Introduction

Societal ageing and changing economic environments have stirred up several discussions on the fiscal sustainability of the state and the employers’ ability to meet pension obligations. Consequential changes in the public and private pension landscape have fundamentally transformed how individuals save for retirement. In Britain, the flat-rate new State Pension (nSP) was introduced in 2016 without the earnings-linked portion, which indicates that the state now plays a reduced role in accumulating and providing retirement income. The gap created by the removal of the earnings-linked portion is expected to be filled by increasing private pension saving, which includes workplace pension schemes as well as an individual's own planning. Most workplace pension schemes, however, now offer Defined Contribution (DC) schemes to new employees instead of Defined Benefit (DB). The risk-bearing structure between the two schemes differ substantially: DB scheme holders are entitled to an agreed level of income for the entire duration of retirement, while DC schemes holders are not. Employers still contribute to the DC schemes but do not have any obligation to ensure neither the certainty nor continuity of retirement income. These changes in the pension landscape have an important implication for individuals: they now carry a greater responsibility in saving for their retirement. Therefore, those who would like more than modest means in retirement are strongly encouraged to save more for their retirement, from earlier on and via various means (Pensions Commission, 2004, 2005).

The current architecture of the British pension system calls for more active saving from individuals. It has become crucial to understand one's retirement saving outside the state or workplace pension schemes that occur automatically (Danzer et al., Reference Danzer, Disney, Dolton and Bondibene2016), which this study refers to as discretionary retirement saving. This type of saving is particularly important for the younger half of the working-age population, as they are saving under the new pension policy structure. Despite an increasing number of studies on young British adults’ retirement saving behaviour (Foster, Reference Foster2017; Robertson-Rose, Reference Robertson-Rose2019; James et al., Reference James, Price and Buffel2020), evidence on discretionary saving is scarce. This study, therefore, raises the following questions: If the younger adults are expected to save more for their retirement and make additional provisions, who is saving for retirement beyond the formal arrangements and who is not? How do they differ in terms of their attitudinal and behavioural characteristics related to retirement saving and, if so, to what extent? While this study examines the British context, these questions are also relevant to other societies that have a comparable pension policy or are moving towards one, with an increasing emphasis on the individuals’ responsibility for retirement saving.

This study focuses on discretionary retirement saving among British adults in their thirties and forties by identifying everyday saving activities (i.e. using a bank account) and connecting it to their retirement saving motivation. Discretionary retirement savers are those who reported to have acted on their own initiative, outside the mandatory or automatic saving schemes. Thus, the main motivation of this paper is to establish a model for a decision-making process that helps to distinguish discretionary retirement savers and non-savers. In doing so, this study focuses on testing two hypotheses, taking the lifecourse perspective. First, it examines the role of attitudinal and behavioural characteristics (internal) in identifying discretionary retirement savers in relation to socio-economic factors (external). More specifically, it tests whether having information on how individuals’ tendency to organise their financial affairs and provision for future uncertainty today, termed financial resilience, adds to the model. The second hypothesis focuses on how and to what extent the social and economic arrangements help to explain individuals’ attitudinal and behavioural characteristics. Given the age group of the study population, it explores whether social ageing, which refers to individuals’ stages of life and stability reflected in the socio-demographic and economic characteristics, contributes to understanding younger adults’ discretionary retirement saving.

The decision-making process is mapped based on the Model of Financial Planning (Hershey et al., Reference Hershey, Jacobs-Lawson, McArdle and Hamagami2007), which is modified to examine discretionary retirement saving for British adults in their thirties and forties. Financial resilience is added to the model to account for today's financial behaviours. In addition to household income, home-ownership and intergenerational transfers are also included in the model to provide a more complete picture of British younger adults’ economic circumstances today.

The analysis is cross-sectional and performed in the structural equation modelling (SEM) framework. It uses the fourth wave of the Wealth and Assets Survey (WAS) carried out between July 2012 and June 2014, as it contains the survey questions about the rollout of automatic enrolment (AE) (October 2012) relevant to this study. The analytical sample includes those who are employed, as pension-saving rules are different for self-employed individuals.

Results show that younger adults’ retirement saving is an outcome of an interplay between internal and external factors, and that the under-saving issue cannot be explained by a lack of ability or willingness alone. Financial resilience is found to be the strongest predictor for identifying a discretionary retirement saver, controlling for other variables, pointing to the importance of accounting for individuals’ current financial behaviour and financial wellbeing in planning for the long term. The findings, however, also show that financial resilience is closely associated with home-ownership and income. In addition, the propensity to have thought about saving for retirement is correlated with these two factors as well as the receipt of intergenerational transfers. These findings suggest that social ageing may be more informative than chronological ageing in studying younger adults’ retirement saving.

This paper is structured as follows. First, it describes the current British pension landscape from the younger generation's perspective and discusses the implications. Then, it introduces the lifecourse approach and the Model of Financial Planning. It continues with a literature review on individuals’ internal qualities, demographic and socio-economic factors that are included in the modified version of the Model of Financial Planning (Hershey et al., Reference Hershey, Jacobs-Lawson, McArdle and Hamagami2007), followed by an explanation of data and analytical procedures. Finally, the results are discussed before concluding with a discussion on policy implications.

Retirement saving for the younger generation in Britain

Recent developments in the pension landscape in Britain

The roles that the state and employers played in accumulating and generating retirement income have reduced since the 2000s. The focus of the British State Pension is on the redistributive social insurance function based on Beveridgean principles (e.g. Hills, Reference Hills2004) rather than achieving a specific target replacement ratio. Receipt of a pension income under the nSP, introduced in April 2016, still depends on National Insurance Contribution (NIC) records through taxation, which requires 35 years for full entitlement for both men and women.Footnote 1 On the one hand, a wider range of National Insurance credits is available, and individuals now accumulate entitlement on their own (independent of a partner's NIC record), although a minimum of a ten-year contribution is required.Footnote 2 These changes increase the certainty of a retirement income, particularly for those with short or interrupted employment patterns. On the other hand, the earnings-linked portion of the State Pension is now removed in the nSP, and a greater NIC amount will not provide additional income, unlike under the previous system. As a result, the State Pension has become more redistributive (Department for Work and Pensions (DWP), 2016); however, individuals who would like more retirement income will still need to save more via work or by making additional provisions.

Changes in the workplace pension schemes clearly point to an increased level of uncertainty and complexity for individuals. Most employers now have either shifted from DB to DC schemes or changed the calculation method. In the private sector, only 12 per cent of employees were active members of DB schemes in 2012, compared to 38 per cent in 1997 (Cribb and Emmerson, Reference Cribb and Emmerson2016). The public sector in Britain still offers DB schemes, but the changes in the indexation and entitlement method have reduced their value substantially. The average value of a public DB scheme accrued for a year has decreased in value from 26 per cent of an employee's annual salary to 11 per cent (Cribb and Emmerson, Reference Cribb and Emmerson2016). Although historically it has generated a more stable, often larger, retirement income than the average DC scheme, it would be unwise to expect that a DB scheme entitlement addresses the concerns for retirement income sufficiency.

