Introduction

Wealth is an important determinant of individual living standards; for example, it allows individuals to smooth consumption over the lifecycle and can help facilitate major lifecycle decisions. However, only recently has it been possible to show the extent to which wealth holdings, that is wealth inequality, differs across individuals at a point in time and how wealth accumulation varies over time for the same individual (Charles & Hurst, Reference Charles and Hurst2003; Boserup et al., Reference Boserup, Kopczuk and Kreiner2017; Black et al., Reference Black, Devereux, Landaud and Salvanes2020). Understanding sources of inequality is important from a social policy perspective especially if it is unearned, for example as in the case of inheritances, rather than due to individual’s own efforts, and for this reason understanding wealth inequality is equal to or possibly even more important than understanding, say, income inequality. Importantly, evidence suggests wealth holdings and inequality are increasingly stratified by family background in advanced economies, and there is a rapid widening of wealth inequalities, which is concerning from a policy perspective in the context of improving social mobility and living standards more generally (Glennerster, Reference Glennerster2012; Killewald et al., Reference Killewald, Pfeffer and Schachner2017; Gregg & Kanabar, Reference Gregg and Kanabar2022).

When considering wealth inequalities across individuals at a point in time and how these relate to family background, it is important to note that certain types of wealth matter more than others. In Britain this is typically housing and pension wealth (Hamnett, Reference Hamnett1991; ONS, 2019). Given the rapid increase in intergenerational wealth persistence in Britain (Gregg & Kanabar, Reference Gregg and Kanabar2022; Blanden et al., Reference Blanden, Eyles and Machin2023) it is therefore crucial to understand whether parental characteristics are increasingly associated with specific types of offspring wealth holdings, even after controlling for individuals’ own characteristics. Surprisingly, little research has focused on this issue. We address this gap in the literature using high-quality British panel data from the Wealth and Assets Survey (WAS) covering a period post the Great Recession and prior to the Covid-19 pandemic.

We document several important and policy-relevant findings. We show inequality in offspring wealth is related to access to homeownership and housing wealth, and such wealth is increasingly stratified by parental characteristics. For individuals from the same family background but born 6 years apart, relative to the slightly older cohort, parental background is increasingly associated with offspring homeownership and housing wealth. We estimate that over the 6-year period 2010/12–2016/18 the association between the intergenerational rank correlation in housing wealth increases by 0.036 rank points. Given a base correlation of 0.18 our estimates infer a doubling in the rank correlation in approximately three decades.

We find that individuals from the most advantaged parental backgrounds (high educated homeowner parents) are three times more likely to report housing wealth by age 35, and the average level of housing wealth, conditional on holding, is roughly ten times higher compared to individuals from the most disadvantaged background (low-educated renter parents). Moreover, on a cohort basis, those from the most advantaged backgrounds are no less likely to report homeownership and housing wealth compared to older cohorts, whereas the opposite holds true for those from the least advantaged background even after controlling for individual factors including education and earnings, which have been shown to be important in determining wealth accumulation (Black et al., Reference Black, Devereux, Landaud and Salvanes2020; Davenport et al., Reference Davenport, Levell and Sturrock2021). Thus, we show the perceived notion that access to homeownership for cohorts born post-1980 is more nuanced than is generally understood.

Our findings highlight rapidly diverging fortunes for young people, the penalty for growing up in households with limited resources is growing rapidly in Great Britain and is increasingly influencing major lifecycle events including homeownership, wealth accumulation and living standards. Separately, our findings also contribute to the debate on intergenerational fairness.

The rest of this paper is set out as follows: Section two briefly reviews the role of parental characteristics for offspring outcomes with a focus on wealth from an intergenerational perspective, and section three considers data and our methodological approach. In section four we present our findings in two parts. Part one presents cross-section estimates of the association between parental background and offspring wealth outcomes by wealth type. For analysis purposes we allocated individuals into 6-year age groups, to match the length of the sample period used for longitudinal analysis, which constitutes the second part of the section. We demonstrate how the relationship between parental resources on the one hand and wealth of the offspring on the other is changing for the same individuals and, importantly, how rapidly this association is changing for individuals from the same parental background but born 6 years apart. Finally, we show how offspring housing wealth is largely responsible for the rapid change in intergenerational wealth persistence in Britain. Section five concludes.

Literature

A growing body of research has documented vast and growing inequalities in wealth across cohorts and especially in the second half of the 20th century. Understanding the sources of such inequalities has come to the forefront of the policy agenda. In particular, the extent to which wealth inequalities in adulthood are related to family background versus differences in individuals’ own efforts (Hamnett, Reference Hamnett1991). Evidence suggests that the former is important and, moreover, that the effect of family background for explaining wealth inequality is growing over time (Charles & Hurst, Reference Charles and Hurst2003; Piketty, Reference Piketty and Saez2014, Black et al., Reference Black, Devereux, Landaud and Salvanes2020, Gregg & Kanabar, Reference Gregg and Kanabar2022; Blanden et al., Reference Blanden, Eyles and Machin2023).

What is less well understood is which types of offspring wealth have become increasingly related to parental characteristics, a gap we address in this paper. Answers to such questions are important if policymakers and researchers wish to design effective policies to improve wealth and social mobility more generally. To understand wealth inequality, it is important to consider the components of total net wealth, which in Britain is typically dominated by housing and pension wealth. As an illustrative case, using the Wealth and Assets Survey (WAS) dataset we split total net wealth into its individual components for an individual who is aged 64, which corresponds to peak wealth age from a lifecycle perspective. Average total net wealth measured in 2022 prices among this age-group corresponded to £733,884 in 2016/18, of which 50% corresponded to pension wealth and 31% housing wealth. However, it is important to note there is significant variation in wealth holdings at older ages, for example 15% of 64 year olds do not report homeownership. The composition of total wealth looks markedly different among 30 year olds, for example housing and pension wealth combined explain 49% of total net wealth (18% and 31%, respectively). Such differences are, in part, due to age, cohort and time effects. Our interest is to understand how wealth accumulation is changing by family background. In this respect two issues need to be considered; first, having versus not having a particular type of wealth and second, conditional on having the level of wealth held.

Recent studies using British data show that the intergenerational persistence in home ownership has risen across successively younger cohorts and that there exists a strong correlation between the likelihood of offspring homeownership and parental wealth (Davenport et al., Reference Davenport, Levell and Sturrock2021; Blanden et al., Reference Blanden, Eyles and Machin2023). Notably, Davenport et al. (Reference Davenport, Levell and Sturrock2021) find that the intergenerational persistence in wealth is higher than that of income.

