In Japan, the new health technology assessment (HTA) system was launched in April 2019; however, the trial evaluation of thirteen products started in 2016 and continued to 2018. Since 1992, Japan has allowed for the submission of pharmacoeconomic data for medicine pricing, and it was one of the first countries to introduce cost-effectiveness data as part of its healthcare decision making. In comparison, the Pharmaceutical Benefits Advisory Committee (PBAC) of Australia became one of the first public bodies to institute mandatory submission of such data for the Pharmaceutical Benefits Scheme (PBS) listing only in 1993 (Reference Henry, Hill and Harris1). However, data submission in Japan was voluntary and there was no consensus on how such data should be used. There was also no review process for the submitted data. Therefore, the Ministry of Health, Labour, and Welfare (MHLW), which is responsible for determining the prices of medicines and medical devices, did not insist on data submission, meaning that the submitted data did not influence pricing and medicine listing. Consequently, few manufacturers submitted data. Meanwhile, many other countries promoted the introduction of an HTA for medicine listing or price negotiation. In Japan, the trial introduction of cost-effectiveness evaluationFootnote 1 did not begin until 2016 (Reference Shiroiwa, Fukuda, Ikeda and Takura2). As an organization for official HTA process, the Center for Outcomes Research and Economic Evaluation for Health (C2H) was finally established in 2018 as a department under the National Institute of Public Health (NIPH).

Shiroiwa et al. (Reference Shiroiwa, Fukuda, Ikeda and Takura2) introduced the background and discussion concerning the trial introduction of cost-effectiveness evaluation in Japan. This study also emphasized the necessity of introducing HTA in the Japanese healthcare system, the role of each interest group, and the main discussion points.

Similar to the systems in France and Germany, the Japanese healthcare system is a multi-payer system. Private payers are not allowed, and all payers are public insurers. The prices of (the same brand) medicines and medical devices were constant across Japan, although they are changed over time. The MHLW regulates reimbursement prices, not ex-factory prices, thus differing from some European countries. Therefore, “price” in this study means the reimbursement price to medical institutions, which includes wholesalers' distribution costs (no regulation of wholesalers' margin), hospitals' stock costs, VAT, and so on, but not dispensing costs. Medicines are generally paid for via a pay-for-service system, except some less expensive ones at some special hospitals. The MHLW does not apply an annual fixed-budget payment system to clinics and hospitals.

Methods

The data set consists of published documents from MHLW and discussions held with certain MHLW stakeholders, my organization (NIPH), and members of industry and academia. The introduction of cost-effectiveness evaluation was discussed at Chuikyo, the Central Social Insurance Medical Council (CSIMC)Footnote 2, an advisory body to MHLW. I was present at almost all the CSIMC meetings and took notes during the discussions. I also used the minutes of these meetings. As I have held another position in the MHLW related to cost-effectiveness evaluation since December 2012, my own observations were also included, although confidential information was omitted.

Results

Results of the Trial Implementation for Evaluation from 2016 to 2019

The trial implementation of the evaluation of thirteen medicines and medical devices on the market began in April 2016. By the end of March 2017, the manufacturers had submitted their analyses, which were reviewed by an independent academic group and the NIPH by September of the same year. The results were submitted to CSIMC and, based on this process, the reimbursement prices of two products—Opdivo (nivolumab) and Kadcyla (trastuzumab emtansine)—were decreased and the price of one product—Kawasumi Najuta thoracic stent graft system—was increased (Table 1)Footnote 3.