More individuals are saving through AE. The DWP (2017) has estimated that over 9 million individuals are saving via work since the introduction of AE, and that two million fewer individuals are under-saving. The minimum contribution rate rose to 8 per cent in April 2019 when the AE implementationFootnote 3 was concluded, contributed by employer (3%), employee (4%) and government (tax-relief, 1%), from the initial minimum rate of 2 per cent (1%, 0.8% and 0.2%, respectively). Despite the increase in the minimum contribution rate, the opt-out rate is reported to be stable (NEST Corporation, 2019).Footnote 4 Some may question whether individuals should focus on saving via a workplace pension scheme. However, concerns regarding saving sufficiency remain. Recent statistics show that, while the number of individuals saving via work has increased, contributions are largely made at the required minimum levels (Office for National Statistics (ONS), 2018). Taking the final contribution rate of 8 per cent into account, the position of the Pensions Commission (2005) was that making additional provisions was strongly recommended due to the uncertainty and risk involved in accumulation. This view was echoed by others who argued that the legal minimum contribution rate may be insufficient for the retirement income (Pensions Policy Institute (PPI), 2015; Institute and Faculty of Actuaries, 2016).

Implications for the younger generation's retirement saving

The recent developments in the British pension landscape discussed above have two implications for the younger generation's retirement saving. First, it involves greater uncertainty in accumulating and generating retirement income, which translates to a higher level of risk. Second, individuals are increasingly expected to save via work as a result, and to make an additional provision during their working-age years. These implications are particularly relevant to the adults in their thirties and forties, who are unlikely to have accumulated substantial DB scheme entitlements and may have started accumulating DC pensions in the middle of their working life through AE. Considering the shift from the DB to the DC schemes in the mid-1990s and the completion of the AE roll out in 2019, this age group roughly corresponds to those in their thirties and forties in 2014/2016, who are referred to as ‘younger adults’ in this study.

The younger adults will retire under a different pension policy structure from their parents. However, studies suggest that they expect to have retirement income from similar sources and to have a similar standard of living (Pettigrew et al., Reference Pettigrew, Taylor, Simpson, Lancaster and Madden2007; MacLeod et al., Reference MacLeod, Fitzpatrick, Hamlyn, Jones, Kinver and Page2012; Robertson-Rose, Reference Robertson-Rose2019). A recent industry survey reports that around two-thirds of adults aged between 30 and 45 expect to receive a State Pension but just under half anticipated a reduction in the State Pension amount when they reach retirement (Old Mutual, 2017).

Some may anticipate that wealth accumulation complements a lower level of retirement saving during the lifecourse, based on the previous generation's experience. The baby boomers accumulated substantial private pensions (DB pensions in particular) and housing wealth (Hills and Bastagli, Reference Hills, Bastagli, Hills, Bastagli, Cowell, Glennerster, Karagiannaki and McKnight2013), which contributed substantially to financial wellbeing in retirement. However, as mentioned above, the private pension wealth trajectory of the current younger generation differs considerably from that of the previous generation due to the shift from the DB to the DC schemes; the outlook for housing wealth has not been too optimistic. Substantially smaller proportions of the younger generation own a home compared to their parents’ generation at their ages as it has become more difficult to enter the housing market. Home-ownership outcomes for the younger generation are increasingly linked to parents’ socio-economic standing (Coulter, Reference Coulter2017a; Suh, Reference Suh2020a).

Saving for and generating retirement income for the current younger generation has become far more complex and involves greater uncertainty than previously. Individuals recognise an increasing need for saving (MacLeod et al., Reference MacLeod, Fitzpatrick, Hamlyn, Jones, Kinver and Page2012); however, the behavioural responses appear to be slow. According to the DWP (2014), retirement saving for this age group was mostly inadequate to generate a retirement income which was considered to be a median target by the Pensions Commission (2004, 2005). Private-sector reports later echo this concern, stating that the behavioural adjustment required for the changing pension landscape is largely absent (e.g. Old Mutual, 2017). These findings suggest a substantial gap between the behavioural change aimed at by policy makers and the current state of discretionary retirement saving.

Research questions

The above-mentioned discussions raise the following questions: If the younger generation is expected to save more for their retirement and make additional provisions, who is saving for retirement and who is not? How are they different in terms of their ability, attitudes and behaviours to retirement saving and to what extent? Adults in their thirties and forties are in the stages of life in which demographic and socio-economic arrangements are crucial for planning the next stage. To what extent do demographic and socio-economic characteristics contribute to explaining abilities, attitudes and behaviours to saving for retirement?

Modelling the decision-making process in retirement saving

This section introduces the Model of Financial Planning (Hershey et al., Reference Hershey, Jacobs-Lawson, McArdle and Hamagami2007) and discusses it in the context of discretionary retirement saving using the lifecourse perspective. The modifications made to the model are explained in detail in the next section.

Model of Financial Planning

This study builds on the Model of Financial Planning (Hershey et al., Reference Hershey, Jacobs-Lawson, McArdle and Hamagami2007). The model is developed on the premise that individuals’ saving behaviours are an outcome of a decision-making process, which is an interaction between psycho-social characteristics, task complexity and available economic resources based on cultural values (Hershey et al., Reference Hershey, Jacobs-Lawson, McArdle and Hamagami2007). For the psycho-social measures, the authors include future time perspective, which is defined as a positive outlook on retirement, retirement goal clarity and financial knowledge.

The model provides the foundation for a quantitative examination of the decision-making process. The psycho-social factors mediate the effects of socio-demographic factors on retirement saving behaviour (Hershey et al., Reference Hershey, Jacobs-Lawson, McArdle and Hamagami2007). The underlying assumption is that individuals not only form attitudes based on their internal controls but are also influenced by their socio-economic environment, which is broadly consistent with the tenets of the lifecourse approach. This framework is therefore particularly useful for examining the role of human agency in retirement saving in the broader socio-economic context.

Retirement saving in this study

This study examines discretionary retirement saving activity outside state or workplace saving, which was previously described as voluntary retirement saving (Gough and Niza, Reference Gough and Niza2011). The focus is on the action of having saved, which is different from participating in a saving programme developed by professionals (Le Grand, Reference Le Grand2006). It is also connected to the everyday understanding of saving as putting money in a savings account (e.g. Kempson et al., Reference Kempson, McKay and Collard2005), which is integrated with everyday economic activities.

Lifecourse approach

In order to study saving activities as a behavioural outcome, it is necessary to consider the role of human agency in an individual's decision-making process (Curchin, Reference Curchin2016). Human agency in this study is interpreted as ‘the ability to influence one's life’ (Mortimer and Shanahan, as quoted in Kristiansen, Reference Kristiansen2014). Due to the discretionary nature of saving that this study examines, it is important to understand individuals’ current financial wellbeing and how it may be connected to saving for their future financial wellbeing. This notion is referred to as financial resilience and explained further in the following section.

Lifecourse scholars are also of the view that human agency must be considered alongside the broader context in which it operates (Elder, Reference Elder1994; Kristiansen, Reference Kristiansen2014). Younger adults’ decision-making about the far future, such as retirement saving, would inevitably be based on their current socio-economic circumstances and priorities in how they would like to organise their lives. The study population is in the age group that is often associated with partnership and family formation, social roles are important and influential in organising their lives (Mortimer and Moen, Reference Mortimer, Moen, Shanahan, Mortimer and Johnson2016). Therefore, household income, home-ownership status and intergenerational transfer receipts, which are particularly relevant to young British adults today, are accounted for in the model (Karagiannaki, Reference Karagiannaki2011a, Reference Karagiannaki2011b; Hood and Joyce, Reference Hood and Joyce2013; Corlett and Judge, Reference Corlett and Judge2017).

A modified Model of Financial Planning

Modifications to the model are introduced so that the model is adequate for examining the decision-making process for discretionary retirement saving. Additional socio-economic factors are included in the model to provide a more realistic picture of the British younger generation's economic circumstances today. The section below explains the modified version of the Model of Financial Planning for this study. A path diagram for the model is shown in Figure 1.