Studies based on European microdata find similar results, Gritti and Cutulli (Reference Gritti and Cutuli2021) document declining levels of homeownership across successively younger cohorts and find that housing wealth is increasingly important for explaining within-cohort inequality in total wealth. Their findings highlight the mechanisms by which wealth is transmitted from parent to offspring depends on parental characteristics. Offspring born to parents whose occupation is considered professional are more likely to receive direct financial transfers before, at the time of and after leaving the parental home to set up a new household. Whereas for those whose parents had low social class occupations, this only occurred at the time of leaving the family home. Second, leaving the parental home was associated with a transfer of housing wealth from parents to children among the lowest social classes. Thus, parents transfer their own accumulated housing wealth at the time offspring leave the parental home. No such pattern was observed among those from the most advantaged backgrounds, whose parents instead provide more sustained levels of financial transfers without having to transfer their own housing wealth. Nevertheless, offspring from such backgrounds still receive housing wealth later in life in the form of inheritance. These findings separately underline the role of social and cultural norms for determining offspring wealth.

Pfeffer and Waitkus (Reference Pfeffer and Waitkus2021) using the Luxembourg Wealth Study decompose country differences in wealth inequality and consider the composition of wealth portfolios. Their results show that cross-national variation in wealth inequality and concentration is driven by housing equity. Given the returns from homeownership over the lifecycle, the fact homeownership has become increasingly stratified by family background has implications for future wealth inequalities both from a cross section, intergenerational and lifecycle perspective (Killewald et al., Reference Killewald, Pfeffer and Schachner2017; Gritti & Cutulli, Reference Gritti and Cutuli2021).

The channels by which parents’ transfer resources from one generation to next are varied, for example investing in early life education either directly or indirectly by residing in certain neighbourhoods with high-quality state schooling, both in turn influence future earnings and hence wealth accumulation. Such relationships are also important for explaining aggregate level cross-country differences in wealth-income inequality ratios (Piketty, Reference Piketty and Saez2014; Pfeffer & Killewald, Reference Pfeffer and Killewald2015; Black et al., Reference Black, Devereux, Landaud and Salvanes2020; Palomino et al., Reference Palomino, Marrero, Nolan and Rodríguez2021). Measured on this basis the U.K., Italy and France exhibit significantly higher wealth-income ratios than Norway and the U.S. (Black et al., Reference Black, Devereux, Landaud and Salvanes2020). Alongside offspring’s own education, higher levels of parental education are strongly correlated with offspring earnings, homeownership and pension wealth (Card, Reference Card1999; Goodman & Mayer, Reference Goodman and Mayer2018; Girshina, Reference Girshina2019). Separately, comparative evidence shows a strong intergenerational persistence in education, which in turn influences offspring earnings and wealth (Blanden, Reference Blanden2013; Lindahl et al., Reference Lindahl, Palme, Massih and Sjögren2015). Taken together the evidence suggests family background is important for influencing the channels that determine wealth accumulation and will explain an increasingly larger fraction of wealth inequalities across successively younger cohorts in the future. We contribute to the literature by confirming this conjecture.

Studies have highlighted the importance of controlling for individual’s own characteristics when analysing intergenerational wealth inequalities across cohorts (Killewald et al., Reference Killewald, Pfeffer and Schachner2017; Black et al., Reference Black, Devereux, Landaud and Salvanes2020; Davenport et al., Reference Davenport, Levell and Sturrock2021). Black et al. (Reference Black, Devereux, Landaud and Salvanes2020) using Norwegian data show individual’s own labour income and net capital gains on real assets, such as housing, play an important role when compared to parental transfers and inheritances in explaining wealth inequalities. Nevertheless, the authors show that offspring from the wealthiest backgrounds are more likely to have higher levels of wealth, receive greater levels of inheritance and accumulate a disproportionate amount of wealth from investments and capital income. Davenport et al. (Reference Davenport, Levell and Sturrock2021) estimate roughly half of the intergenerational persistence in wealth in the U.K. can be explained by individual’s own education and earnings, and thus parental transfers and savings play an important role in explaining wealth inequalities.Footnote 1 However, whilst research has shown an association between income and wealth particularly at the top of both respective distributions, at an aggregate level there exists a non-correlation between income and wealth inequality (Killewald et al., Reference Killewald, Pfeffer and Schachner2017; Pfeffer & Waitkus, Reference Pfeffer and Waitkus2021).

A common mechanism closely linked to social and cultural norms by which wealth is transferred is via lifetime transfers. Studies show the uneven nature of inheritance distribution in the U.K. and the growing importance of parental homeownership in this context (Hamnett, Reference Hamnett1991). Palomino et al. (Reference Palomino, Marrero, Nolan and Rodríguez2021) show certain factors, predominantly inheritances, jointly explain between one-third and almost one-half of wealth inequalities in Great Britain and France, respectively. Decomposing their findings, the authors show intergenerational transfers alone explain between 26% and 36%, whereas family background explains between 9% and 17% of inequality in France and the U.S., respectively. Importantly, evidence suggests individuals from the most advantaged backgrounds tend to deplete inheritances at a slower rate, and in long run even in relatively egalitarian societies such as Sweden inheritances tend to increase wealth inequality (Nekoei & Seim, Reference Nekoei and Seim2023). Boileau and Sturrock (Reference Boileau and Sturrock2023) using WAS instead focus on inter-vivo transfers and like inheritances find these are stratified in terms of their prevalence and magnitude by parental characteristics.

Data and methodology

Our analysis uses the biennial WAS representative of Great Britain and managed by the Office for National Statistics (ONS, 2012). In wave 1 WAS contained 30,000 households oversampling wealthier households (by a rate of between 2.5 and 3) compared to other postal addresses due to household surveys inadequately capturing the top of the wealth distribution (ONS, 2012; Advani, Bangham, et al., Reference Advani, Bangham and Leslie2020). Our study is based on secondary data and as such any ethical considerations regarding data collected was gained by the primary data collection and management team at the ONS.

