment choice itself is a more efficient solution, in general, to the dual adverse selection problem as in Eckbo et al. (Reference Eckbo, Makaew and Thorburn2018), and that what we observe is the influence of dual adverse selection considerations after that choice has been made.

Nonetheless, we believe that our collective findings are best explained by the endogenous contracting explanation of compensation changes articulated in the Dual Adverse Selection Hypothesis. At a minimum, our findings considerably narrow the scope for possible alternative explanations of observed compensation changes following acquisitions. Any alternative would need to explain why such changes are limited to stock acquisitions, why the changes primarily take the form of increases in equity-based pay, and why the changes are larger for acquirers with greater overvaluation risk, in riskier acquisitions, in acquirers whose CEOs have low previous exposure to the stock price, and in acquisitions that are announced when it is more likely that the target is aware of the planned compensation changes. While the Dual Adverse Selection Hypothesis offers a unified explanation for this collective set of our findings, we are unaware of any alternatives that are capable of doing so.

Appendix. Variable Definitions

Compensation Variables (Execucomp)

- Chg CEO compensation

-

Change in total CEO compensation from the prior year divided by the prior year compensation and is winsorized at the 1st and 99th percentiles.

- Chg salary

-

Change in CEO salary from the prior year divided by the total CEO compensation from the prior year and is winsorized at the 1st and 99th percentiles.

- Chg bonus

-

Change in CEO bonus from the prior year divided by the total CEO compensation from the prior year and is winsorized at the 1st and 99th percentiles.

- Chg equity

-

Change in CEO equity-based compensation from the prior year divided by the total CEO compensation from the prior year and is winsorized at the 1st and 99th percentiles.

- Chg stock

-

Change in CEO stock compensation from the prior year divided by the total CEO compensation from the prior year and is winsorized at the 1st and 99th percentiles.

- Chg options

-

Change in CEO options compensation from the prior year divided by the total CEO compensation from the prior year and is winsorized at the 1st and 99th percentiles.

- Chg other

-

Change in CEO other compensation from the prior year divided by the total CEO compensation from the prior year and is winsorized at the 1st and 99th percentiles.

- Increase in CEO equity compensation dummy

-

Indicator variable equal to 1 if the equity component of the CEO’s compensation increased in the year of the announcement.

Acquisition Variables (SDC)

- 5% Acquisition

-

Indicator variable equal to 1 if the firm announced an acquisition in which the acquisition value was at least 5% of the market value of equity of the acquirer.

- All-stock

-

Indicator variable equal to 1 if the form of payment for the announced acquisition was at least 95% equity and equal to 0 for all other 5% acquisition years.

- All-cash

-

Indicator variable equal to 1 if the form of payment for the announced acquisition was at least 95% cash and equal to 0 for all other 5% acquisition years.

- Mixed

-

Indicator variable equal to 1 if the form of payment for the announced acquisition was neither a 95% equity acquisition nor a 95% cash acquisition.

Firm Characteristics (Compustat, CRSP, Execucomp)

- Assets

-

Prior year assets for the firm (denoted in $millions).

- Log assets 2004

-

Logged value of the prior year assets for the firm.

- Firm age

-

Number of years since the firm was listed on CRSP.

- CEO age

-

Age of the CEO.

- Market-to-book

-

Prior fiscal year-end ratio of the market value of assets divided to the book value of assets and is winsorized at the 1st and 99th percentiles.

- Prior year return

-

Buy and hold return for the stock over the prior fiscal year.

- ROA

-

Return on assets at the end of the prior fiscal year and is winsorized at the 1st and 99th percentiles.

- Change in CEO

-

Indicator variable equal to 1 in years there was a change in CEO.

- Industry

-

Fama–French 48 industries.

- Relative size

-

The acquisition value divided by the MVE of the acquiring firm.

CEO Prior Compensation Variables

- Excess CEO compensation

-

Indicator variable equal to 1 if the CEO’s excess compensation in the prior year was above the median across all firms in the year. Excess compensation is the residual from a regression of CEO compensation on log of firm sales, firm market-to-book, prior year return on the firm’s stock, firm ROA, CEO tenure, and an indicator variable equal to 1 if the CEO is at least 60 years old. The regression includes industry-year fixed effects.

- CEO delta

-

Estimates of the CEO’s exposure to changes in the firm’s stock price. It is calculated based on the methodology in Core and Guay (Reference Core and Guay2002) and is winsorized at the 1st and 99th percentiles.

- CEO vega

-

Estimates of the CEO’s exposure to changes in the firm’s stock price volatility. It is calculated based on the methodology in Core and Guay (Reference Core and Guay2002) and is winsorized at the 1st and 99th percentiles.

Acquirer Board Variables

- Fraction of directors after CEO

-

The fraction of directors that were appointed to the board during the CEO’s tenure. The data are from Coles, Daniel, and Naveen (Reference Coles, Daniel and Naveen2014) and cover 1996 to 2014.

- Classified board

-

Indicator variable equal to 1 if elections to board seats are staggered across years. The data are from the Institutional Shareholder Services governance database.

Acquirer Risk Variables

- Investment grade

-

Indicator variable equal to 1 if the firm has an investment grade rating and zero if it is unrated or has a noninvestment grade rating. The data are from the Institutional Shareholder Services governance database.

- Industry yearly M/B

-

Indicator variable equal to 1 if the industry median market-to-book ratio for a given year is greater than the median market-to-book for that industry across all sample years.

- Stdev mkt-adj return

-

Standard deviation of the difference between the daily firm return and the market return calculated over the 1-year period prior to the acquisition announcement.

Acquisition Risk Variables

- Abs(DGTW abret)

-

Absolute value of the DGTW adjusted buy and hold return for the acquirer in the 12-month period after the acquisition announcement using the technique of Daniel, Grinblatt, Titman, and Wermers (Reference Daniel, Grinblatt, Titman and Wermers1997) and is winsorized at the 1st and 99th percentiles.

- Excess chg imp vol (Optionmetrics):

-

Market adjusted change in the implied volatility of the 1-year at-the-money option (the average of the call and put option) from the end of the prior fiscal year to the end of the current fiscal year.

- Change stdev

-

Difference in the daily standard deviation of returns of the acquirer from the 1-year period prior to the acquisition announcement to the 1-year period after the acquisition announcement.

Acquisition Related Returns

- CAR (1,+1)

-

Acquiring firms cumulative abnormal return based on the market model in the 3-day announcement period window (day −1 to +1).

- DGTW abret (−1 to +12)

-

DGTW abnormal return over the period 1 month before the acquisition announcement to 12 months after the acquisition announcement.

Supplementary Material

To view supplementary material for this article, please visit http://doi.org/10.1017/S002210902510255X.

Funding statement

We are grateful for the support of the Institute for the study of Free Enterprise.

Open access

Open access