Figure 1. A hypothesised Model of Financial Planning with modifications.

Financial resilience

The recurring nature of everyday financial behaviour provides insight into an individual's views and behavioural tendencies, which may explain different decisions made by individuals with a similar level of resources. Financial resilience represents this notion. For the younger generation, current saving behaviour, which can extend to longer-term saving, has become more critical. In this sense, individual behavioural tendencies are a good starting point that connects to the discretionary retirement saving activity.

Salignac et al. (Reference Salignac, Marjolin, Reeve and Muir2019) provide a framework for understanding financial resilience from the perspective of financial inclusion. The framework is comprised of four interconnected elements: economic resources (e.g. savings and debt), financial knowledge and behaviour (e.g. knowledge confidence), financial resources (e.g. access to bank accounts and credit facilities) and social capital (e.g. social support). The authors view financial resilience as a dynamic process rather than an outcome-focused state of being able to bounce back from adversity, as these four elements are interconnected and constantly change, which makes individuals’ ability to adapt crucial (Salignac et al., Reference Salignac, Marjolin, Reeve and Muir2019). Financial resilience in this study is applied to a narrowly defined context of discretionary retirement saving, corresponding mainly to the economic resource aspect in the study by Salignac et al. (Reference Salignac, Marjolin, Reeve and Muir2019).

Financial resilience is conceptually close to ‘financial capability’, which refers to having an adequate level of financial knowledge, and being competent and confident in making good decisions (Kempson et al., Reference Kempson, Collard and Moore2005a; Atkinson et al., Reference Atkinson, McKay, Kempson and Collard2006; Johnson and Sherraden, Reference Johnson and Sherraden2007). Financial resilience is termed differently here for its focus on existing behavioural patterns rather than the capability to manage future financial affairs.

As it focuses on current behavioural tendencies, financial resilience can also serve as an implicit measure for inertia. The study on the Save More Tomorrow (SMarT) programme shows the difficulties involved in changing saving behaviours (Thaler and Benartzi, Reference Thaler and Benartzi2004). The bigger a behavioural change is required, the greater the resistance one is expected to experience. Saving for retirement is far more complex and involves a longer time horizon; however, it shares a fundamental trait with rainy-day saving, which is withholding immediate consumption and reserving it for future. Rainy-day savers, therefore, may find extra steps required to save for retirement easier and are more likely to respond more positively. Individuals who do not currently save in any form may experience stronger behavioural resistance as a greater degree of behavioural change is expected.

Long-term perspective and retirement planning

The ‘time’ element in retirement from the perspectives of younger adults can be viewed in two different ways: as a general or abstract notion of a ‘far future’ event (future orientation), and in the more precise context of retirement (having thought about funding retirement). Regarding the former, economic studies have argued that myopic, or impatient, individuals overestimate the costs today and discount future benefits heavily (e.g. Fisher, Reference Fisher1930; Browning and Lusardi, Reference Browning and Lusardi1996). Some describe it as continuous discord between rational thinking and irrational tendency, or between the planner who looks out for long-term wellbeing and the selfish and myopic doer (Thaler and Shefrin, Reference Thaler and Shefrin1981; Loewenstein, Reference Loewenstein1996; Metcalfe and Mischel, Reference Metcalfe and Mischel1999). Psychologists, on the other hand, report that positive outlook to retirement (termed ‘future time perspective’) is associated with retirement saving contribution rates (Hershey et al., Reference Hershey, Jacobs-Lawson, McArdle and Hamagami2007).

Thinking about the distant future involves a high degree of abstract thinking beyond the timescale of everyday life (Canova et al., Reference Canova, Rattazzi and Webley2005; Lusardi and Mitchell, Reference Lusardi and Mitchell2007; Lusardi, Reference Lusardi2008). Thinking about a retirement-specific context (e.g. wanting to travel after retirement) may reduce the degree of abstractness, as it prompts individuals to develop more concrete ideas (e.g. building detailed travel plans). Studies found that having a clear retirement goal was associated with a higher level of saving contribution (Hershey et al., Reference Hershey, Jacobs-Lawson, McArdle and Hamagami2007; Stawski et al., Reference Stawski, Hershey and Jacobs-Lawson2007) and financial preparation (Hershey et al., Reference Hershey, Mowen and Jacobs-Lawson2003). These studies suggest that thinking about retirement and developing retirement-specific goals help to build a concrete context, leading to a behavioural outcome of saving.

Knowledge and retirement saving confidence

Financial knowledge and confidence in retirement saving are also important factors to consider in the decision-making process. Financial literacy scholars have argued that, as the complexity in financial products increases, the ability to obtain and understand financial information has become critical in order to make a sound decision (van Rooij et al., Reference van Rooij, Lusardi and Alessie2011b; Lusardi and Mitchell, Reference Lusardi and Mitchell2007). Others argue that financial knowledge enables individuals to realise the need to save for retirement (e.g. Mckenzie and Liersch, Reference Mckenzie and Liersch2011) and increases the willingness to engage with sophisticated financial instruments (van Rooij et al., Reference van Rooij, Lusardi and Alessie2011a).

A subjective measure of financial knowledge was found to be more relevant to financial behaviours than the objective score because knowledge internalisation increases self-efficacy (Serido et al., Reference Serido, Shim and Tang2013). Similar findings are reported in the context of retirement saving (Hershey et al., Reference Hershey, Jacobs-Lawson, McArdle and Hamagami2007), responsible financial behaviours (McCormick, Reference McCormick2009), changes in financial attitudes (Shim et al., Reference Shim, Barber, Card, Xiao and Serido2010), and attitudes and behavioural intentions of saving (Borden et al., Reference Borden, Lee, Serido and Collins2008).

Financial knowledge is also positively associated with how accurately individuals estimate the size of the required funding for retirement, as the study comparing American and Dutch adults shows (Van Dalen et al., Reference Van Dalen, Henkens and Hershey2010): the tendency to overestimate their ability to fund retirement is directly connected to the tendency to be overly confident about their retirement saving. Empirical evidence in this context includes a British study on future private pension incomes (Banks et al., Reference Banks, Emmerson, Oldfield and Tetlow2005) and an American study on over-confidence in retirement saving that is found unsubstantiated by asset holding (Helman et al., Reference Helman, Copeland and Vanderhei2015). Therefore, it is expected that confidence in retirement saving is highly relevant, as financial knowledge may explain how one perceives the need to save for later.

Economic circumstances: household income, home-ownership and intergenerational transfers

Income is one of the most relevant factors in understanding retirement saving behaviour (see e.g. Browning and Lusardi, Reference Browning and Lusardi1996). Many studies have found a strong positive relationship between income and retirement saving, whether it is measured as a saving rate (Dynan et al., Reference Dynan, Skinner and Zeldes2016), enrolment to saving schemes (Bassett et al., Reference Bassett, Fleming and Rodrigues1998) or contribution rates for workplace pension schemes (Hershey et al., Reference Hershey, Jacobs-Lawson, McArdle and Hamagami2007; Stawski et al., Reference Stawski, Hershey and Jacobs-Lawson2007). Recent qualitative studies on British young adults, however, suggest that an increase in income may have a positive, but limited, effect on increasing saving through workplace pension schemes (PPI, 2018; Robertson-Rose, Reference Robertson-Rose2019).