WAS measures of derived individual total net wealth include contributions of housing, pension and savings plus durable assets. Black et al. (Reference Black, Devereux, Landaud and Salvanes2020) exclude pension wealth from their measures of total net wealth (it is not available in their data) and argue such wealth should not be included when modelling wealth accumulation. However, our interest is understanding the components of offspring wealth driving the rapid change in the intergenerational persistence in wealth. Even if pension wealth is not transferable, consider the parent generation who can expect income from such wealth (and/or a lump sum as is the case in the U.K.). This could act as security, or alternatively, parents knowing this wealth is available to them in the future can utilise or transfer other sources of wealth, for example releasing equity from their main residence to help provide financial support to their offspring, such as to purchase their first home. Turning to the offspring generation, given our aim is to understand which components of wealth are correlated with parental resources, and housing and pension wealth having been shown to be the two largest subcomponents of total wealth in Great Britain (ONS, 2019), we also include offspring pension wealth in our measure of total wealth when analysing changes in intergenerational correlations over time. Pension wealth is strongly correlated with earnings/labour income and if the relationship between parental wealth and offspring pension wealth is changing over time this is informative for understanding potential transmission mechanisms, such as early life education investments and hence whether educational attainment and/or occupation is driving changes in wealth inequalities.

Definitions of each derived measure used in the analysis can be found in online Appendix A. Information of mortgage and non-mortgage debt is also captured. The inclusion of durable assets means that net wealth is never zero or negative for individuals in our sample.Footnote 2 Black et al. (Reference Black, Devereux, Landaud and Salvanes2020) show total net wealth measures such as those provided in the WAS dataset which by construction account for individual consumption and spending/saving decisions act as good proxies for ‘potential wealth’, based on actual future wealth accumulation that is not affected by such issues. In addition to asset and debt information, WAS collects individual and household level socioeconomic and demographic data including retrospective information relating to individual’s parent’s circumstances when they were teenagers (aged around 14).

Retrospective family background and early life questions

We seek to understand an offspring’s trajectory of holding certain housing, pension, financial and physical wealth as they age and their value by differing family origins. Whilst WAS does not collect information on parental wealth except in the case where adult children live in the same household as their parents, the survey does collect retrospective socioeconomic information relating to survey respondent’s parents which have been shown to be important determinants of household’s resources early in life and offspring’s future outcomes (Johnson & Schoeni, Reference Johnson and Schoeni2011; Blanden et al., Reference Blanden2013; Jerrim & Macmillan, Reference Jerrim and Macmillan2015; Gregg et al., Reference Gregg, Macmillan and Vittori2017). As wealth accrual will continue after a young adult has left home (Killewald et al., Reference Killewald, Pfeffer and Schachner2017; Boserup et al., Reference Boserup, Kopczuk and Kreiner2017; Adermon et al., Reference Adermon, Lindahl and Waldenström2018; Black et al., Reference Black, Devereux, Landaud and Salvanes2020; Gregg & Kanabar, Reference Gregg and Kanabar2022), the age at which these are collected is not the focus but rather they are markers for assessing relative resources of the parents.

We utilise these data to construct a marker of parental resources in the form of a rank estimator described in the methodology section. Specifically, survey respondents in WAS are asked to recall circumstances in their early teenage years relating to:

-

(1) their parents housing tenure

-

(2) their parent(s) education level

-

(3) employment status of parents

-

(4) whether they lived with one or both parents or some other arrangement

-

(5) number of siblings

Unfortunately, region of parents’ residence and parental age were not asked.Footnote 3 For the purpose of this study we focus on (1) and (2) to construct a measure of parental resources. We choose markers that can be thought of as being relatively stable, given the point in the lifecycle at which they are measured and their correlation with available resources in the home. Indeed, both education and housing tenure have been shown to be important predictors of total wealth (Kaas et al., Reference Kaas, Kocharkov and Preugschat2019; Pfeffer & Waitkus, Reference Pfeffer and Waitkus2021).Footnote 4 Other retrospective markers collected in WAS such as economic status and whether an individual grew up in a single or two parent household, whilst related to resources in the household, could be considered as transitory due job loss and relationship breakdown respectively. Keister (Reference Keister2003) highlights the role of sibling status in determining the likelihood and size of wealth transfers from one generation to the next, and notes the effect is mitigated by parent education (& offspring education and income), providing further justification for basing our marker of parental resources on these variables. We interact parental housing tenure and education to define the parental groups of interest, these are converted into an ordering (rank) which is used for analysis purposes. Combining additional parental characteristics would lead to a richer ordering, however at the cost of small cell sizes and what is feasible for analysis purposes.Footnote 5

Thus, readers should interpret our estimation results keeping in mind the set of parental characteristics used to proxy early life resources in the household. However, to demonstrate the robustness of our findings, we control for the presence of siblings in the household when individuals were growing up, offspring education and income in the regression specifications in Table 5 and note our main findings hold.

