Introduction

The World Commission on Environment and Development (WCED) was created by the United Nations in 1983 to address growing concern about the accelerating deterioration of the human environment and natural resources and its consequences for economic and social development.1 In its 1987 report, Our Common Future, the WCED coined the most-often-quoted definition of sustainable development as the “development that meets the needs of the present without compromising the ability of future generations to meet their own needs.” This definition placed equity across generations and over time at the core of economic development.

Scholarship inspired by the WCED report focused on unpacking the elements of sustainable development, identifying its drivers and barriers, and ascertaining the role of business in addressing the global social and environmental challenges in this domain. For example, in 1989, Karl-Henrik Robèrt, a Swedish oncologist, translated the WCED definition into four system conditions for sustainability via the Natural Step Framework. These conditions called for eliminating humanity’s contribution to (i) the progressive buildup of substances extracted from the Earth’s crust, (ii) buildup of chemicals and compounds, (iii) physical degradation and destruction of nature and natural processes, and (iv) conditions that undermine people’s capacity to meet their basic human needs (Natural Step, n.d.).

The central elements of sustainable development as proposed by WCED and the Natural Step Framework are fairly similar. However, these macro systems concepts are easier to visualize at a global, national, or a societal level, but are much more difficult to operationalize, measure, and implement at the firm level of analysis that is the central focus of most strategy and organizational scholars. Unpacking the elements of the WCED definition, however, provides some guidance for operationalization at the firm level of analysis. The definition calls for businesses to adopt three sustainability related principles: (i) sustainability of resource extraction – should not exceed the capacity of natural systems to regenerate resources such as forests, fisheries, soil, and clean water; (ii) sustainability of waste generation – should not exceed the carrying capacity of natural systems to absorb them; and (iii) sustainability of social equity – business activities should have a positive impact on poverty reduction, distribution of income, and human rights. Hence, this definition is relevant to the role of business in sustainable development, as defined in this monograph.

John Elkington, the founder of the consulting firm SustainAbility, coined the term triple bottom line, arguing that firms needed to measure three separate bottom lines: profits, people, and planet (Elkington, Reference Elkington1997; The Economist, 2009). Since then, the term sustainability or corporate sustainability began to distinguish a firm’s triple bottom line strategy from its traditional economic performance. The urgency and necessity of firms to consider their performance on triple dimensions of profits, people, and planet is increasingly driven by global reports of climate change, rising seas, and air and water pollution brought to the attention of organizational leadership by extensive news coverage of United Nations Conventions such as the 2015 Paris Agreement, award-winning documentaries such as An Inconvenient Truth (2006) and its sequel An Inconvenient Sequel: Truth to Power (2017), and increasing number of businesses committing to the UN’s Sustainable Development Goals (SDGs). While many business leaders and decision makers are persuaded of the need to do something meaningful to contribute to the conservation of our planet and reversing the negative trends in atmospheric destruction, the impact of such actions on the other two ‘p’s of organizational profits and people is far from clear. Thus, decision makers wrestle with uncertainty while making decisions for their firms.

In this monograph, sustainability refers to a firm’s strategy and investments intended to achieve performance on a triple bottom line; that is, generation of financial returns on investment that are satisfactory for shareholders and investors, enhancement of social justice and human welfare, and reduction of negative environmental impacts or generation of positive environmental impacts (refer to Table 1.1 for an overview of terms). Further, in order to narrow the scope of the monograph to a manageable set of literature, we focus mainly on environmental sustainability; that is, strategies, actions, and practices undertaken by business with regard to their interface with the natural environment. While we do not completely exclude discussions of social impacts of business since in several contexts (especially the emerging low-income markets) where social and environmental issues are closely intertwined, these are less central to the review and discussion.

| Macro-level concept | Sustainability | ||

|---|---|---|---|

| Triple Bottom Line Dimensions | Profits | People | Planet |

| Economic | Social | Environmental | |

| Focal Stakeholder of Interest | Shareholders / Investors | Internal Stakeholders – employees | Community, NGOs, regulators, customers, suppliers, the Earth and its natural resources (e.g., air, water, minerals) |

| External Stakeholders – community, NGOs, suppliers, customers, regulators | |||

| Success Indicators | Financial Return on Investments | Social justice, fair prices and wages, fair treatment, human welfare | Preservation and enhancement of the natural resources, habitats, species |

| Disciplinary Focus | BPS Division of the Academy of Management | SIM & OB Divisions of the Academy of Management | ONE Division of the Academy of Management |

| Finance | |||

| Commonly Used Strategies / Terms in the Literature | Corporate Philanthropy; | Corporate Social Responsibility (CSR) | Corporate Greening; |

| Impact Investing | Corporate Citizenship | Corporate Environmental Strategy (proactive vs. reactive) | |

| Firm Level Concept | Sustainable Business | ||

In academic literature, the term environmental sustainability is most frequently used in niche journals such as Business Strategy and the Environment, Greener Management International, Journal of Industrial Ecology, Organization and Environment, and Sustainable Development while the focus of corporate response and strategies on social issues is often the focus of journals such as Business and Society where the more commonly used term is corporate social responsibility, or CSR. However, its usage in strategy and management journals is more limited. In the traditional strategy literature, the term sustainable is most commonly used in reference to long-lasting competitive advantage or the “economic performance” element of the triple bottom line. In the domain of financial performance, more recently, scholarship on impact investing and corporate philanthropy has emerged. The bottom lines focused on people and the planet have gained momentum in the management literature starting in the late 1990s. Even so, to avoid empirical complexity, most academic research focuses on only one of these dimensions – people or the planet via either CSR or corporate environmental strategy.