Home-ownership is highly relevant to retirement saving in the British context (Dewilde and Raemaeckers, Reference Dewilde and Raemaeckers2008); owning a home is a way to save for retirement, with the idea that down-sizing provides extra funding (Hancock, Reference Hancock1998; Crawford, Reference Crawford2018). On the other hand, housing difficulties also affect an individual's saving ability in the short term. The younger generation in Britain spend a longer period renting (Clarke et al., Reference Clarke, Corlett and Judge2016), and spend almost three times more on rent than their grandparents’ generation at their age (Corlett et al., Reference Corlett, Finch and Whittaker2016). Home-ownership continues to be the preferred housing tenure among the younger generation; the ability to own a home is expected to influence their long-term saving decisions (PPI, 2018).

Intergenerational transfers, such as inheritance, cash gifts or informal loans, have become more prevalent in recent years (Karagiannaki, Reference Karagiannaki2011b; Karagiannaki and Hills, Reference Karagiannaki, Hills, Hills, Bastagli, Cowell, Glennerster, Karagiannaki and McKnight2013); three-quarters of British adults born in the 1970s have either received or expected one (Hood and Joyce, Reference Hood and Joyce2017). Such a transfer is also found to be associated with substantially increased chances of becoming home-owners among young British adults (Suh, Reference Suh2020a), which could then motivate retirement saving (PPI, 2018). An industry study reports that around half of 30–45-year-olds expect an inheritance, and that it could prompt them to consider retirement saving (Old Mutual, 2017).

Socio-demographic characteristics: age, sex, marital status and degree-level education

Age functions as a proxy to measure the temporal distance between age today and at retirement (Elder and George, Reference Elder, George, Shanahan, Mortimer and Johnson2016). Young age is often found to be associated with myopia (e.g. Foster, Reference Foster2017; PPI, 2018), which may also be connected to a higher opt-out rate for workplace pension schemes among young males (Bryan and Lloyd, Reference Bryan and Lloyd2014). These ‘myopic’ behaviours may be due to resource constraints. However, a study by a financial services company hints that the perception of ‘age’ may also be at play; adults in their thirties consider they have another 8–10 years before starting to save, while the number of years only marginally reduces to 6–8 years for adults in their forties (Old Mutual, 2017).

Previous studies have attributed women's lower level of pension saving to the gendered employment patterns and lower lifetime earnings during the lifecourse (Ginn and Arber, Reference Ginn and Arber1996; Bardasi et al., Reference Bardasi, Jenkins and Rigg2002; Möhring, Reference Möhring2018). Women in Britain and internationally are also found to have a lower level of financial literacy than men (Lusardi, Reference Lusardi1997; Bucher-Koenen et al., Reference Bucher-Koenen, Lusardi, Alessie and van Rooij2014). Studies also have found that men tend to have more specific retirement goals (Wang and Shi, Reference Wang and Shi2014), and that women are more likely to be more risk-averse than men in their investment choices for retirement saving (Watson and McNaughton, Reference Watson and McNaughton2007; Clark and Strauss, Reference Clark and Strauss2008).

Marital status and number of children provide information on an economic unit, which shows how retirement saving decisions may affect the partners (Knoll et al., Reference Knoll, Tamborini and Whitman2012). Couples often make a collective decision, which increases the level of financial socialisation (Noone et al., Reference Noone, O'Loughlin and Kendig2012) and helps to strengthen consistency in their economic activities for a common goal (Noone et al., Reference Noone, O'Loughlin and Kendig2012; Payne et al., Reference Payne, Yorgason and Dew2014). Co-habitation has become more common in Britain (Vogler, Reference Vogler2005), especially among young adults (Pahl, Reference Pahl2005).Footnote 5 Co-habiting couples have a similar financial advantage to married ones by pooling income and sharing costs (Grinstein-Weiss et al., Reference Grinstein-Weiss, Zhan and Sherraden2006); however, marital status is considered more relevant to retirement saving as married couples are known to have more formal sharing arrangements such as having a joint account (Burgoyne et al., Reference Burgoyne, Reibstein, Edmunds and Dolman2007).

Educational qualification levels are also found to be related to financial capability, time perspective and financial knowledge (Atkinson et al., Reference Atkinson, McKay, Kempson and Collard2006; Serido et al., Reference Serido, Shim and Tang2013; Hayes et al., Reference Hayes, Collard and Kempson2014). Financial activities that require high cognitive abilities such as planning, staying informed and choosing products were found to show substantial differences by educational qualification levels (Finney et al., Reference Finney, Hayes and Hartfree2015).

Workplace pension schemes

A potential trade-off exists between workplace and other means of private pension saving (Mitchell and Moore, Reference Mitchell and Moore1998; Bryan et al., Reference Bryan, Lloyd, Rabe and Taylor2011). Individuals may also adjust saving rates depending on the workplace pension scheme types. For instance, due to uncertainty involved in DC pensions, DC scheme holders may be more inclined to save additionally.

Data and analytical strategy

Data and the study sample

The fourth wave of the WAS (ONS Social Survey Division, 2020), which was carried out between July 2012 and June 2014 (hereafter 2012/2014), is used in this study. Introduced in 2006/2008, WAS is a biennial survey which focuses on the wealth holding and economic wellbeing of British households. It provides rich information not only on detailed wealth holding but also on the individuals’ attitudes and economic activities that are essential for this paper. Since the third wave in 2010/2012, an additional sample was interviewed alongside the panel sub-sample to ensure the dataset is nationally representative at each wave. The fourth wave produced around 20,200 household and 38,300 individual interviews (ONS, Reference Office for National Statistics (ONS) Social Survey Division2020).

The analytical sample for this study includes those in their thirties and forties (N = 5,942). The sample only includes those who are employed and in paid work, excluding self-employed, to whom different pension-saving rules apply. For example, the workplace pensions of self-employed individuals (if existent) are likely to be classified as private (non-workplace) pensions.

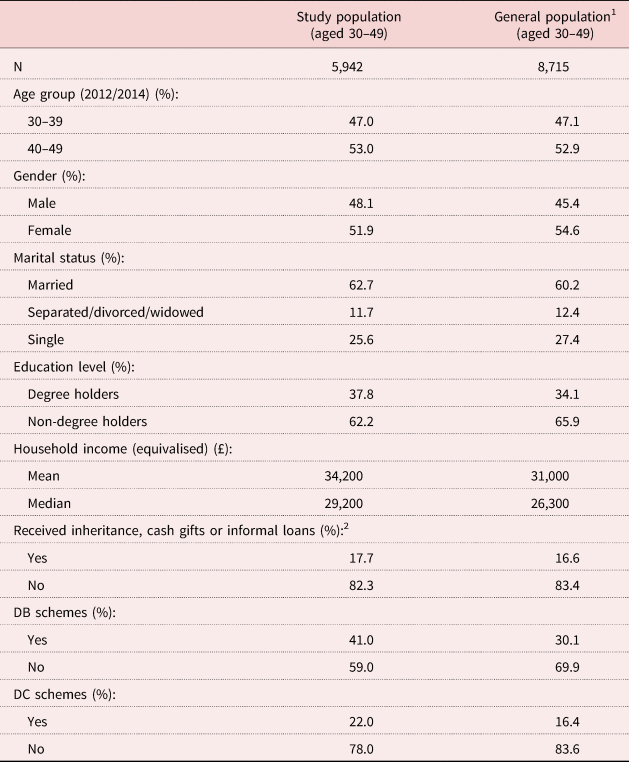

Characteristics portrayed in Table 1 show that the study sample is more likely to possess a university degree than the general population in their thirties and forties. The analytical sample has a higher household income on average and are more likely to have a workplace pension scheme, whether it is a DB or a DC scheme.Footnote 6 These differences, which are likely to be due to the inclusion of employed individuals only, are taken into consideration when interpreting the results.