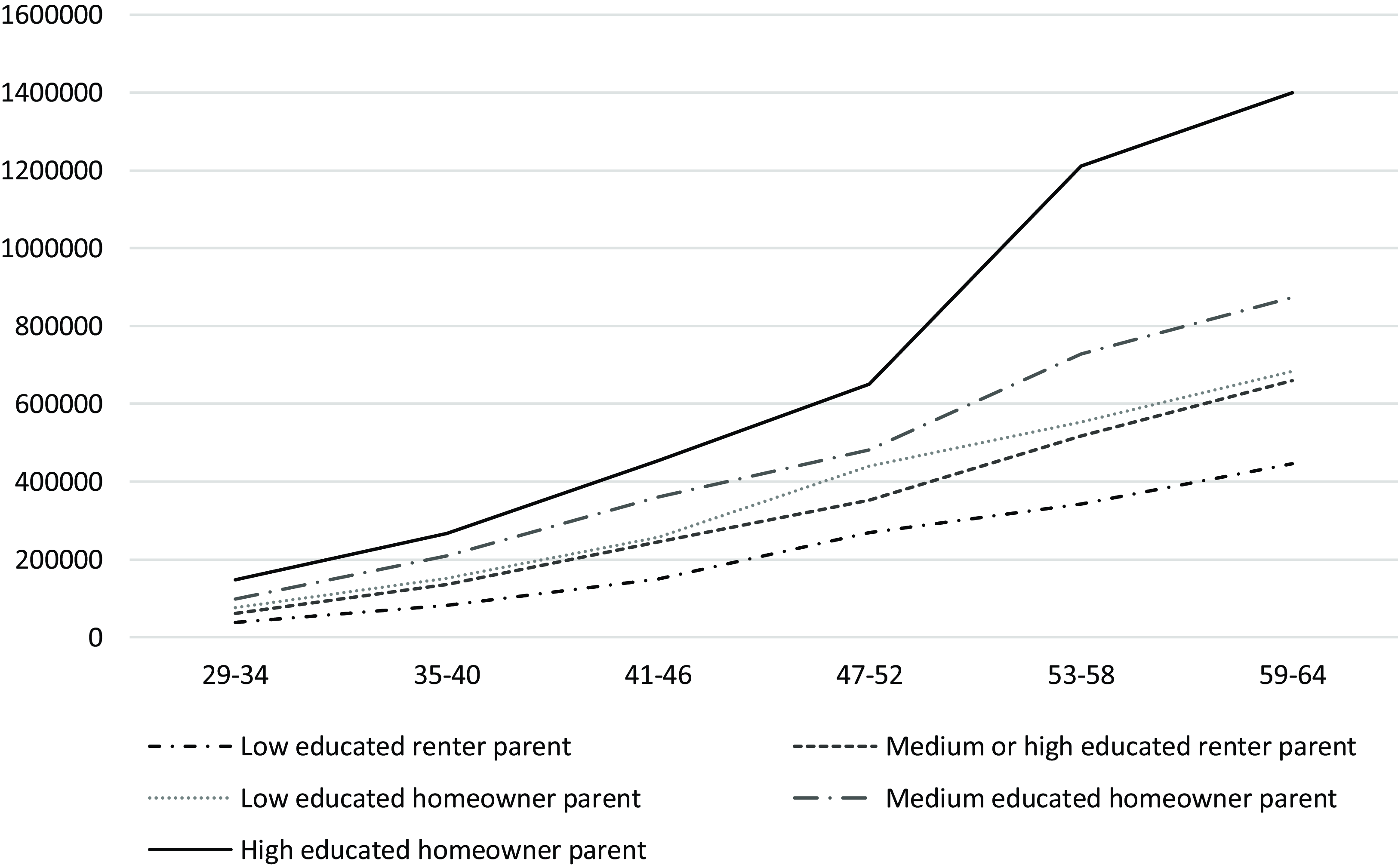

To assess whether parental markers act as good proxy measures for resources early in life and the fact we construct a rank estimator (defined in the next section) based on these same markers, we plot total offspring wealth, stratified by parental education and housing tenure using the wave 3 cross section sample of WAS. In practice we create five groups due to small cell sizes for individuals whose parents were medium or highly educated renters. Online Appendix B includes additional plots by wealth type stratified by parental characteristics. Figure 1 provides a description of wealth profiles across different individuals, belonging to different birth cohorts at a single point in time. We are implicitly assuming rank stability in parental resources, which based on housing tenure and education, is not an unreasonable assumption, even if the parent cohorts experienced differing home ownership and educational attainment opportunities. Thus, in terms of the rank ordering and the relationship with respect to resources in the household it is reasonable to assume this remained unchanged. We separately verify this for a sample of parents in WAS which we discuss next.

Figure 1. Total net wealth by family background.

Notes: Sample based on wave 3 of WAS (2010/12). N = 13,330. Figures correspond to 2022 prices.

Figure 1 shows a clear ordering in total net wealth by family background. Offspring from relatively more advantaged backgrounds report higher levels of total net wealth across all age groups up until peak wealth age. From a cross section perspective, the extent of wealth inequality is striking, offspring from the most advantaged background report levels of net wealth by age 41–46 of a similar level to that achieved by those from the least advantaged background (albeit relating to an older cohort) in their mid 60s, which corresponds to peak wealth age. Importantly, we note this is prior to the age at which inheritances are received, which typically occur when an individual is in their 50s and is clearly visible, particularly for the most advantaged groups in Figure 1.