The social and environmental research streams are largely addressed by researchers in the two divisions of the Academy of Management – Social Issues in Management (SIM) and Organizations and the Natural Environment (ONE). More recently, scholarship on the social dimension of sustainability is gaining momentum in the Organizational Behavior (OB) division (e.g., El Akremi et al, Reference El Akremi, Gond, Swaen, De Roeck and Igalens2015). While there is a great deal of overlap, each research stream tends to use different terms to refer to the elements that make up the concept of sustainability. For example, terms like CSR or corporate citizenship focus on the social dimension of sustainability; while others like corporate greening or corporate environmental strategy focus on the ecological dimension.

Two terms have been used in the literature to describe the organizational strategies focused on each of the three triple bottom line dimensions. These are Corporate Philanthropy and Impact Investing (for the profit dimension), CSR and Corporate Citizenship (for the people dimension), and Corporate Greening and Corporate Environmental Strategy (for the planet dimension). While our focus in this monograph will be to understand patient investments in proactive environmental strategies (PES) by family and non-family firms, understanding the differences between these terms is helpful in delineating the extant literature that is relevant for embedding the discussions in this monograph. Table 1.1 summarizes various terms used in the literature, sometimes without a clear separation or delineation. Following Table 1.1, we briefly elaborate on the more commonly accepted definitions or usage of each of these terms.

Key Terms in the Sustainability Literature

Corporate Philanthropy

Extant literature uses the term corporate philanthropy to describe a firm’s actions to mitigate negative social and environmental impacts. Corporate philanthropy usually refers to corporate giving or donations intended to tackle government failures in addressing social needs, problems, and challenges. A distinct stream of literature uses the term strategic philanthropy (e.g., Porter and Kramer, Reference Porter and Kramer2002; Post and Waddock, Reference Post, Waddock and America1995). This concept argues that firms can engage in philanthropy to further their strategic interests. That is, they develop a strategic plan to give away resources with nothing apparent in return in order to garner intangible benefits such as goodwill or legitimacy or license to operate. Even though strategic philanthropy is undertaken for a strategic business purpose, it does not require the firm to change its core strategy or develop goals to achieve triple bottom line performance.

Impact Investing

Since 2009, a diverse community of investors, business leaders, and researchers have coalesced to form the Global Impact Investing Network (GIIN). This nonprofit organization defines impact investments as “the investments into companies, organizations, and funds with the intention to generate social and environmental impact alongside a financial return” (GIIN, n.d.). This initiative provides an infrastructure to support the activities and research related to impact investing. While micro-level impact investing efforts at individual, household, and community levels are gaining momentum, scientific research on this topic is in early stages (e.g., Bugg-Levine and Emerson, Reference Bugg-Levine and Emerson2011). However, with the emergence of a specialized niche journal focused on related research – the Journal of Sustainable Finance and Investments – scholarly interest in this topic is expected to grow. Jackson (Reference Jackson2013) considers it as one of the most promising and creative areas of development finance.

Our interest in this monograph is to understand the factors that enable or hinder the core thinking of key decision makers regarding environmental strategies of ongoing firms rather than on how and where a business invests or spends its profits. Thus, while we acknowledge the importance of financial profitability dimension of sustainability, building related theory is beyond the scope of this monograph.

Corporate Social Responsibility (CSR)

Carroll (Reference Carroll1979: 500), provided an early conceptualization of CSR: “Corporate social responsibility encompasses the economic, legal, ethical, and discretionary (philanthropic) expectations that society has of organizations at a given point in time.” Building on this conceptualization and other definitions in the literature, El Akremi, Gond, Swaen, De Roeck and Igalens (Reference El Akremi, Gond, Swaen, De Roeck and Igalens2015) developed and validated a thirty-five-item scale to measure employees’ CSR perceptions. These authors define CSR as “an organization’s context-specific actions and policies that aim to enhance the welfare of stakeholders by accounting for the triple bottom line of economic, social, and environmental performance, with a focus on employees’ perceptions” (El Akremi et al., Reference El Akremi, Gond, Swaen, De Roeck and Igalens2015: 623). Notable progress is being made in the CSR literature to assess a firm’s legal and ethical responsibilities toward its stakeholders.

Since societal perspectives about negative impacts of business operations are constantly evolving, firms need to address a moving target. For example, from the Industrial Revolution through the thirties, child labor was a norm in a wide variety of occupations not only in the United States but in most developed countries of the time. Today, while over 200 million children are still engaged as laborers in the world, such practices are abhorred by the International Labor Organization of the United Nations. Amidst such changing expectations, the CSR literature aims to understand firm activities directed to mitigate what society deems negative or unacceptable behaviors toward its employees or the community in which it operates. This may involve investments in its own operations and/or via philanthropy. However, CSR does not necessarily imply that a firm will fundamentally change its strategy and operations to generate positive social or environmental impacts.