Table 1. The characteristics of the study sample and the general population (Wealth and Assets Survey, 2012/2014)

Notes: All figures are weighted using a cross-sectional weight. 1. General population includes those aged between 30 and 49 who have completed a full interview in person. 2. Measured at the household level. Individual records are identified using the following thresholds in the Wealth and Assets Survey: inheritance equal or greater than £1,000, cash gifts equal or greater than £500 and informal loans equal or greater than £500. DB: Defined Benefit. DC: Defined Contribution.

The outcome variable

Discretionary retirement savers (hereafter ‘retirement savers’) are identified as those who ‘have saved any of their income in the last two years for example, by putting something away in a bank, building society or Post Office account other than to meet regular bills’, and if the reasons for having done so includes a retirement saving motivation (i.e. ‘to provide income for retirement’). One may save for multiple purposes (Wärneryd, Reference Wärneryd1989). For example, a shorter-term goal of saving a deposit for a home may contribute to a longer-term goal of saving for retirement. Co-existing saving motivations are recognised, and individuals are identified as retirement savers if one of their saving motivations is linked to generating income for retirement (ONS, 2016).

Descriptive statistics

Descriptive analysis shows that, while just over half of individuals aged 30–49 have saved for any reason other than retirement, only eight out of ten have saved for retirement in the past two years (see Table S2 in the online supplementary material). Figure 2 shows the proportion of savers who have saved but not for retirement (hereafter ‘general savers’) and retirement savers (motivations including one specific to retirement) by age group. It shows that, while the higher proportions of retirement savers are concentrated around mid-life and near-retirement age groups (55–59 and 60–64), the proportions of general savers vary to a lesser extent. This shows that age is an important factor to consider, although it is unclear whether the differences refer to the changes in saving behaviour or perception.

Figure 2. Proportions of general savers and retirement savers by age group (Wealth and Assets Survey, 2012/2014). Notes: All figures are weighted for repetitiveness. Retirement savers include individuals whose responses for saving motivations indicate that at least one of the reasons for saving was for future retirement income. Non-retirement savers are those who reported having saved but did not mention that they were saving for future retirement income.

One might question, then, whether the distinction between the two saver types provides any insight, as general saving becomes part of wealth building that could fund retirement. This assumption is reasonable if individuals save for long-term purposes; however, many save for short-term consumption as well, such as holidays and future purchases that are not necessarily contributing to wealth building in the long-term.

Analytical strategy

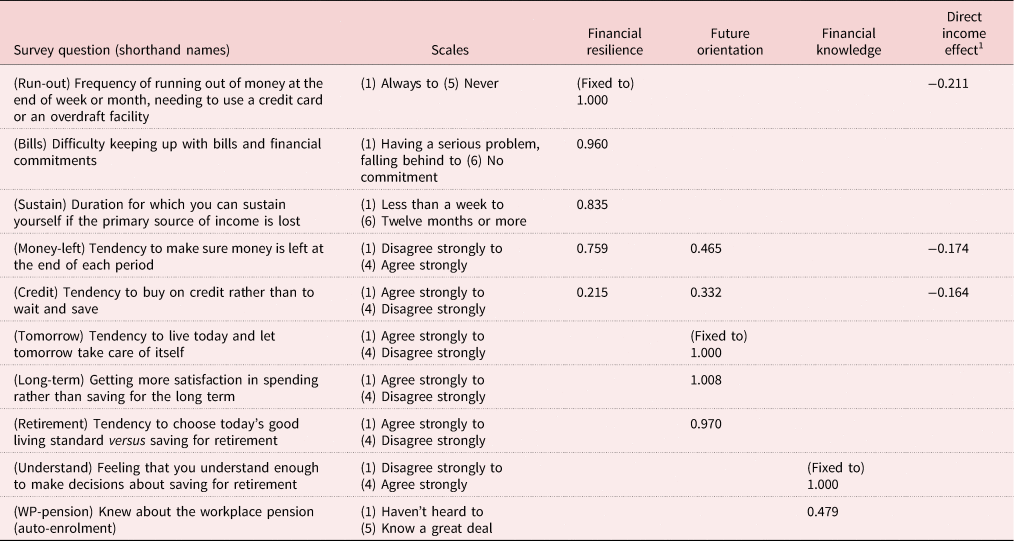

The analysis is conducted through SEM in the Multiple Indicators Multiple Causes Model, although this study does not make any causal claims. The analysis is conducted in three stages. In the first stage, a measurement model is built using factor analysis to construct measures for qualities that are not directly observable (Bartholomew et al., Reference Bartholomew, Steele, Galbraith and Moustaki2008). A set of survey questions theoretically relevant to a latent quality is selected and tested using factor analysis (see Table 2). The idea here is that an attitude, for example, although not directly observable, can be measured via a set of survey questions that collectively reveal information about it.

Table 2. Measurement part of the final model: three-factor with direct income effects

Notes: N = 5,942. 1. Standardised direct effects are reported. Unstandardised loadings are reported to facilitate the interpretation of factors using the anchored item scales (fixed at 1 for each factor). Survey weight is used, and the household structure is accounted for in the analysis. Model fit statistics: Root Mean Square Error of Approximation (RMSEA) = 0.022 (probability RMSEA ⩽ 0.05 = 1.000); Comparative Fit Index (CFI) = 0.973; Tucker–Lewis Index (TLI) = 0.966; Standardised Root Mean Square Residual (SRMR) = 0.058).

Each relationship between a latent variable (‘construct’ or ‘factor’) and its survey questions (‘observed items’ or ‘items’) can be understood as a regression model where the latent variable functions as an explanatory variable for the outcome variable (the survey response). As the survey questions are on the Likert scale, these are treated as ordinal.Footnote 7 The quality of the measurement is judged by the strengths of associations, referred to as ‘loadings’, between the latent variable and its observed items as well as the model fit statistics. Factor loadings are indicative of the contribution of the items to the factor; the relative size of the loadings guides qualitative interpretation of the factor.

As factors are interpreted based on the model parameters such as factor loadings, it is important to ensure that the interpretation is consistent across the study sample. Measurement Invariance (MI) testing is a procedure that tests the consistency in the factor loadings and item intercept terms by sub-group. Factor loading invariance indicates that the factors can be interpreted consistently across groups, while intercept non-invariance across groups would mean that the expected response for some survey questions,Footnote 8 holding other variables (including latent factors), differ by groups (Millsap, Reference Millsap2011; Kuha and Moustaki, Reference Kuha and Moustaki2015). In this study the survey questions which help measure financial resilience may be answered differently depending on different income levels. This is tested following the MI testing procedure (Millsap and Yun-Tein, Reference Millsap and Yun-Tein2004; Millsap, Reference Millsap2011), the results of which are explained in detail in the Results section.

The second stage involves testing relationships among the latent factors from the first stage. In a path diagram, arrows indicate the direction of the association between the factors; these relationships can be direct or indirect. A direct relationship exists if an explanatory variable is directly associated with the outcome variable (Kline, Reference Kline2011), which is represented by a straight arrow pointing to the outcome variable in a path diagram. An indirect relationship exists when two factors are not directly linked except through another variable, which is often described as ‘mediation’ (Kline, Reference Kline2011). The sum of these represents the total effect. Each path is tested based on a set of hypotheses based on the discussions in the previous section, and only the paths that are statistically significant at the 5 per cent level are retained.