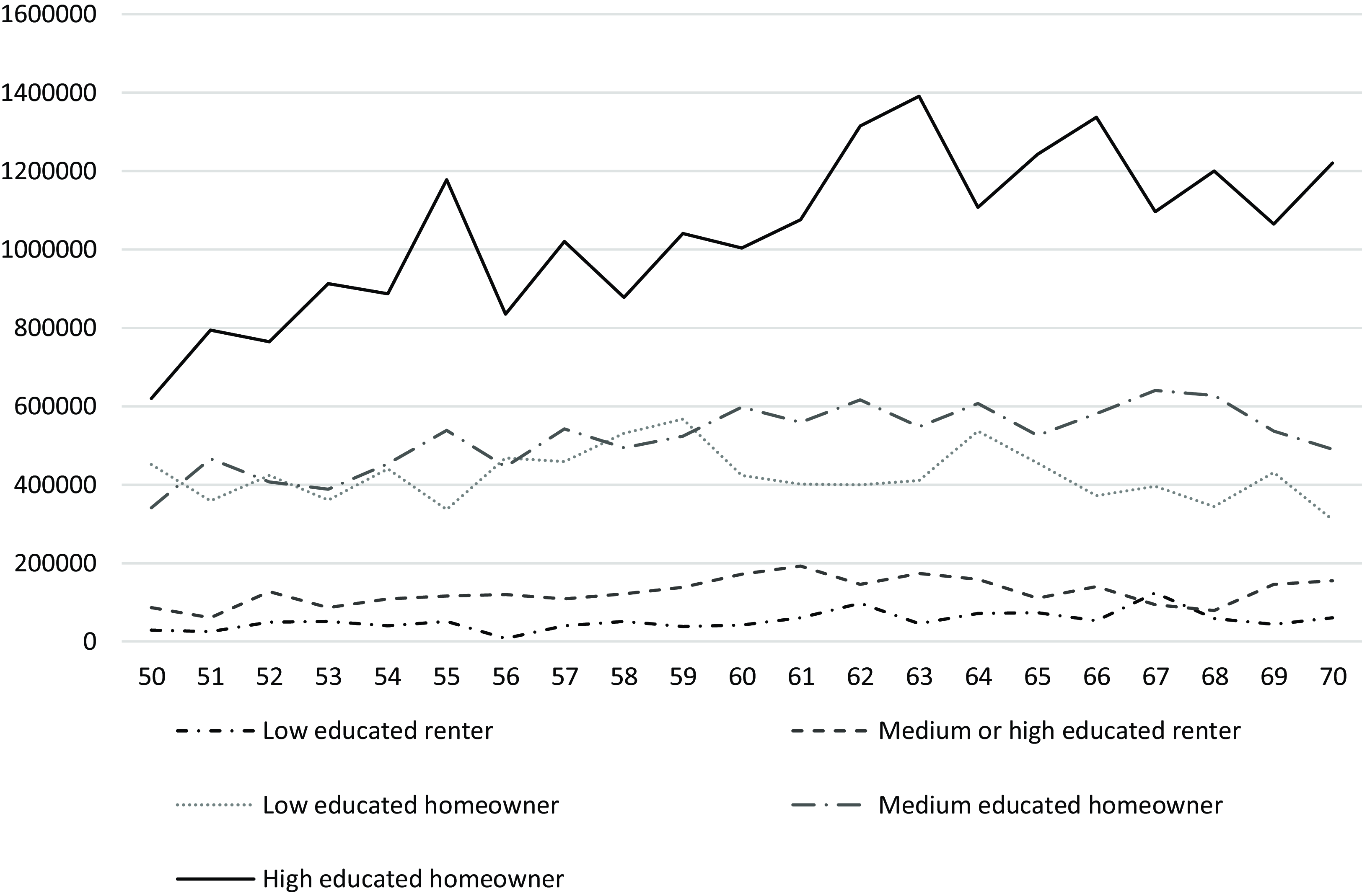

The markers of household resources refer to characteristics of the parents when offspring are in their teens and parents aged around 40, given average age of first birth in the U.K. (ONS, 2022). Intergenerational correlations in wealth are usually measured when parents are at peak wealth age, around 64 in Great Britain. So, our estimates of parental resources are measured before parents reach peak wealth age. Whilst we do not have data on parental wealth, we can at the minimum verify if the rank ordering we assume is consistent with the profile of wealth accumulated by individuals aged 50–70, by their own housing and education characteristics in wave 3 of WAS.Footnote 6

This group of individuals are born between 1940–1960 so are relatively young given our sample of offspring includes individuals up to their mid 60s; however, it does provide partial evidence based on data available in the same study that the choice of parental markers we use accurately reflects parental resources in the household an individual grew up in. These ‘parents’ roughly correspond to the parent cohort for the youngest offspring in our sample born around 1980 in Figure 2, and importantly, allows us to trace out the general pattern of wealth accumulation among these ‘pseudo parents’ who share these same characteristics in wave 3 of WAS.

Figure 2. Total net wealth by single age year and own characteristics.

Notes: Sample based on wave 3 of WAS (2010/12). N = 9,726. Figures correspond to 2022 prices.

Figure 2 shows a clear ordering by own housing tenure and education group in terms of total net wealth, across the majority of ages considered, suggestive that the differences in household resources when raising children hold, at least from a cross-section perspective among individuals who are of a similar age to the youngest parents in our sample.

In addition to providing a visual depiction between parental characteristics and wealth levels among pseudo parents we also create a rank ordering, based on the same covariates used in the main analysis, namely interacting own housing tenure and education to determine the correlation between pseudo parent characteristics in wave 3 of WAS and their own actual level of total net wealth, which is measured in the survey. Undertaking such an exercise yields a correlation of 0.61, which is remarkably high.

Methodology

Starting from wave 3 onwards (2010–12) WAS released consistent measures of individual total wealth and its subcomponents including housing, pension, financial and physical wealth (defined in online Appendix A). When using wealth data two issues need to be addressed (Pence, Reference Pence2006). First, wealth data has a long thick right-hand tail where some very high values can lead to misleading conclusions when assessing relationships at the mean such as with ordinary least squares regression, and so analysis across the respective offspring and parental distribution is important (Killewald et al., Reference Killewald, Pfeffer and Schachner2017). Second, individual total net wealth reported in WAS is not zero or negative except for a very small number of individuals at young ages because a wide range of assets including durable goods and physical wealth are included. However, subcomponents of wealth such as housing and pension wealth are zero, especially at younger ages, and this value is economically meaningful and should be accounted for in analysis.

We follow previous studies and estimate the intergenerational correlation in wealth using a rank estimator (Chetty et al., Reference Chetty, Hendren, Kline, Saez and Turner2014). The rank estimator relies on ordering individuals based on certain characteristics, from lowest to highest value. Parental wealth rank, our independent variable of interest, is based on housing tenure (two groups) and education (three groups) interacted. We view these characteristics as markers of parental resource both independently and jointly, in online Appendix C we plot offspring total wealth separately by each characteristic and find the ordering of wealth follows a very similar pattern to that reported in Figure 1. Thus, from an intergenerational perspective we view these are reinforcing or complementary markers of (dis)advantage. Whilst major homeownership and education expansion took place in different time periods (the former in the 1930s, 1950s and 1960s, and the latter starting in the 1960s), for most of the 20th and 21st century homeowners have experienced positive returns to housing wealth (Chambers et al., Reference Chambers, Spaenjers and Steiner2021).

The expansion of tertiary education beginning in the 1960s was predominantly taken up by individuals from relatively affluent backgrounds and has been partly attributable for the wage polarisation observed in the U.K. in the 1970s and 1980s but not after this period (Machin, Reference Machin2011; Blundell et al., Reference Blundell, Green and Jin2022), allowing graduates to purchase housing in relatively more desirable areas, often major cities where high-paying jobs are located. Over time, such neighbourhoods have experienced sharp earnings and house price growth, in part also due to supply constraints and regulation (Hilber et al., Reference Hilber and Vermeulen2016). Whilst education is relatively more accessible for younger cohorts irrespective of family background, and there is greater variation in the monetary returns to a degree, from an intergenerational wealth perspective and given our main findings, a priori there is no reason to believe that there is likely to be a decoupling between parental housing tenure and education in the future, to the extent that these characteristics will stop playing an important role in explaining intergenerational wealth dynamics.

For analysis purposes we define five groups, and due to small cell sizes we combine individuals whose parents were medium or highly educated renters. Parent’s rank then takes the value 1-5, which is converted to a scale that runs from zero to one for estimation purposes. Our dependent variable is offspring wealth, which can take the form of total wealth or one of the other derived measures of wealth available in WAS (defined in online Appendix A). We then derive the rank of offspring wealth based on their actual wealth as measured in WAS and transform this to take a value between zero and one for estimation purposes.

Our estimating equation of interest is given by:

$${R_{{\rm{offspring}},{\rm{current\;age}}}} = \alpha + \gamma {R_{{\rm{parent}}}} + \beta {X_{{\rm{offspring}}}} + \varepsilon $$

$${R_{{\rm{offspring}},{\rm{current\;age}}}} = \alpha + \gamma {R_{{\rm{parent}}}} + \beta {X_{{\rm{offspring}}}} + \varepsilon $$

where

${R_{{\rm{offsrpig}},{\rm{current\;age}}}}$

refers to the rank of wealth of the offspring for a particular derived net wealth measure (total, housing, pension, financial or physical) at their current age.

${R_{{\rm{offsrpig}},{\rm{current\;age}}}}$

refers to the rank of wealth of the offspring for a particular derived net wealth measure (total, housing, pension, financial or physical) at their current age.