Table 1. Results of Trial Implementation

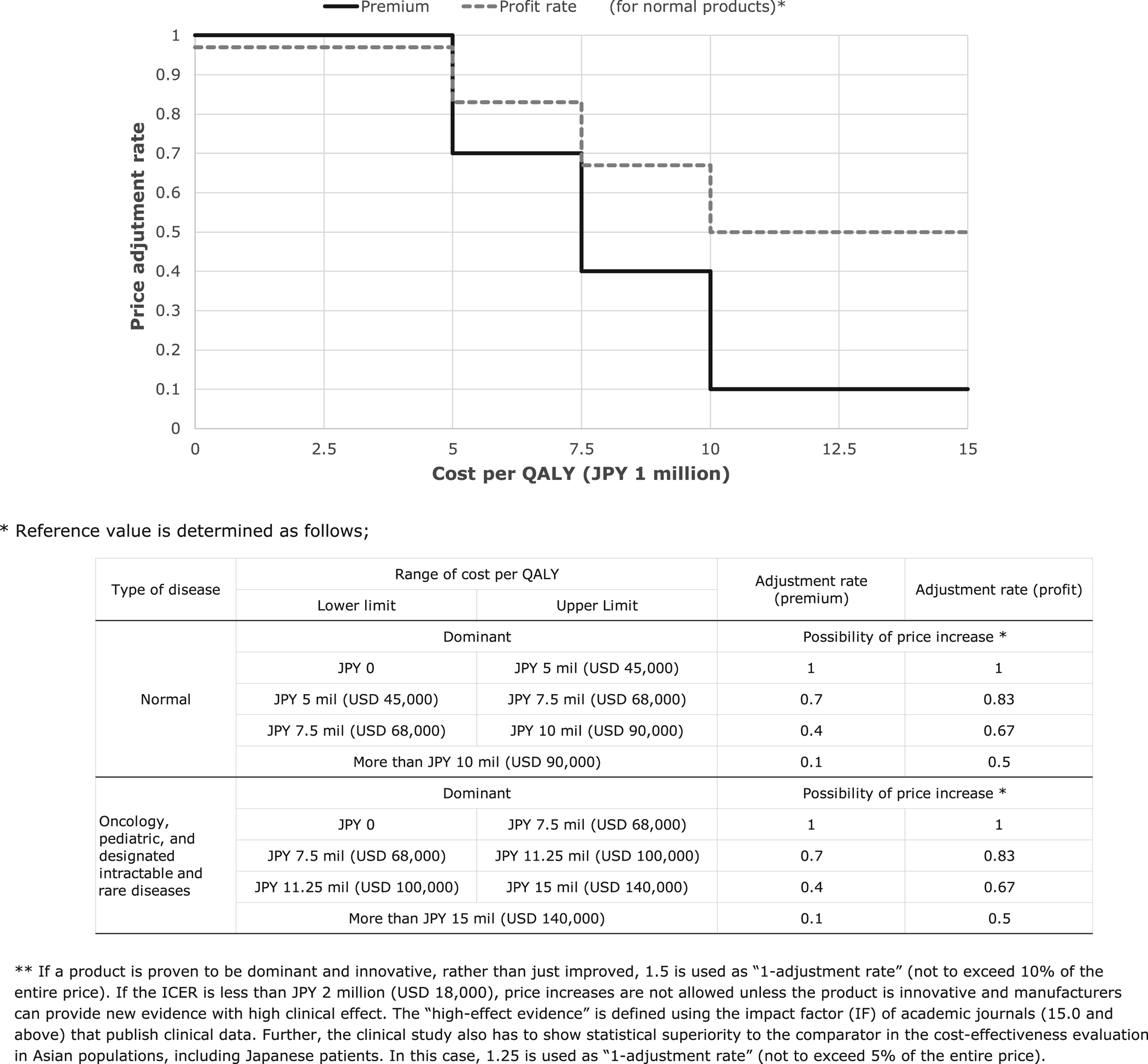

A: dominant; B: ICER is less than JPY 5 million (USD 45,000)/QALY; C: ICER is from JPY 7.5 to 10 million (USD 68,000–90,000)/QALY; D: ICER is JPY 10 million (USD 90,000)/QALY and over; E: ICER is JPY 11.25–15 million (USD 100,000–140,000)/QALY; F: ICER is JPY 15 million (USD 140,000)/QALY and over; G: impossible to analyze.

At first, the MHLW planned to officially introduce the cost-effectiveness evaluation from FY 2018 (April), just after the trial periods. However, the manufacturers opposed this strongly. Their main contention was that they were provided with few opportunities to communicate with NIPH and the experts at CSIMC. Manufactures were of course not very willing to officially introduce cost-effectiveness evaluation. As a result, the official introduction was postponed and the trial implementation was reviewed in FY 2018. After completing the reviews, detailed discussions on the official introduction resumed, with the members of the CSIMC finally reaching a consensus. The details of this consensus are presented in the next sections.

Overview of Introduced Cost-Effectiveness Evaluation System from 2019

Target Products of the New Cost-Effectiveness Evaluation System

Due to the CSIMC discussions following the submission of the trial implementation results, the new cost-effectiveness evaluation is being used initially only for the price adjustment of medicines and medical devicesFootnote 4, not for reimbursement decision makingFootnote 5. The cost-effectiveness evaluation process starts after the products are launched in the market. The procedure is similar to Germany's AMNOG (Reference Ruof, Schwartz, Schulenburg and Dintsios3), which evaluates new products after listing. The results are reflected in the product prices after approximately 15–18 months.