The last stage expands the structural model by adding a set of demo-socio-economic characteristics (‘covariates’) to the model with a similar procedure as in the second stage. Age is grouped to contrast respondents in their thirties versus forties. Sex distinguishes males versus females. Marital status identifies individuals who are single or separated from those who are married. The education level variable distinguishes individuals with a university degree and those without. The two workplace pension types included are DB and DC, although some individuals may have both or none. Household income is a (log) net annual household income which includes any benefit receipts and other regular income (such as rent income) but excluding any one-off transactions. It is equivalised using the modified Organisation for Economic Co-operation and Development equivalisation factor. Home-ownership status is derived from housing tenure, distinguishing households with owner-occupation from other tenure types. Intergenerational transfer receipt is a binary variable that identifies households with a total of £1,000 or more as an inheritance, cash gift or informal loan from family and friends in the past two years. Cluster correction is used to account for the similarities between individuals from the same household.

As the analysis is conducted in three stages, the measurement model is established each time the structural part of the model is tested (Bakk and Kuha, Reference Bakk and Kuha2018). A sensitivity testing is performed to check possible changes in the measurement model. Two models are compared as follows: the loadings were freely estimated in the first model, while factor loadings were fixed according to the previous measurement model in the second model. The results show that the differences are marginal and do not change factor interpretation (not reported; available upon request). Therefore, the first model is preferred for its better goodness of fit.

Results

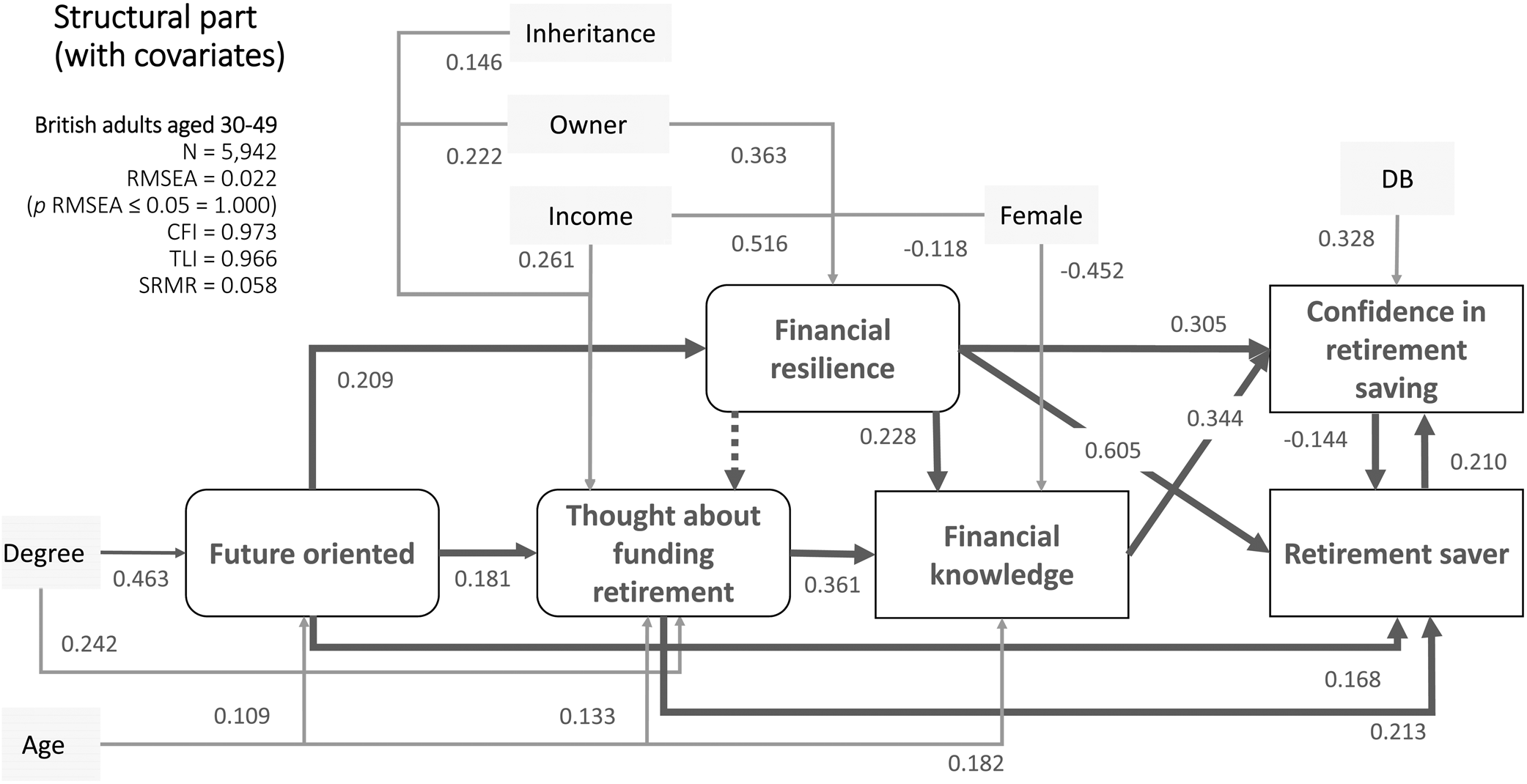

The statistical fit of the final model indicates that the model is well-fitted; the Root Mean Square Error of Approximation (RMSEA) is reported to be 0.022 (p RMSEA ⩽ 0.05 = 1.000),Footnote 9 Comparative Fit Index (CFI) = 0.973, Tucker–Lewis Index (TLI) = 0.966, compared to a benchmark of RMSEA < 0.06 and CFI and TLI > 0.950 (Hu and Bentler, Reference Hu and Bentler1999). The measurement part of the model is presented in Table 2, and the structural part of the model is presented in Figure 3.

Figure 3. Results from the structural part of the model. Notes: Owner refers to home-ownership while inheritance refers to the intergenerational transfer receipt(s). The dotted line indicates the path that lost statistical significance at the 5 per cent level compared to the structural model without covariates (but with household income for measurement invariance structure). Partial effects on household income that are not reported in the figure are: female (−0.136), degree holder (0.677), home-owner (0.538), having a Defined Benefit (DB) pension (0.082) and having a Defined Contribution pension (0.203).

Notes: RMSEA: Root Mean Square Error of Approximation. CFI: Comparative Fit. TLI: Tucker–Lewis Index. SRMR: Standardised Root Mean Square Residual.

Latent constructs for attitudinal and behavioural factors – the measurement model

The three latent variables – financial resilience, future orientation and self-reported financial knowledge – are constructed based on conceptually related survey questions (see Table 2), with minor modifications based on modification indices. Factor interpretations are provided herein after a short discussion on the MI testing and sensitivity analysis.

MI testing results show that it is reasonable to assume the loadings and item intercepts are invariant concerning gender and age. In terms of household income, however, only the factor loadings can be assumed invariant, as intercepts vary by levels of household income. It is more useful to interpret direct and indirect associations with income. For example, income has a negative association with ‘run-out’ (−0.211; see Table 2), but it has a stronger positive association with financial resilience (0.516; see Figure 3), which in turn increases the expected value of ‘run-out’ via its loading (0.856, standardised; not reported). Therefore, the net effect is a positive correlation (0.230 = 0.516 × 0.856 − 0.211; standardised).

