No CrossRef data available.

Article contents

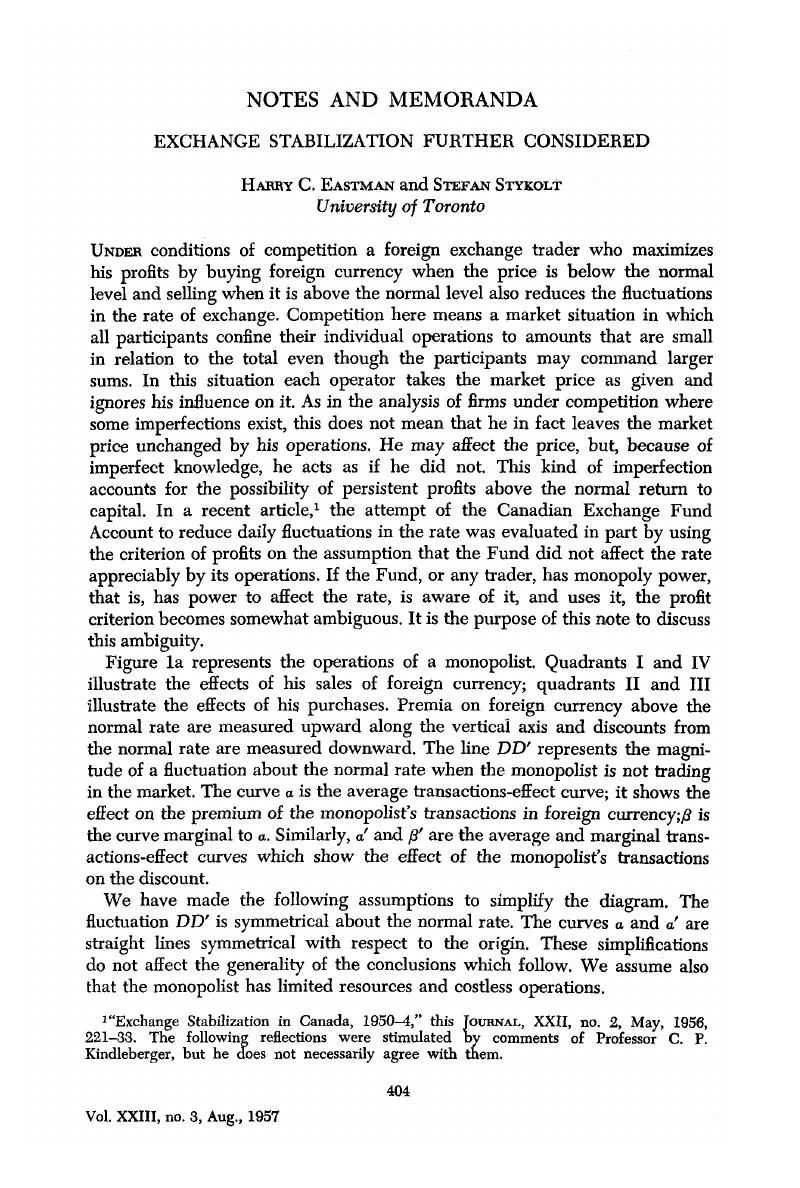

Exchange Stabilization Further Considered

Published online by Cambridge University Press: 07 November 2014

Abstract

An abstract is not available for this content so a preview has been provided. Please use the Get access link above for information on how to access this content.

- Type

- Notes and Memoranda

- Information

- Canadian Journal of Economics and Political Science/Revue canadienne de economiques et science politique , Volume 23 , Issue 3 , August 1957 , pp. 404 - 408

- Copyright

- Copyright © Canadian Political Science Association 1957

References

1 “Exchange Stabilization in Canada, 1950–4,” this Journal, XXII, no. 2, 05, 1956, 221–33.Google Scholar The following reflections were stimulated by comments of Professor C. P. Kindleberger, but he does not necessarily agree with them.

2 Of course, the sequence of transactions may be reversed: sales at a premium may follow purchases at a discount.

3 Eastman, and Stykolt, , “Exchange Stabilization in Canada,” 226.Google Scholar

4 A Fund that follows what seems to be the officially stated policy of preventing large departures in the rate upward or downward from normal will roughly approximate the policy of maximum profits described in paragraph 2.

5 Eastman, and Stykolt, , “Exchange Stabilization in Canada,” 226–7.Google Scholar

6 Ibid., 231.

7 The Fund's over-all position at the beginning of 1952 was U.S. $1,745.6 million. The matched turnover of U.S. dollars for the whole of 1952 was U.S. $248.4 million. (Minister of Finance, Exchange Fund Account, “Notes on Statements of Assets and Liabilities for 1952 Compared with 1951” (typed, n.d.).) We have no information on matched turnover for other years.

8 The total volume of Canadian exchange transactions cannot be calculated. In 1952 it exceeded $13.5 billion, which is the sum of all transactions set out in the balance of international payments for 1952 except that a gross rather than a net figure is used for sales and purchases of securities between Canada and other countries.