The target medicines and medical devicesFootnote 6 are principally selected when they are newly listed at the general assembly of the CSIMC. At the time of the introduction of the cost-effectiveness evaluation for FY 2019, the evaluation results were initially used for: (A) Adjusting premiums when the price is calculated using a “similar efficacy comparison method”Footnote 7 (i.e., “new drug price” = “existing drug price” + “premium”), and (B) adjusting the premium and regulated constant profit rate for manufacturers (the latter is adjusted only if the disclosure levelFootnote 8 is 50 percent or less) when the price is calculated using the “cost calculation method”Footnote 9.

Pediatric products, or products intended for designated intractable and rare diseases as defined by Japanese law, are exempt from the evaluation. Moreover, in the case of (B), if the disclosure level of the product is more than 50 percent and no premium is added, the product is exempt from cost-effectiveness evaluation.

However, not all products that satisfy the above conditions are selected as targets; products with a small budget impact are also exempt. The selection criteria are as follows:

Category H1: Annual peak salesFootnote 10 of JPY 10 billion (USD 90 million, USD 1 = JPY 110) and over. In Japan, new products (medicines and devices) are listed quarterly. Products from category H1 are selected at the time of their listing and the cost-effectiveness evaluation process starts.

Category H2: Annual peak sales from JPY 5 billion (USD 45 million) to JPY 10 billion (USD 90 million). H2 category products are considered candidate targets. They are kept in reserve as candidates and the target products are selected from these candidates based on their peak sales twice a year, considering the number of selected products and the process capacity.

In the case of technologies that are exempt from evaluation, when the actual sales exceed the category criteria above (e.g., due to the addition of a new application), they are also included in categories H1 or H2 as target products.

Category H3: The CSIMC can select target products if their prices are significantly high (the specific threshold is not given) or if new clinical data that could influence the cost-effective evaluation becomes available. For example, it is possible that no superiority is confirmed in the actual clinical setting or better outcomes are shown after the completion of the cost-effectiveness evaluation. C2H can submit the recommendation of candidate products for re-evaluation to CSIMC.

Category H4: Products with premiums listed before the implementation of the policy and whose annual actual sales (not predicted peak sales) exceed JPY 100 billion (USD 900 million). The criteria for categories H1 to H3 are meant for products newly listed after the start of the cost-effectiveness evaluation, and the criteria for H4 are intended for existing, older technologies. Further, CSIMC can also select products for category H4 based on the same criteria as those of category H3.

Category H5: In this final category, the medicines and devices similar to the target products selected for evaluation are included. Such products are not individually evaluated but are treated in the same manner as similar products already targeted.

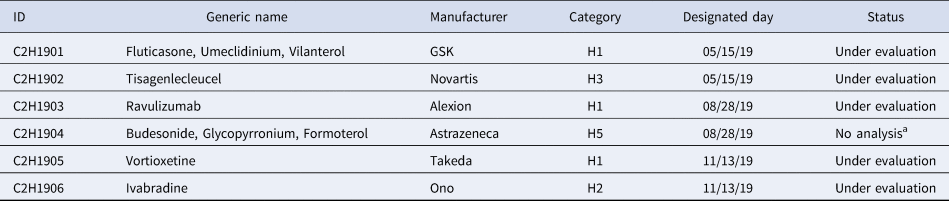

Table 2 shows the products selected for cost-effectiveness evaluation in December 2019 and the categories.

Table 2. Selected Products for Cost-Effectiveness Evaluation from December 2019

a The same results with C2H1901 will be applied.

Price Adjustment System Based on Cost-Effectiveness

The MHLW adjusts the reimbursement price of products using the results of the cost-effectiveness evaluation described in the previous section. In the case of products evaluated using the similar efficacy comparison method, only the premium (part of the whole price) is adjusted. In contrast, both the profit rate and the premium are adjusted if the cost calculation method is applied (the profit rate is adjusted only for products with a profit rate of 50 percent or less).

First, the target product is evaluated from the perspective of additional benefit as a selected major outcome(s) (e.g., effectiveness, safety, or QOL) using systematic reviews. If the product has no additional benefits compared with a similar product (referring to the cost-effectiveness analysis), a so-called cost-minimization analysis should be performed.