Corporate Citizenship

Corporate citizenship is used to describe a firm’s role in, or responsibility toward, society. Broadly, it refers to “the portfolio of socioeconomic activities that companies often undertake to fulfill perceived duties as members of society” (Gardberg and Fombrun, Reference Gardberg and Fombrun2006: 330). Since corporations are granted “the legal and political rights of individual citizens through incorporation,” they also are ascribed, explicitly and implicitly, “a set of responsibilities” (Gardberg and Fombrun, Reference Gardberg and Fombrun2006: 330). These authors provide examples of corporate citizenship as including “pro-bono activities, corporate volunteerism, charitable contributions, support for community education and health care initiatives, and environmental programs – few of which are legally mandated, but many of which have come to be expected by government hosts and local communities” (Gardberg and Fombrun, Reference Gardberg and Fombrun2006: 330). Matten and Crane (Reference Matten and Crane2005: 173) argue for a broader definition of corporate citizenship as “the role of the corporation in administering citizenship rights for individuals” indicating that the corporation is not only a citizen itself but administers citizenship for “traditional stakeholders such as employees, customers, or shareholders,” and “wider constituencies with no direct transactional relationship to the company.” Regardless of a narrower or broader definition, the term corporate citizenship includes elements of corporate action and strategy similar to CSR. It is no surprise therefore that the two terms are often used interchangeably in practice to describe a firm’s social and community initiatives. Regardless of how these terms are actually used by firms, or are defined by scholars, CSR or Corporate Citizenship do not imply that the firm will change its core operations or strategies. Usually, these terms are used to describe a firm’s practices and actions to mitigate the impacts of its operations that society deems negative.

Corporate Greening

While the terms CSR and corporate citizenship emphasize social actions and impacts, corporate greening is used to describe corporate actions to address environmental impacts of a firm’s operations. It refers to actions adopted by a firm for risk reduction, reengineering, and cost-cutting (Hart, Reference Hart1997). Thus, greening usually refers to organizational practices but rarely refers to corporate strategy, innovation, or technology development (Hart, Reference Hart1997). Like CSR and corporate citizenship, the term corporate greening describes reduced negative environmental impacts but does not imply a change in core operations or strategy to generate positive impacts. Just as societal expectations of appropriate social practices have evolved, societal expectations of environmental pollution continuously evolve. For example, societal perceptions about emissions of waste from manufacturing facilities have changed substantially over the last five decades. Visual representations such as smokestacks represented economic development in the 1950s, but they now represent air pollution in most societies across the world.

Corporate Environmental Strategy

Corporate environmental strategy refers to a firm’s strategy to manage the interface between its business and the natural environment (Aragón-Correa and Sharma, Reference Aragón-Correa and Sharma2003). Since the nineties, a significant stream of literature in ONE has emerged around corporate environmental strategy. For example, based on a comparative case study of seven companies in the oil industry, Sharma and Vredenburg (Reference Sharma and Vredenburg1998) distinguish between firms following proactive versus reactive environmental strategies. Proactive environmental strategy for a firm refers to a “consistent pattern of environmental practices, across all dimensions relevant to their range of activities, not required to be undertaken in fulfillment of environmental regulations or in response to isomorphic pressures within the industry as standard business practice” (Sharma and Vredenburg, Reference Sharma and Vredenburg1998: 733). Firms pursuing a reactive environmental strategy may comply with the prevailing laws, lobby against environmental regulation, and even excel in specific areas in reducing environmental impacts, but their focus and consistency in pursuit of environmental strategy is limited (Sharma and Vredenburg, Reference Sharma and Vredenburg1998). Proactive environmental strategy, on the other hand, implies changes in a firm’s strategy to prevent negative environmental impacts at source rather than just reducing them after the negative impacts such as pollution are generated (Russo and Fouts, Reference Russo and Fouts1997).

Sustainable Business

A sustainable business is one that has altered or developed, or is in the process of altering or developing, its strategy and operations in accordance with the principles of sustainability. These principles encompass the triple bottom line: above industry average performance on financial, social, and environmental metrics. The sustainable firm’s business model and strategy are designed to achieve not only its economic or core objectives (e.g., for a nonprofit organization, the core objective may be the delivery of health care or clean water rather than profits), but also its social and environmental performance. Hence, a sustainable business is significantly different from a firm that does not fundamentally change its business model and strategy but rather acts responsibly by adopting practices to mitigate the negative social and environmental impacts of its existing operations. As compared to the terms already discussed, sustainable business, as used in this monograph, has fundamental implications not only for business strategy but also for the core operational and business model of the firm.

It is unlikely and perhaps impossible for any organization to be completely sustainable by itself. While sustainability is a journey on which an increasing number of organizations have embarked, networks of firms are forming industrial ecosystems to use each other’s wastes so as to ensure that no pollution leaves the network. A good example of this is the Danish Klundborg Symbiosis, a partnership between eight public and private companies in Kalundborg (Denmark) that use the circular approach to production. This approach builds on the principle that a residue from one company becomes a resource for another thereby benefiting the local economy, environment, and society (for more details, please see www.symbiosis.dk/en).