After a satisfactory level of MI testing and sensitivity analysis, the factors are interpreted. Financial resilience indicates a cautious and responsible approach to managing financial resources today and short-term future uncertainty. Individuals who score high on this factor are more likely to manage current financial commitment, are able to anticipate near-future uncertainty and save for a rainy day, and are better prepared in case of a loss in income. As conservative consumers, financially resilient individuals are more likely to save up for a purchase rather than using credit cards. Therefore, financially resilient individuals are expected to be more financially capable (Atkinson et al., Reference Atkinson, McKay, Kempson and Collard2006) and are more likely to have a higher degree of self-regulation. The interpretation of financial resilience here is consistent with the definition offered by Salignac et al. (Reference Salignac, Marjolin, Reeve and Muir2019) albeit narrower in scope, focusing primarily on the economic resources; a higher level of financial resilience corresponds to better financial wellbeing while a low level indicates economic vulnerability.

Future orientation represents having a long-term perspective with regards to resource allocation. Scoring low on this factor would indicate myopia (Foster, Reference Foster2017). Individuals with high future orientation scores are more conscious of future financial security, more conservative in consumption and less likely to utilise a credit facility. They are thus more likely to have a positive attitude to retirement saving in general. Future orientation here refers to a general long-term perspective, without reference to a precisely defined future time-point.Footnote 10

Financial knowledge (self-reported) is a subjective measure of financial knowledge relating to retirement saving. A higher score indicates being well-informed about new developments in pension policy, such as the auto-enrolment introduced in October 2012, the implementation of which coincides with the survey period (July 2012 to June 2014). They are also more likely to be confident in making retirement saving decisions.

There are two other attitudinal variables that are useful to interpret here, although they are not part of the measurement model and therefore not shown in Table 2. These variables are each built based on one observed item, as no other survey questions could provide information for these measures. Consideration for funding retirement corresponds to the measure ‘retirement goal clarity’ (Hershey et al., Reference Hershey, Jacobs-Lawson, McArdle and Hamagami2007). It is based on the survey question: ‘Have you ever thought about how many years of retirement you might need to fund?’ It anchors ‘retirement’ as a concrete time-point with the explicit reference to ‘the number of years to fund in retirement’, which differs from the general notion of future used in future orientation. The measure, therefore, distinguishes those who have thought further about the funding aspect.

The measure for confidence in retirement saving is based on the survey question: ‘Do you think you are saving enough for your retirement?’ It prompts individuals to make a judgement about the ‘sufficiency’ of their current saving. Therefore, it is understood in line with confidence in the current retirement saving progress.

Relationship between latent constructs and covariates – the structural model

The results from the structural model show that attitudinal and behavioural factors play an essential role in understanding retirement saving behaviour, broadly in line with the findings of Hershey et al. (Reference Hershey, Jacobs-Lawson, McArdle and Hamagami2007). There are, however, appreciable differences in how and to what extent the internal and external factors are associated. The results from the final model are presented in Figure 3. All paths shown are found to be statistically significant (solid line), with one exception which lost its significance (dotted line). Coefficients are standardised and therefore are equivalent to correlation. Figures used in the discussion below are presented in Figure 3.

Financial resilience is found to be the strongest predictor of a retirement saver (coefficient = 0.605), controlling for other variables. This strong association is plausible as the qualities indicating their financial prudence today may also be helpful for retirement saving. One might argue that it is mostly driven by income, as individuals in high-income households are more likely to be resilient, being able to put aside more resources. In fact, financial resilience is strongly correlated with income (0.516), although how income is related to financial resilience may differ by income levels, as shown in the measurement model (Table 2).

Accounting for financial resilience, however, there is no statistically significant direct association between household income and the outcome variable. There are two possible explanations. First, financial resilience mediates the positive association between income and retirement saving, which indicates that individuals’ approaches to resource allocation and money management are more meaningful than household income per se. That is, how household income may influence attitudes towards, and behaviours of, retirement saving is more informative than relying solely on the levels of income as a predictor for retirement saving behaviour. This is in line with previous studies on British young adults’ place pension savings (Robertson-Rose, Reference Robertson-Rose2019; James et al., Reference James, Price and Buffel2020). Second, home-ownership is included in the model in addition to income, which is also positively associated with financial resilience (0.363). It indicates that household income alone may no longer provide a complete picture of younger British adults’ economic circumstances that influence how they organise their lives and plan for the future.

Home-ownership and intergenerational transfer receipt are found to be positively associated with individuals’ chances of having considered funding for retirement (0.222 and 0.146, respectively), which are broadly comparable to the partial association with income (0.261). As the home-ownership and intergenerational transfer receipt variables are added to the model, the coefficients for income on financial resilience and having considered funding retirement reduced. Also, as per the addition of the two variables, financial resilience no longer predicts having considered funding retirement (dotted line).

Future orientation and having thought about funding retirement are found to be associated positively with retirement saving activity (0.168 and 0.213, respectively). Associations are weaker than expected, however, indicating that adults in their thirties and forties are not necessarily acting on their future considerations (if they had any). It is also possible that individuals prefer other saving methods (e.g. purchasing a private pension or increasing workplace pension saving amounts) or decide not to save after all. These scenarios are realistic, especially in the near-zero interest rate environment in Britain following the recent financial crisis since 2007.

The age variable is also tested as a continuous variable, but the binary variable that distinguishes those aged 30–39 versus 40–49 is preferred not only because of a more accurate reflection of the widely held perception of ageing due to the change in the tens (e.g. being in their forties as opposed to in their thirties), but it also added more to the model. Being in one's forties as opposed to one's thirties has a positive but weak association with having a general and a retirement-specific long-term view (0.109 and 0.133, respectively). The small coefficients for age indicate that those in their forties are not likely to be more forward-looking nor more likely to have considered saving for retirement than those in their thirties, which echoes the findings by an earlier industry report (Old Mutual, 2017). Considering that those in the mid- to late-forties have already been working for half their working-age years before retiring, this is somewhat alarming in the current pension structure. University education has a strong positive association with the cultivation of a long-term view (0.463) and a moderate association with the retirement-specific time perspective (0.242), although further research is required to unpack these relationships.

Financial knowledge is found to increase confidence in the progress of current retirement saving (0.344) but is not associated directly with retirement saving activity; this finding is not surprising as the outcome variable refers to having saved using a bank account, which is easily understood and widely used among British adults today. The older group is found to have a slightly higher level of confidence in their financial knowledge (0.182). The gender difference in financial knowledge (Lusardi and Mitchell, Reference Lusardi and Mitchell2008) is also evident in this study; being female is found to have an alarmingly strong negative association with financial knowledge (−0.452).

Lack of confidence in current retirement saving (i.e. feeling the current saving is not on track to fund retirement sufficiently, hereafter ‘confidence’) may motivate some individuals to save more for retirement, and in turn, saving more may increase the level of confidence on the current saving progress. This hypothesis is tested by having a non-recursive structure for these two factors, indicating one is the explanatory variable for the other and vice versa at the same time. When tested without covariates initially, no statistically significant retirement saving effect is found on confidence. This is not presented in this study, but if represented in the manner akin to Figure 3, it would be equivalent to not having the arrow pointing from ‘Retirement saver’ to ‘Confidence in retirement saving’. As the covariates are introduced in the model, however, a statistically significant, weak negative effect of confidence reducing retirement saving activity (−0.144) is found.

Having a DB scheme is found to be positively correlated with confidence (0.328), which may explain the weak negative association between confidence and being a retirement saver. Having DC scheme is also tested but found not to add to the model. Putting these together, it appears that British adults in their thirties and forties recognise the different risk structure in DB and DC schemes. If it is indeed the case, it signals a change in risk perception compared to about ten years ago, when a previous study documented no significant difference in risk perception between the two scheme holders in Britain (Clark and Strauss, Reference Clark and Strauss2008).