Only if additional benefits to a comparator can be proven, can an incremental cost-effectiveness ratio (ICER) be calculated. The adjustment rate is determined using the ICER interval and the premium or profit rate (Figure 1). The Japanese reference value 5 million (USD 45,000) per QALY is frequently cited in academic research. According to the CSIMC discussion, the value is justified by (a) empirical survey of willingness-to-pay (Reference Shiroiwa, Sung, Fukuda, Lang, Bae and Tsutani4) (b) GDP per capita, and (c) cost per QALY threshold in other countries (Figure 1). Further, MHLW uses different premium and profit rates for different categories. The actual decreased price is calculated by the multiplying adjustment rate by the range of price adjustment (premium, profit rate, or both). For example, a medicine with a 10 percent premium (JPY 110) is not cost-effective when compared with a similar drug (JPY 100). According to the results of the cost-effectiveness evaluation, the adjustment rate is .4 (the method for determining the adjustment rate is described below) and the price of the product is decreased by JPY 10 × (100 − 40 percent), or JPY 6.

Fig. 1. Stepwise function of price adjustment rate (normal product).

As a more complicated example, if the ICER interval of a cost-calculated product (JPY 110) with a 10 percent premium (JPY 10) is JPY 8 million per QALY, the adjustment rate for the premium is .4 and that of the profit rate is .67. The product loses 60 percent of its premium and 33 percent of its profit rate, that is 10 × .6 + 100 × 14.6 (profit rate) × .33 or JPY 10.8, using the cost-effectiveness evaluation.

In the case of oncology, pediatric, and designated intractable and rare disease products, the reference value is increased by a factor of 1.5. The factor is based on the consensus of the CSIMC, not based on the scientific discussion. For both normal and special products, the price reduction stops when the ICER reaches JPY 5 million (or 7.5 million). As previously mentioned, the products indicated as meant only for pediatrics or intractable and rare diseases are exempted from the evaluation. However, when products for special populations, such as the pediatric population, have other indications for adults, they are not exempted from evaluation and cost-effectiveness for pediatric population is evaluated.

Finally, if the price is reduced based on the calculation above, the cost/QALY may fall below JPY 5 million (or JPY 7.5 million) as a result of the adjustment, and it may be overadjusted for manufacturers. In this case, the reduction stops at the threshold price. In addition, the maximum reduction rate is limited to 10–15 percent of the entire price before adjustment. Such safeguards may be put in place when the premium rate is high.