Sustainability Strategy

At the firm level, a sustainability strategy aims to achieve its short-term financial, social, and environmental performance without compromising its long-term performance on these three dimensions. This means that the firm needs to create value for its stakeholders in the present while investing in strategies and resources to improve the social, environmental, and economic performance desired by its stakeholders (including its shareholders) in the future. In this process, the firm has to manage the uncertainty related to the evolving and changing definition of “value” over time for its various stakeholders (El Akremi et al., Reference El Akremi, Gond, Swaen, De Roeck and Igalens2015). Hence, the temporal orientation of the dominant coalition or the top management team of a firm becomes an important determinant in understanding its environmental strategy. Temporal orientation is the distance into the past or future that an individual or a collective considers in their cognitive processes, behaviors, and decision-making (Bluedorn, Reference Bluedorn2002).

Effectively addressing sustainability challenges by an existing business requires it to effect changes in its strategy, and perhaps also its business model and organizational design and structure. These are deep-rooted changes that may require investments in new technologies, entry into unfamiliar market segments such as lower-income markets in developing countries, and building new capabilities that may yield returns over longer term as compared to investments that firms normally make in incremental product innovations and entry into adjacent new markets. In order to build such capabilities, the strategic decision-making unit of the firm, whether the dominant coalition in family firms or the top management team in non-family firms, needs to be aligned in their vision about the firm’s future business, their values toward the role of business in environmental preservation, and need to garner the support of their critical stakeholders.

What drives firms to undertake such investments that are likely to pay back over a longer term? What factors determine the top management team’s strategic time horizon and expectations of return on investments? This monograph examines these factors within the context of ongoing businesses. While firms may also undertake investments in social sustainability initiatives, such as fair trade in its supply chain, we narrow our focus in this monograph on investments aimed to address major environmental sustainability challenges such as climate change, clean water, and renewable energy, amongst others, and refer to such investments and initiatives as a proactive environmental strategy (PES). We use the term patient capital for such long-term investments thereby distinguishing them from short-term investments.

Patient Capital

The term patient has been used in extant literature at different levels of analysis, ranging from the individual level at the perspective of an investor, to the macroeconomic or national level, but rarely at the firm level of analysis. A search of peer reviewed scholarly articles in ABI/Inform using the search terms patient and capital reveals almost no scholarly discussion of the concept. In its limited academic usage, the term is neither defined nor used consistently. The prefix patient is often used as a descriptor in the literature in association with terms other than capital and with varying interpretations. For example, “patient money” refers to research and development expenditures with uncertain outcomes undertaken by firms (Manners and Louderback, Reference Manners and Louderback1980). The term patient investor is used in theories of economic equilibrium while referring to individual investors or traders with longer-term return expectations (Grenadier and Wang, Reference Grenadier and Wang2007; Shive and Yun, Reference Shive and Yun2013).

In practitioner articles, patient capital is used in reference to foreign direct investments with long-term development objectives. However, this literature does not offer a definition. Nor does it embed the term in extant literature (Teece, Reference Teece1992). Patient capital is also used in reference to the restructuring of financial markets to avoid financial crises similar to the one experienced in 2008 (Mazzucato, Reference Mazzucato2013), and in the context of long-term orientation of companies with shared employee ownership (Fojt, Reference Fojt1995). In referring to the external sources of capital for financing not-for-profit organizations, Kingston and Bolton (Reference Kingston and Bolton2004: 114) provide a rare definition of patient capital as “the finance provided over an extended period and below market rates. For example, a loan might be given with a ten-year capital repayment holiday. A subset of patient capital is when terms are not set until there is some certainty about the prospects for the venture.” However, these authors do not refer to investments made by firms internally with long-term return expectations.

At the level of analysis of the firm, references to patient capital are very limited. Robeson and O’Connor (Reference Robeson and O’Conner2013) find in their study that firms exhibit higher innovativeness when their decision makers are engaged and supportive of these projects, and patient with the financial results from investments. In the context of family firms, patient financial capital has been argued to be a positive attribute for innovation because of the lower accountability for short-term financial results and a higher motivation to perpetuate the business for future generations (Sirmon and Hitt, Reference Sirmon and Hitt2003). Building on this idea, this monograph theorizes the conditions that encourage firms to pursue proactive environmental strategies.

Patient capital is not subject to traditional financial valuation models and challenges traditional economic theories such as the classic agency theory, which require managers to act in the best interests of the owners (which are usually equated with maximization of returns in the short term versus the long term) via transparent results that are continuously exposed to external markets for valuation purposes. For example, Keiretsus in Japan, Chaebols in Korea, and family conglomerates in India are known to deploy patient capital by cross-subsidizing projects that require longer returns with funds from high-profit-making and cash-generating businesses. In the late 1970s and through the 1980s, the Korean Chaebols were able to become serious players in dynamic random access memory (DRAM) technology, eclipsing Taiwan and other Asian powerhouses, through this strategy, even after sustaining tremendous financial pressures (Fuller, Akinwande, and Sodini, Reference Fuller, Akinwande and Sodini2003).