The negative association between confidence and retirement saving, however, is weaker than expected. There are three possible explanations for this. First, the confidence measure may convey a general evaluation of saving ‘enough’ for retirement at present, compared to a precisely defined saving activity in the past two years. For the younger population who have many years to save, retirement saving confidence may represent future saving plans, regardless of having done so recently. Second, saving enough for retirement can be considered as continuously being financially resilient until retirement (e.g., ‘If I keep doing what I am doing now, I will be fine’). A positive direct relationship between financial resilience and self-assessed retirement saving sufficiency supports this as a possibility. Third, confidence may derive from using other means to save for retirement, such as buying a property or private pension, other than financial saving.

Discussion and conclusion

This study provides a quantitative analysis of discretionary retirement saving activity outside workplace pension schemes and NIC among British adults aged between 30 and 49 using a modified version of the Model of Financial Planning (Hershey et al., Reference Hershey, Jacobs-Lawson, McArdle and Hamagami2007). It assessed the roles of attitudes and behavioural tendencies in explaining discretionary retirement saving activity by establishing latent constructs that help measure qualities that are not directly observable. In particular, it includes a measure for individuals’ financial behaviour tendency and wellbeing today, which is key to assessing retirement saving outside the automatically occurring saving schemes. It also examined how and to what extent British younger adults’ current social and economic circumstances contributed to explaining different levels of attitudinal and behavioural characteristics that in turn inform retirement saving activity.

The study found that only one in ten adults aged between 30 and 49 reported having put money aside for retirement in the previous two years in 2012/2014. The results show that this low level of saving initiative cannot be attributed solely to the lack of economic resources (‘can't save’) or the lack of willingness (‘won't save’) as it is an outcome of a complex interplay between the two aspects.

Financial resilience, which refers to economic self-regulation and inclination to account for uncertainty, is found to be the strongest predictor for identifying a retirement saver. At first glance, this seems to suggest that a low level of saving among young adults is due to a lack of willingness to save. However, financial resilience is closely interlinked with socio-economic characteristics that are important to an individual's immediate economic circumstances, such as household income and home-ownership. This implies that financial resilience is a relative concept that needs to be contextualised, as how individuals conduct their everyday financial matters is likely to be influenced by their social and economic conditions that are not within their control.

This study also found that demographic and socio-economic factors play an important role in understanding how individuals may be encouraged to think about the long-term future more actively. Many adults in their thirties and forties are engaged in partnership formation and bringing up a family, and therefore want to create an ideal environment for the next stages of life. For example, employment stability and secure housing are prioritised in order for the younger generation to feel ‘settled down’, rather than saving for retirement (PPI, 2018). This could also be interpreted as individuals of a similar age may be at different stages of their lives. The notion of ‘getting older’ extends beyond chronological ageing to ‘social ageing’; that is, individuals may judge their current socio-economic circumstances against a set of benchmark conditions according to their stages in life, rather than their age per se. In this sense, the social ageing perspective may be more informative to understand potential barriers to retirement saving than chronological ageing.

The study findings have an important policy implication: it is important to seek behavioural changes as well as improvement in the individuals’ socio-economic ecosystem to seek an increase in retirement saving participation. For instance, increasing income levels alone to encourage saving may be less effective in isolation without increasing their financial wellbeing today. Also, as one helpful reviewer pointed out: should all individuals be encouraged to save for their retirement regardless of the current economic difficulties? The findings of this study suggest that focusing on saving for retirement without giving any consideration to improving the immediate economic circumstances is unlikely to be effective for building meaningful and sustainable behavioural changes.

Another important policy question to raise, based on the discussions above, is how those on limited economic resources should be saving for retirement. There are a few considerations that take advantage of the design of AE. First, an increase in the AE contribution rate by the employers and the state may be considered. For example, employers of low-income earners could contribute to their workplace pension schemes at a higher rate than the minimum contribution rate in exchange for tax relief. Second, the opt-out option may be modified to allow a maximum number of years for opting out; for instance, individuals who opt out may do so for a limited number of years before being automatically re-enrolled, with a potential incentive from the state for individuals to remain in enrolment.

One might argue that an increase in the State Pension may relieve individuals from the increasing pressure instead of seeking challenging behavioural changes from individuals. This will be welcomed if it is funded in a fiscally and socially sustainable manner which does not put pressure on future generations. Findings from this study are also in line with the view that emphasises on the ongoing nature of retirement saving that occurs during the entire ageing process, where ageing refers to a life-long development not confined to old age (Walker, Reference Walker2018). Current financial difficulties affect future economic autonomy, and the social outcomes along the lifecourse are not likely to be ameliorated by increasing retirement income in the future.

This study has certain limitations. The analytical sample only includes those who are employed; therefore, the findings do not apply to those who are self-employed or other forms of employment without further research. Also, the influence that parents and colleagues have on attitudes towards retirement saving (Robertson-Rose, Reference Robertson-Rose2019) and the trust in the government and financial institutions (e.g. Foster, Reference Foster2017) are not explored.

The study also presents a number of future research opportunities. Substantial within-generation inequality among the younger generation has been documented in terms of income (Corlett et al., Reference Corlett, Finch and Whittaker2016; Corlett, Reference Corlett2017), home-ownership outcomes (Corlett and Judge, Reference Corlett and Judge2017; Coulter, Reference Coulter2017b; Suh, Reference Suh2020a) and intergenerational transfer receipts (Karagiannaki, Reference Karagiannaki2011b, Reference Karagiannaki2017; Hood and Joyce, Reference Hood and Joyce2017) in Britain. Given their importance in this study, it may be hypothesised that the inequality in these economic conditions may translate to inequality in the ability to make provision for the future. As economic and political uncertainty in Britain and internationally continues to affect the younger generation's economic outcomes, further research in this area can inform policy makers of the effect on long-term financial wellbeing.

Moreover, financial resilience is assumed to be consistent across the income distribution in this study. Salignac et al. (Reference Salignac, Marjolin, Reeve and Muir2019) consider the relationship between internal and external resources related to financial resilience to be dynamic. Furthermore, Kempson et al. (Reference Kempson, Collard and Moore2005a) view financial capability as a relative concept. Building on these studies, it may be possible to examine aspects of financial resilience depending on the income level and to assess how it may shape future planning. In addition, while the term ‘gender’ was used interchangeably with ‘sex’, the scope of this study is limited to highlighting the differences in patterns rather than examining underlying gender issues (Ginn and Arber, Reference Ginn and Arber1996; Price, Reference Price2007; Joseph and Rowlingson, Reference Joseph and Rowlingson2012; Grady, Reference Grady2015; Foster and Ginn, Reference Foster, Ginn and Shaver2018; Foster and Heneghan, Reference Foster and Heneghan2018). The gender aspect is further examined as an extension to this study (Suh, Reference Suh2020b).

This paper makes several contributions. The study examined retirement saving behaviour from individuals’ perspective by incorporating financial resilience as a measure of economic autonomy today. The study moved away from the overemphasis on the role of income in understanding retirement saving behaviour. Instead, it provides a more complete picture of British younger adults’ social and economic environment today by taking home-ownership and intergenerational transfer records into account. As a result, it depicted a nuanced picture of interplay between internal and external characteristics in understanding retirement saving behaviour among British adults aged 30–49 outside automatically occurring saving schemes. Also, it views ageing from the lifecourse perspective and introduced the concept of ‘social ageing’, which is an alternative to the chronological ageing-focused approach widely used in retirement saving studies. By doing so, the study provided a more nuanced picture of how individuals may respond to policies that aim to increase discretionary retirement saving.

Supplementary material

The supplementary material for this article can be found at https://doi.org/10.1017/S0144686X21000337.

Open access

Open access