Process of Cost-Effectiveness Evaluation

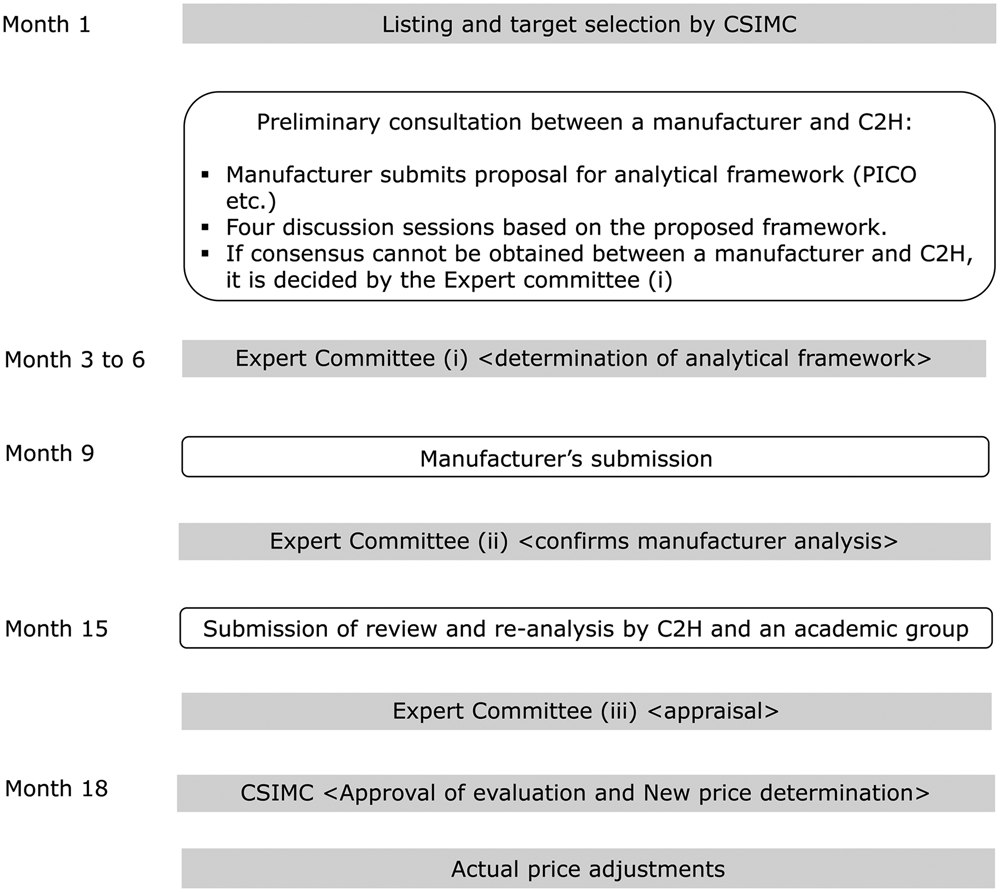

The target products are selected after the CSIMC decides the listing. The MHLW routinely adds new products to its quarterly reimbursement list. If a product is selected for cost-effectiveness evaluation, the manufacturer must submit the data within 9 months from the selection. During the first 3–6 months, the analysis framework (including the target population, comparator, etc.) should be determined based on preliminary consultations with the C2H. The submitted analysis is reviewed by academic analysis groupsFootnote 11 and is finalized by C2H (at the NIPH) within 3–6 months. Based on the manufacturer's submission and the C2H public analysis, the Expert Committee on Cost-Effectiveness EvaluationFootnote 12 examines the scientific quality of the analysis and determines the most likely ICER figure or range for the product (the appraisal process). This result is then reported to the CSIMC general assembly and the MHLW adjusts the price of the product based on the cost-effectiveness evaluation. The entire process takes 15–18 monthsFootnote 13 (Figure 2).

Fig. 2. Process of evaluation.

The C2H was established for the official evaluation process in 2018 as a department of the NIPH. Three universities were selected for the academic analysis groups.

Revision of the Cost-Effectiveness Evaluation Guidelines

The official cost-effectiveness evaluation guidelines (Guidelines for Preparing Cost-Effectiveness Evaluation to the CSIMC) were revised and approved by the CSIMC general assembly (5). The second edition of the guidelines follows the same principles as the original (Reference Shiroiwa, Fukuda, Ikeda, Takura and Moriwaki6), but contains some revisions concerning the results used for price adjustment.

First, regarding the comparator, the concept of “most replaced” played a significant role in the first edition; when a technology is newly introduced in the clinical setting, the listed old technology (standard or most commonly used therapy) is replaced by the new technology. This applies to the discussions on listings but not to those concerning price adjustment, as a new technology has already been listed and has replaced the old technology. Therefore, instead of the “most replaced” concept in the first edition, technology at the tip of the efficiency frontier (the most effective technologyFootnote 14) was used as the comparator.

Second, the difference in the parameters between groups, which may be caused by chance, is disallowed, and the same pooled value is used in both groups for model parameters. Of course, the “difference” may be accepted if it is sufficiently supported by other clinical evidence, even if there is no statistical significance. Therefore, this evaluation system first requires proof of “additional benefit” over those offered by a comparator, and cost-minimization analysis must be employed if such benefit is not confirmed.

For example, the hazard ratio of the product under evaluation is estimated to be 1.08 (95 percent CI, .76–1.41), and there is no other evidence of its superiority to a comparator. Thus, in this case, 1.0, and not 1.08, should be used for the hazard ratio of the base-case analysis, which may be contrary to the Bayesian concept. When the results of a cost-effectiveness analysis are used for listing, the decision is mainly binary (yes or no). However, in our setting, the single price adjustment rate using the cost-effectiveness analysis result is used. In such a case, it seems difficult to apply ICER based on the Bayesian concept to decision-making. Further discussion on this issue might be needed.

In the case of evaluation of technologies that have multiple indications or heterogeneous groups, various pricing methods are used in other countries (Reference Pearson, Dreitlein, Henshall and Towse7). Section 6.5 of the official guidelines states the ICER of each group and determines the price adjustment rate for each group. Next, the weighted mean of the price adjustment rate considering the size of each population was calculated. For example, a product with a 10 percent premium has indications for three different indications (e.g., lung, breast, and colorectal cancer). First, three different ICERs are calculated independently for each indication (lung, breast, and colorectal cancer). Assuming the ICER is JPY 7 million/QALY for lung cancer, 20 million/QALY for breast cancer, and JPY 10 million/QALY for colorectal cancer, the adjustment rate is 1, .1, and .7, respectively (Figure 1). If the percentage of the population is .3, .45, and .25, the price is decreased by 10 percent (premium) × {(1 − 1) (adjustment rate for lung cancer) × .3 (population weight for lung cancer) + (1 − .1) (rate for breast cancer) × .45 (weight for breast cancer) + (1 − .7) (rate for colorectal cancer) × .25 (weight for colorectal cancer)} = 4.8 percent. This method is similarly applied to the sub-population in the same indication.