Some common characteristics of patient capital include (a) willingness to forgo maximum financial returns for achieving social/environmental impact, (b) greater tolerance for risk than traditional investment capital, (c) longer time horizons for return of capital, and (d) intensive support of management to grow the enterprise. The last implies that the top management team of the firm has an objective to seek long-term growth rather than short-term returns. Indeed, there is some evidence that members of family businesses may choose growth and control of business over short-term dividends or cash back and, hence, exhibit patience with investments (Oswald et al., Reference Oswald, Ghobadian, O’Regan and Antcliff2013). Hence, patient capital is not philanthropy or a grant, but an investment that foregoes short-term return for long-term growth and achievement of nonfinancial objectives such as social and environmental impacts, and control of business over generations (e.g., Meier and Schier, Reference Meier and Schier2016). Thomas Friedman states that patient capital has “all the discipline of venture capital – demanding a return, and therefore rigor in how it is deployed – but expecting a return that is more in the 5 to 10 percent range, rather than the 35 percent that venture capitalists look for” (Friedman, Reference Freidman2007, n.p.). Based on this, we adopt Wikipedia’s (n.d.) proposed working definition of patient capital as the willingness “to make a financial investment in a business with no expectation of turning a quick profit. Instead, the investor is willing to forgo an immediate return in anticipation of more substantial returns down the road.”