$\gamma $

refers to the intergenerational correlation that corresponds to the association between parental characteristics and offspring wealth, higher values implying a stronger relationship between resources during teenage years and wealth outcomes measured in adulthood. We also include additional individual and household level controls that may be correlated with offspring wealth to isolate our coefficient of interest,

$\gamma $

refers to the intergenerational correlation that corresponds to the association between parental characteristics and offspring wealth, higher values implying a stronger relationship between resources during teenage years and wealth outcomes measured in adulthood. We also include additional individual and household level controls that may be correlated with offspring wealth to isolate our coefficient of interest,

$\gamma $

. We do not include time subscripts in (1); however, note that cross section analysis is undertaken at wave 3 (2010/12) and panel analysis uses waves 3 and 6, which corresponds to 2010/12–2016/18. The pooled sample (where we combine all waves/rounds) also corresponds to waves 3–4 and rounds 5–6. Standard errors are clustered at the individual level for analysis purposes.

$\gamma $

. We do not include time subscripts in (1); however, note that cross section analysis is undertaken at wave 3 (2010/12) and panel analysis uses waves 3 and 6, which corresponds to 2010/12–2016/18. The pooled sample (where we combine all waves/rounds) also corresponds to waves 3–4 and rounds 5–6. Standard errors are clustered at the individual level for analysis purposes.

The main advantage of using a rank estimator for analysis is that it doesn’t require data on parental wealth, instead relying on the retrospective parental characteristics discussed in the previous subsection and informed by the literature review to proxy household resources during offspring’s teenage years. An alternative approach to estimate the intergenerational association between parents and offspring wealth would be to use a two stage estimator (see inter-alia Dearden et al., Reference Dearden, Machin and Reed1997), which requires predicting a value of parental wealth; however, such estimators suffer from various biases pertaining to correct estimation of the variance in the second stage of the regression (due to parental wealth being estimated, also known as a ‘generated regressor’), lifecycle bias (due to age effects and not observing wealth for all individuals at peak wealth age) and measurement bias (see Murphy & Topel, Reference Murphy and Topel1985; Wooldridge, Reference Wooldridge2002). Rank-Rank regression provides an accurate estimate of the intergenerational rank correlation and is more efficient but does not capture wealth inequalities within cohorts or generations, just the degree of re-ordering of individuals.Footnote 7 Therefore our analytical approach cannot formally account for the size of wealth inequalities in the offspring and parent generation and how the association between these two quantities is changing over time from an intergenerational perspective.

Our estimates will be affected by the profile of lifecycle wealth accumulation, which typically exhibits a rapid divergence before and after peak wealth age (64) and this is attributable to both age and cohort effects. Whilst the absolute level of wealth differences expand as people move closer to retirement, wealth inequality as measured by the Gini has been shown to decline (within age group) across successively older age groups (Cowell et al., Reference Cowell, Nolan, Olivera and Van Kerm2017). Gregg and Kanabar (Reference Gregg and Kanabar2022) show the inequality in wealth at younger ages in Great Britain is such that it is sufficient to overturn the lifecycle bias. Separately, Boserup et al. (Reference Boserup, Kopczuk and Kreiner2016, Reference Boserup, Kopczuk and Kreiner2018) and Adermon et al. (Reference Adermon, Lindahl and Waldenström2018) using Scandinavian data find the intergenerational persistence in wealth follows a U-shape, namely that the rank-rank measure is higher at younger ages, declines as individuals age up until their 40s and then increases following the death of their parents. Thus, the underlying ordering of people by own and parental wealth holdings is also heavily influenced by bequests and need not have the same age relationship as the amounts of wealth held. In Rank-Rank regression lifecycle biases are much smaller as inequalities have no influence, just the rank ordering. Indeed, as parental characteristics are observed even if deceased, this allows us to analyse the relationship between offspring and their parents without needing to adjust for the lifecycle bias and hence offers us a common approach to estimating the association between offspring wealth and parental characteristics for all ages. No adjustment to correct for lifecycle issues is required for the offspring generation as our central interest is understanding how inequality in current wealth holdings by wealth type (not peak) relates to parent’s characteristics.

The estimates for different age groups reported in the next section will both reflect lifecycle differences across age but also differences across cohorts. Such cohort differences in wealth accumulation have been shown to be significant from an intergenerational perspective (Resolution Foundation, 2018) and we return to this issue by considering wealth accumulation by wealth type across cohorts and over time in the final part of section “Estimation results”. We also utilise the short panel to explore lifecycle changes within cohorts. Over a 6-year period we show the evolution of the estimated Rank correlation, by wealth type, as people age and by a chain extension over the lifecourse. We pool wave 3 and round 6 of WAS to compare how the Rank correlation is changing for each wealth type across the 6-year period between survey waves (2010/12 and 2016/18) for individuals at the same age except born 6 years apart. We use an identical approach to assess whether parental wealth is becoming increasingly associated with homeownership across successively younger cohorts.

Estimation results

We present our findings in two parts. First, we analyse intergenerational associations between parent resources which proxy parental wealth for modelling purposes, and offspring wealth for different wealth types using wave 3 (2010–12) and round 6 of WAS (2016–18); the second part of the findings analyse changes for the same individuals over time. To match the longitudinal analysis sample period length, we define age groups using 6-year age windows. By defining age groups in this way, we can compare cohort on cohort changes at the same age and by chain extension analyse the trend across the lifecycle. This allows us to highlight the role parental background has in explaining the change in the intergenerational persistence in wealth, by wealth type, across time rather than drawing inference based on a single cross section. An important aspect to consider is offspring holding a certain type of wealth versus level differences conditional on holding, and we show parental wealth plays an increasingly important role when considering this distinction both from a cohort and intergenerational perspective.