Value-Based Pricing Adjustment System

In summary, the size of the price adjustment in the new cost-effectiveness system is determined by the following three factors: (a) price reduction rate (per part of the price or per premium and/or profit rate) determined by the ICER, (b) price reduction rate (for the entire price) when the cost/QALY reaches JPY 5 million (e.g., JPY 7.5 million in case of anticancer medicines), and (c) 10–15 percent of the entire price before adjustment.

The MHLW indicates that factor (a) is the principal price adjustment method, and that (b) and (c) are supplementary to prevent the reduction rate from becoming excessive. However, the actual price reduction rate is essentially determined by the weakest (or the lowest percentage) of the three rules. The adjustment method can therefore be explained as follows.

The price is reduced to the point where the ICER reaches JPY 5 million/QALY (rule [a]), and two other rules ([a] and [c]) alleviate the adjustment.

This indicates that the Japanese system is also similar to value-based pricing (VBP) (Reference Webb and Walker8), in which the prices of medicines and medical devices are set at a level where the ICER is below the cost/QALY threshold.

Discussion

We have taken the first step of introducing cost-effectiveness evaluation (or HTA) to the Japanese healthcare system. The discussion on the introduction began in 2012 and lasted for 7 years, until it was officially introduced. This long period of discussion was needed for reaching an agreement with stakeholders and ensuring understanding of the concept and technical terms of HTA. Technically, how to build the new concept of cost-effectiveness into the existing pricing system is a difficult problem. The pricing system has complicated but established rules and procedures.

It seems complicated to harmonize the new system with the existing, more complicated, pricing rule. However, the principal idea is essentially similar to that of value-based price adjustment (VBPA). The superficial difference in the systems of Japan and other countries (e.g., the UK) may be the result of how official prices of drugs and devices are determined. In many developed countries, prices are freely determined by manufacturers or through negotiation with public bodies, and thus, explicit rules and regulations of pricing are simpler. However, in Japan, the MHLW, and possibly also manufacturers, prefer detailed and strict calculation rules for pricing.

From my academic perspective, a simpler and clearer HTA system is more suitable. My concern is that in the case of unpredictable flaws in the system, which are sometimes obscured by complexity, manufacturers are provided with some incentive or disincentive—an undesirable consequence for the healthcare system. However, our system has to start from this point, and it is a critical step forward in the Japanese HTA system. We should continue efforts to enhance the system by collaborating with the government, academia, and manufacturers.

For improving the system, immediate discussions are needed on:

(a) The application of a cost-effectiveness evaluation to the decision-making process for listing new medicines: The Japanese system currently uses cost-effectiveness evaluation results only for price adjustment, not for reimbursement decisions. The reimbursement decision should also consider cost-effectiveness. If the stakeholders hesitate to limit the reimbursement of products, it might be better to start with optimizing the reimbursement condition using a cost-effectiveness evaluation.

(b) Expansion of target products: The current system exempts the evaluation of technologies with no premium. However, in certain cases, the comparator for medicine or medical device pricing might be different from that of the cost-effectiveness evaluation. Technologies with no premium are not always cost-effective, even when their price is similar to existing technologies; therefore, their prices should be evaluated.

(c) Target of price adjustment: The current system limits the target of price adjustment to a part of the entire price (premium and/or profit rate). There is no clear rationale for this from an academic perspective, as the size of the premium is not determined by the HTA. Some have criticized this rationale, as the premium rate or how the comparator is determined at the price setting is sometimes arbitrary and unclear. It is therefore more reasonable for a price adjustment to target the entire price or part of the price.

HTA system reform will help promote both technological innovation and sustainability of the healthcare system with transparency. Moreover, there are few economic evaluation experts in Japan with the relevant evaluation experience. We need to create greater capacity to enhance this academic review system. This is a fundamental issue for our newly constructed system.

Sources of Funding

This research received no specific funding from any agency, nor from the commercial or not-for-profit sectors.

Open access

Open access