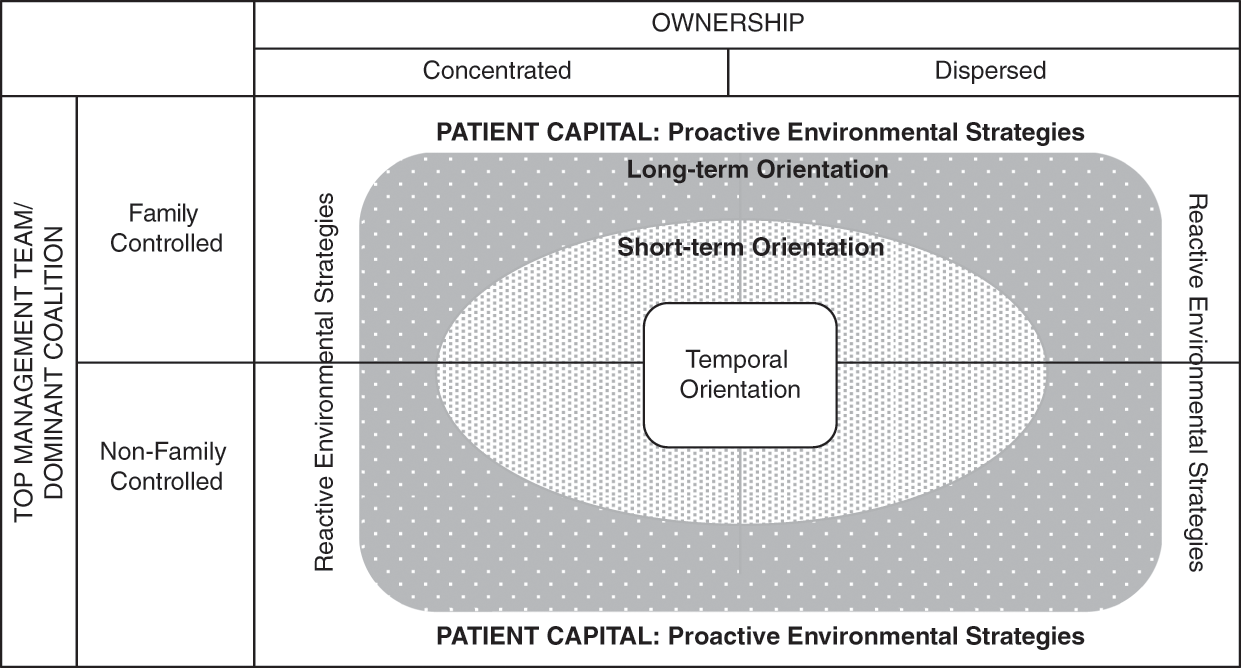

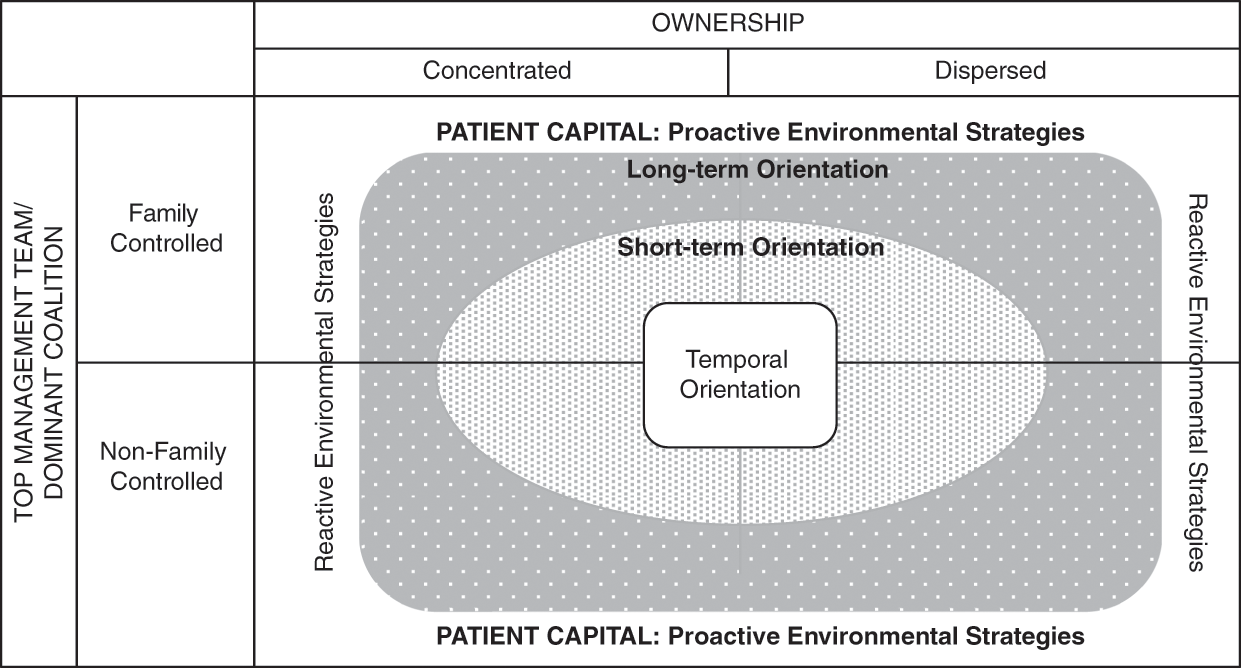

In order to examine the factors influencing investment of patient capital by firms, in this monograph, we draw on extant literature and original primary and secondary research to compare strategies and investments in sustainable practices and business models by firms operating under two different corporate governance systems: those with ownership that is concentrated vs. dispersed, and firms controlled by one or few families vs. non-family members.

Corporate Governance

Corporate governance is broadly defined as “the process and structure used to direct and manage the business affairs of the company towards enhancing business prosperity and corporate accountability with the ultimate objective of realizing long-term shareholder value, whilst taking into account the interests of other stakeholder” (Keasey, Thompson, and Wright, Reference Keasey, Thompson and Wright1997: 288). This is only one of the several broad-scope definitions from the literature as the focus of governance varies across disciplines. For example, in the economics and finance literatures, scholars relate corporate governance to capital allocation decisions within and across firms (Morck and Steier, Reference Morck and Steier2005), as their interest is on issues relating to how the suppliers of finance to corporations (owners) get a return on their investment (Shleifer and Vishny, Reference Shleifer and Vishny1997). Hence, of prime importance to this research stream are the mechanisms and controls designed to reduce or eliminate the principal-agent problem (Baker and Anderson, Reference Baker and Anderson2010; Villalonga et al., Reference Villalonga, Amit, Trujillo and Guzman2015). From this perspective, governance is treated as synonymous with ownership (Carney, Reference Carney2005; Gersick and Neus, Reference Gersick, Neus, Melin, Nordqvist and Sharma2014). For researchers in the discipline of law, corporate governance is an organizational mechanism that refers to the monitoring and control over the allocation of a firm’s resources, and the structuring and management of such relationships within a firm (McCahery and Vermeulen, Reference McCahery and Vermeulen2006). Thus, in each definition, there is varied emphasis on ownership and management dimensions.

In this monograph, our focus lies in understanding factors that enable or hinder the performance of a firm on the environmental dimension of its triple bottom line, not only in the short term, but also in the longer term. As both ownership and managerial decision-making significantly influence adoption of environmental strategies, we adopt Keasey, Thompson, and Wright’s (Reference Keasey, Thompson and Wright1997) above-mentioned comprehensive definition of corporate governance as it includes both these dimensions.

Ownership vs. Management Control

Ownership may be widely dispersed (as in publicly listed companies) or tightly controlled by a small group of individuals (as in privately held companies). The relative proportion of each of these forms of governance varies across nations. In the United States, about 1 percent of all registered companies are publicly listed. While low in number, their impact on the economy is significant and thus these companies have been subject of a large body of research not only in finance but also in strategy (VanderMey, Reference VanderMey2017). Ownership of these publicly listed companies is widely dispersed amongst many shareholders, each usually owning a few hundred to a few thousand shares and expecting short-term returns. Despite shareholder protections, these arm’s-length equity investors are largely disorganized and lack a voice in corporate boardrooms where key decisions that impact returns on their investments are made. Only investors that accumulate stakes larger than 3 to 5 percent gain a voice in the boardrooms (Morck and Steier, Reference Morck and Steier2005). These include institutional investors and firms such as Berkshire Hathaway that take major stock positions in a firm. However, such investors, while holding significant blocks of shares, do not have majority voting power in the firms they invest in. Such separation of ownership and management control grants significant power to the Chief Executive Officers (CEOs) and their top management team (TMT) to determine the strategic goals of the company (Cyert and March, Reference Cyert and March1963). As this influential group is well positioned to use (or abuse) their power according to their economic, social, and/or environmental values and beliefs, there has been significant scholarly interest in understanding the agency problems and inefficiencies caused as a consequence of separation of ownership and management roles in publicly listed firms (Chen and Smith, Reference Chen and Smith1987; Jensen and Meckling, Reference Jensen and Meckling1976). Efforts have been devoted to understanding how best to align the interests of owners and managers via incentive structures such as compensation and/or stock options related to corporate performance or monitoring systems (Jensen and Meckling, Reference Jensen and Meckling1976).