Cross section analysis

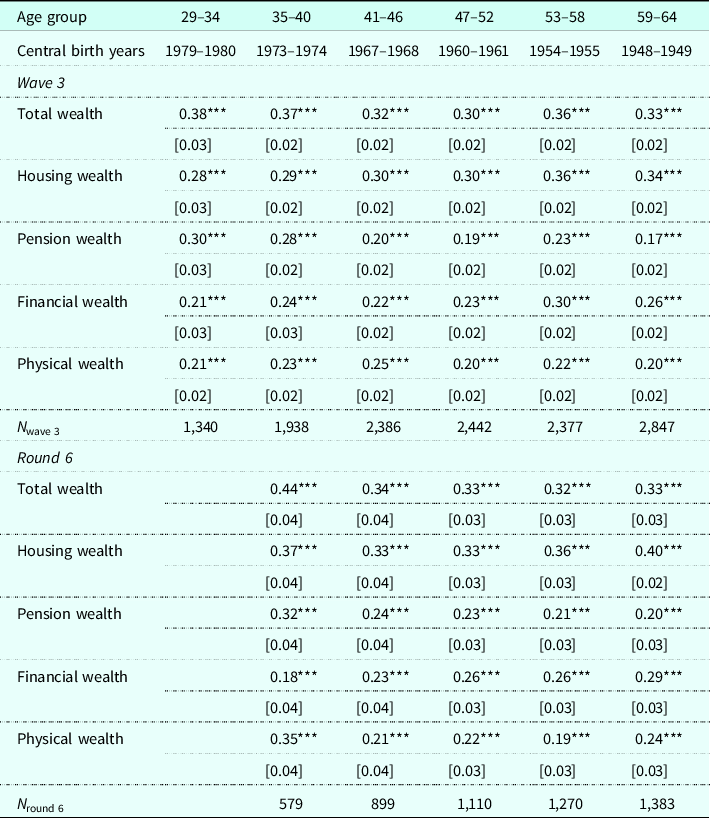

Table 1 reports intergenerational rank correlations for different wealth types. Importantly, zero holdings of certain wealth types, which are economically meaningful, can be accommodated for. Table 1 shows parental characteristics are strongly associated with all types of wealth measured in WAS. The magnitude of the estimated coefficients in Table 1 is remarkably stable across age groups in the case of housing, financial and physical wealth, irrespective of the wave/round of data considered. The estimates at wave 3 (2010/12) imply that increasing total parent wealth by one decile leads to offspring housing wealth (financial wealth, physical wealth) increasing by approximately 2.8–3.6 (2.1–3, 2–2.5) rank points. In the case of pension wealth, across successively younger cohorts the rank estimate increases, from 0.17 for those aged between 59 and 64 to 0.3 among individuals aged between 29 and 34, which is identical to the rank estimate calculated for housing wealth for the latter group.

Table 1. Cross section rank correlations at wave 3 and round 6 by wealth type

Notes: Respective regressions model rank of offspring wealth level on age and rank of parent’s total wealth. Standard errors clustered at individual level. Empty cells refer to age groups where sample size is too small for estimation purposes. Wave 3 of WAS corresponds to (2010–12) and wave 6 (2016–18). Wealth values adjusted for inflation prior to transformation and reflect 2022 prices.

The channels that determine the strength of the association between parental resources and offspring wealth types is unlikely to be the same for a variety of reasons, including age, cohort and time effects. Nevertheless, family background matters. As an illustration, consider the effect of early life investments on offspring education, which have been shown to influence subsequent education attainment and earnings (Card, Reference Card1999). Such investments are more commonly made by parents who are relatively better off. In terms of the offspring generation, higher levels of educational attainment is associated with occupational choice and in particular accessing higher paying jobs that influence pension wealth accumulation. However, the intergenerational association between parent and offspring education, earnings and pension wealth accumulation need not be the same. Nevertheless, higher earnings, over and above direct transfers from parents, mean offspring from more advantaged backgrounds are also more likely to report homeownership and conditional on owning property, accumulate housing wealth more rapidly compared to individuals from less advantaged backgrounds. A separate and related point is that certain wealth types will represent a greater proportion of total net wealth depending on the age at which wealth is measured in the offspring lifecycle. Table 1 documents trends across age groups at a single point in time. Arguably, a more informative approach is to compare groups at the same age to understand whether the intergenerational correlation has changed for individuals from the same parental background except born 6 years apart. We turn to this next.

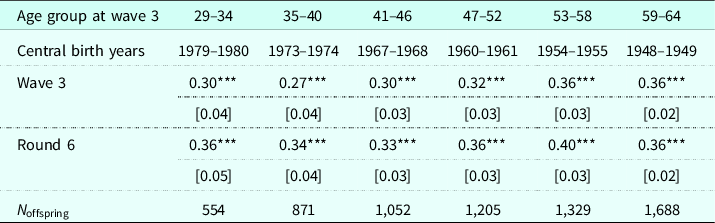

Panel analysis

Table 2 reports rank correlations for the same individuals at wave 3 and 6 years later at round 6, allowing us to document the change in the intergenerational correlation of wealth by wealth type for the same individual. We report intergenerational correlations for total and housing wealth only as the latter is responsible for driving the change in the persistence in wealth (see Tables 4 and 5), for interested readers we report the intergenerational correlation coefficient for pension, financial and physical wealth in online Appendix D.

Table 2. Balanced panel intergenerational rank correlation estimates for total wealth by age group

Notes: ***p < 0.01, **p < 0.05, *p < 0.1. Wealth values adjusted for inflation prior to transformation and reflect 2022 prices.

Table 3. Balanced panel intergenerational rank correlation estimates for housing wealth by age group

Notes: ***p < 0.01, **p < 0.05, *p < 0.1. Specifications control for single year age dummies. Wealth values adjusted for inflation prior to transformation and reflect 2022 prices.

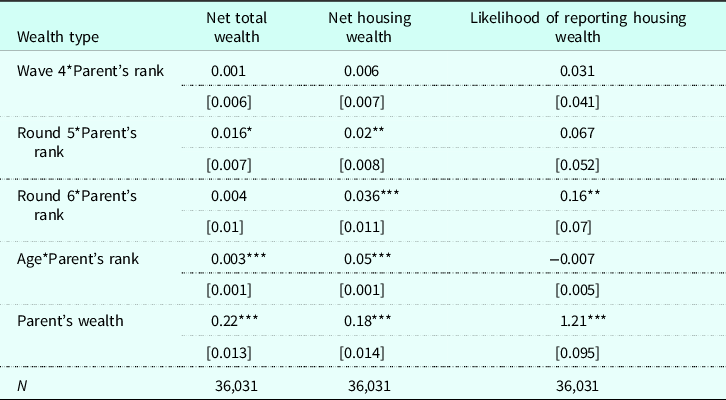

Table 4. Rate of change in the intergenerational rank correlation between 2010/12 and 2016/18 of total net wealth and net housing wealth and likelihood of reporting housing wealth

Notes: ***p < 0.01, **p < 0.05, *p < 0.1. Wealth values adjusted for inflation prior to transformation and reflect 2022 prices. All specifications also control for first and second order polynomial terms in age and wave dummies.

Table 2 shows the rank correlation is largely stable for older ages groups at the same age except born 6 years apart, whereas for the youngest age group parental characteristics are playing an increasingly important role in explaining offspring total net wealth outcomes.Footnote 8 A key question then is to understand which types of wealth held by offspring are driving this change.