In the last few years, two significant trends have become evident. First, there has been a steady decline in the number of publicly listed firms in the United States. While there were more than 7,000 such companies in the late 1990s, this number went down to about 4,900 ten years ago, and to 3,603 in 2018. Nevertheless, today’s listed companies are larger and more stable than their counterparts in earlier decades. Second, is the important role of kinship groups or families in publicly listed firms. While earlier research had assumed that only institutional investors who could gain significant ownership stakes needed to have a strong voice in the boardrooms of public companies, more recently another important stakeholder group – kinship group i.e., members of one or a few related families – may also own significant numbers of shares to put them in an influential position on the board. In fact, both in the United States and the United Kingdom, a third of the listed companies are family controlled (Villalonga et al., Reference Villalonga, Amit, Trujillo and Guzman2015). Such control is particularly dominant in some industries like agricultural production and the livestock industry (holding 100 percent market share), the motion picture industry (with 95 percent share), automotive dealerships and service stations (with 88 percent share), hotels and other lodging businesses (79 percent share), and 60 percent in printing and publishing firms (Villalonga and Amit, Reference Villalonga and Amit2009).

In contrast to the United States and United Kingdom, in much of the rest of the world, few wealthy families exert concentrated control of large corporations and govern them with the intention of retaining this control over generations (Morck and Steier, Reference Morck and Steier2005). For example, LaPorta, Lopez-de-Silanes, and Shleifer (Reference LaPorta, Lopez-de-Silanes and Shleifer1999) contrasted the ownership of large and medium-sized publicly listed companies around the world and illustrated that a large majority of corporations in countries like Mexico, Argentina, Hong Kong, Israel, Mexico, and Sweden are family controlled.

Family-controlled firms also dominate the private sector, not only in the United States but around the world, as estimates range from 60 percent to 98 percent of all businesses in most countries (e.g., Fernández-Aráoz, Iqbal, and Ritter, Reference Fernández-Aráoz, Iqbal and Ritter2015; Shanker and Astrachan, Reference Shanker and Astrachan1996; please refer to Global Data Points @ the Family Firm Institute for the most recent data). While a large majority of small and medium businesses are family controlled, in Germany and Japan, family-controlled conglomerates characterized by long-term debt, financial ownership by large investors, weak corporate control, and rigid labor markets tend to dominate the economy (Aguilera, Reference Aguilera2005; LaPorta et al., Reference LaPorta, Lopez-de-Silanes and Shleifer1999). And, large private enterprise is on a rise as evidenced by a 2010 McKinsey & Co. study that found 60 percent of private sector companies with revenues of over $1 billion each in emerging economies were owned by founders or families. By 2025, family businesses will represent nearly 40 percent of the world’s large enterprises, up from 15 percent in 2010 (Björnberg, Elstrodt, and Pandit, Reference Björnberg, Elstrodt and Pandit2014), emphasizing the need to examine, understand, and engage this fast-growing segment of the economy in addressing sustainability challenges.

Family vs. Non-Family Control

Family firms are fundamentally different from non-family firms as the dominant coalition (DC) of these firms is formed of individuals with bonds of kinship with the next generation and are thus often managed with an eye toward long-term continuity (Chua, Chrisman, and Sharma, Reference Chua, Chrisman and Sharma1999). The US Bureau of Labor Statistics reports a decline in the median number of years a salaried employee works for one organization from 4.6 years in 2014 to 4.2 years in 2016. Regardless of their individual values and attitudes toward sustainability, managers with short stints at different organizations are less likely to leave strategic deep-rooted and long-lasting imprints at any one organization. In contrast, the average managerial tenure in long-lived family firms is at least three times higher and values held by the controlling family influence the strategic decisions of the firm (e.g., McConaughy, Reference McConaughy2000; Miller and Le Breton-Miller, Reference Miller and Le Breton-Miller2005).

In family-controlled firms, the ownership and management overlap lowers information asymmetry and the classic or Type I agency costs between owners and managers (Anderson, Mansi, and Reeb, Reference Anderson, Mansi and Reeb2003; Anderson and Reeb, Reference Anderson and Reeb2003; Bartholomeusz and Tanewski, Reference Bartholomeusz and Tanewski2006). However, family business researchers point to other forms of agency costs between majority and minority shareholders (Type II), family shareholders and family creditors (Type III), and family shareholders and family non-shareholders (Type IV). In each of these agency dualities, the costs and problems differ, as do management strategies to curtail free riding, opportunism, and entrenchment issues (e.g., Chrisman, Chua, and Litz, Reference Chrisman, Chua and Litz2004; Schulze et al., Reference Schulze, Lubatkin, Dino and Buchholtz2001; Villalonga et al., Reference Villalonga, Amit, Trujillo and Guzman2015).

Counterintuitively, some argue that formal corporate governance mechanisms aimed at monitoring non-owner or non-kin agents could have negative effects on mutual trust and intrinsic motivation based on the altruistic and cooperative behavior more common in family firms (Davis, Schoorman, and Donaldson, Reference Davis, Schoorman and Donaldson1997; Dyer, Reference Dyer2003; Karra, Tracey, and Phillips, Reference Karra, Tracey and Phillips2006). Such altruistic behavior is predicated on the stewardship of the family business to ensure the continuity and/or longevity of the enterprise and its mission, by investing in building the business for the long-run benefit of various family members. Long-term continuation of the business is paramount for the controlling family encouraging the managers and employees to focus on cooperative goals (Gomez-Mejia et al., Reference Gomez-Mejia, Haynes, Nunez-Nickel, Jacobson and Moyano-Fuentes2007; Habbershon and MacMillan, 1999; Vallejo, Reference Vallejo2009).

A combination of ownership and managerial control and long tenures of employees provides a richer context to pursue environmental strategies, the returns of which are only likely to be accrued over time. While companies governed by widely dispersed shareholders will be driven by market and competitive forces, those controlled by one or a few families through concentrated ownership and transgenerational ambitions for the company will be more likely to set longer-term expectations for profitability and social objectives (Aguilera et al., Reference Aguilera, Rupp, Williams and Ganapathi2007). While studies show a higher propensity to invest in projects and businesses with long-term payoffs, other studies have found that family-controlled firms may be more hesitant and slow in adoption of new technologies and in making riskier investments with uncertain returns, due to their sunk costs and heavy reliance on the company for financial and socioemotional returns (e.g., Gomez-Mejia et al., Reference Gomez-Mejia, Haynes, Nunez-Nickel, Jacobson and Moyano-Fuentes2007).

Although these are likely broad-brush generalizations, they provide a starting point to motivate an examination of deployment of patient capital under different governance systems in order to invest in corporate sustainability strategies and practices. Thus, in this monograph, we distinguish companies with concentrated ownership from those with dispersed ownership, as well as firms whose dominant coalition (DC) is controlled by members of one/few families from others controlled by non-family members as a top management team (TMT).

Figure 1.1 depicts an overview of the main variables that are the focus of this monograph, temporal/time orientation of business, concentration of ownership (concentrated or dispersed) and patient capital investments in long-term initiatives and projects necessary for a proactive environmental strategy (PES). Given the early stage of research at the interface of corporate environment sustainability and family business, our focus in the monograph is mainly on the two pure cases: non-family firms with dispersed ownership with top management teams of professional managers not related by kinship; and family firms with concentrated ownership with a dominant coalition controlled by family members. While we acknowledge there will be other combinations with less intense influence of professional non-kin managers or family members on ownership and management dimensions of a firm, we leave those categorizations for further finer-grained theory development and empirical analysis.

Layout of the Monograph

In the next chapter, we outline our research design and the data collected to support our theory development. The primary data were collected from family-owned and non-family owned wineries in different institutional contexts: Canada, France, and Chile. The next three chapters review the extant literature on the drivers and barriers to proactive environmental sustainability. These drivers and barriers are broadly classified at three levels: institutional/stakeholder, organizational, and individual/managerial. Chapter 3 reviews and summarizes the institutional and stakeholder drivers and barriers that influence a firm’s adoption of an environmental strategy and examines if family-owned businesses respond differently than companies with dispersed ownership to institutional and stakeholder influences and forces. Chapter 4 focuses on the differences between family owned and non-family firms on corporate governance and ownership, decision-making coalition (DC vs. TMT), organizational drivers and barriers such as organizational structure and design, and market and competitiveness drivers including organizational resources and capabilities. Chapter 5 examines the role of individuals as employees and managers who interpret the business environment (including environmental issues as they evolve), and develop and implement strategy, and the cognitive biases that shape such decision-making. We examine the differences between family firms and non-family firms in motivating employees and managing their cognitive biases by creating opportunity frames that can stimulate and catalyze innovation. During our discussion in Chapters 3 to 5, while we draw upon the literature in corporate sustainability, strategy, organizational behavior, and family business, we illustrate and support our theoretical discussions with primary data from the winery industry and also draw upon other case examples of family-owned businesses. In Chapter 6, we discuss implications of our analysis and our findings in terms of how family firms differ from non-family firms in developing and implementing a proactive environmental strategy in responding to exogenous forces and in their values, organizational design, and capabilities. We conclude with a research agenda for scholars examining environmental sustainability strategy, innovation, and strategic decision-making processes of family and non-family firms. We also discuss what non-family firms can learn from family firms in developing a proactive environmental strategy and vice versa. By bringing research issues of environmental sustainability into family firms, we provide insights for a dominant sector of the economy (family firms), and by bringing insights from family firms into extant sustainability literature, we offer thoughts for finer-grained, process-oriented research studies that account for corporate governance and ownership concentration in the sustainability literature.