Table 3 reports rank estimates for net housing wealth. By comparing the diagonal cells in adjacent age groups, the general pattern is clear: The correlation is larger for successively younger cohorts at the same age. Thus, parental resources are increasingly associated with housing wealth. Two key issues need to be understood in this context (i) the role of parental characteristics on offspring reporting homeownership and conditional on having, the level of housing wealth. A related and important issue is to quantify the change in the intergenerational correlation over time. To explore each of these issues in turn, we pool waves/rounds 3–6 of WAS corresponding to the period 2010/12–2016/18. We report equivalent regressions for pension, financial and physical wealth in online Appendix E.

Table 5. Homeownership and housing wealth controlling for individual’s characteristics

Notes: ***p < 0.01, **p < 0.05, *p < 0.1. Base groups: No siblings, employed, married, degree, North East, professional and male. Outcomes relating to offspring wealth measured in 2022 prices and converted to rank.

Rows 3 and 4 of column 2 in Table 4 show the joint interaction between the survey wave dummies and parental rank is positive and significant at conventional levels. Between 2010/12 and 2016/18 the rank correlation grew by 0.036 rank points on a base of 0.18. This implies a doubling in the intergenerational correlation between parental characteristics and offspring housing wealth in approximately three decades if this rate of change is maintained. Thus, even after controlling for individuals’ own education, which in itself is an important determinant of homeownership, and the fact access to higher education has been expanded to all social classes via the student loan system, our findings underline both parental housing tenure and education, independently and jointly, are increasingly important for explaining housing wealth inequality in Great Britain.

The final column of Table 4 reports estimated coefficients from a probit regression of the likelihood of offspring reporting homeownership. Consistent with the findings in column 2, which relate to housing wealth (that is, conditional on homeownership), our results suggest that over the relatively short sample period considered in this study and ending in 2016/18 the likelihood of reporting homeownership is increasingly related to parental resources as proxied by housing tenure and education for individuals of the same age except born 6 years later.

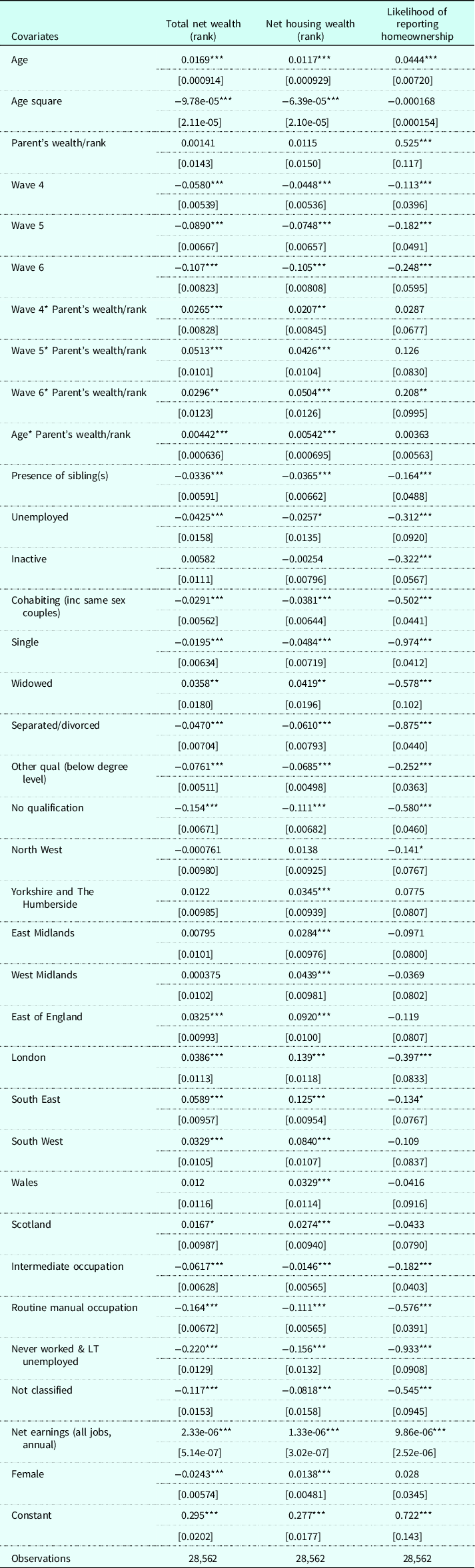

The ability to purchase a home is related to both individual and parental characteristics. To understand the relative importance of the latter we estimate similar regression specifications to those reported in Table 4, except now we control for offspring’s own education, earnings, social class, economic status, presence of siblings, marital status, gender and region. From a modelling perspective, adding individual levels controls to the regression will bias down the effect of parental characteristics on offspring wealth. Nevertheless, these have been shown to be important in explaining homeownership from an intergenerational perspective in Britain (Blanden et al., Reference Blanden, Eyles and Machin2023; Davenport et al., Reference Davenport, Levell and Sturrock2021). Our interest is to document whether the findings reported in Table 4 regarding the increasingly important role family background plays over time and across successively younger cohorts still holds once we control for such characteristics.

Columns 2 and 3 of Table 5 show that after controlling for a rich set of individual characteristics, we observe no direct correlation between family background and total net (housing) wealth of offspring. Nevertheless, there is a strong positive correlation between our markers of parental resources when interacted with the survey wave dummies consistent with our previous results: that parental characteristics are increasingly associated with offspring wealth outcomes. In both regression specifications we also note individuals’ characteristics are also important for determining offspring net (housing) wealth. Residing in certain regions such as London, South East, South West and East of England is strongly associated with having higher total (housing) net wealth. On the other hand, presence of siblings, being unemployed, having a lower level of educational attainment and working in lower skilled occupation is associated with lower wealth levels.

The final column of Table 5 reports estimated coefficients from a regression of whether offspring report housing wealth. In this case we find a strong positive correlation between parental resources and homeownership. We also find that this relationship is growing stronger over our sample period for individuals from the same parent background except born 6 years apart. Ceteris paribus, we find the probability of reporting homeownership is lower in London and the South East of England, consistent with the fact house prices are significantly higher than elsewhere in Great Britain. We note, holding all else constant, that offspring with siblings are 16 percentage points less likely to report homeownership, consistent with the notion that parental resources are divided among a greater number of recipients (Keister, Reference Keister2003). Similarly, we find individuals with lower levels of educational attainment and working in lower skilled occupations are less likely to report homeownership. Finally, age is positively correlated with homeownership, which likely reflects lifecycle effects.

Taken together the findings in Tables 4 and 5 highlight that homeownership and housing wealth are becoming increasingly stratified by parental characteristics. To assess the extent of the divergence in homeownership and housing wealth we exploit the panel dimension of WAS to show the rate at which individuals accumulate housing and housing wealth by family background across successively younger cohorts.

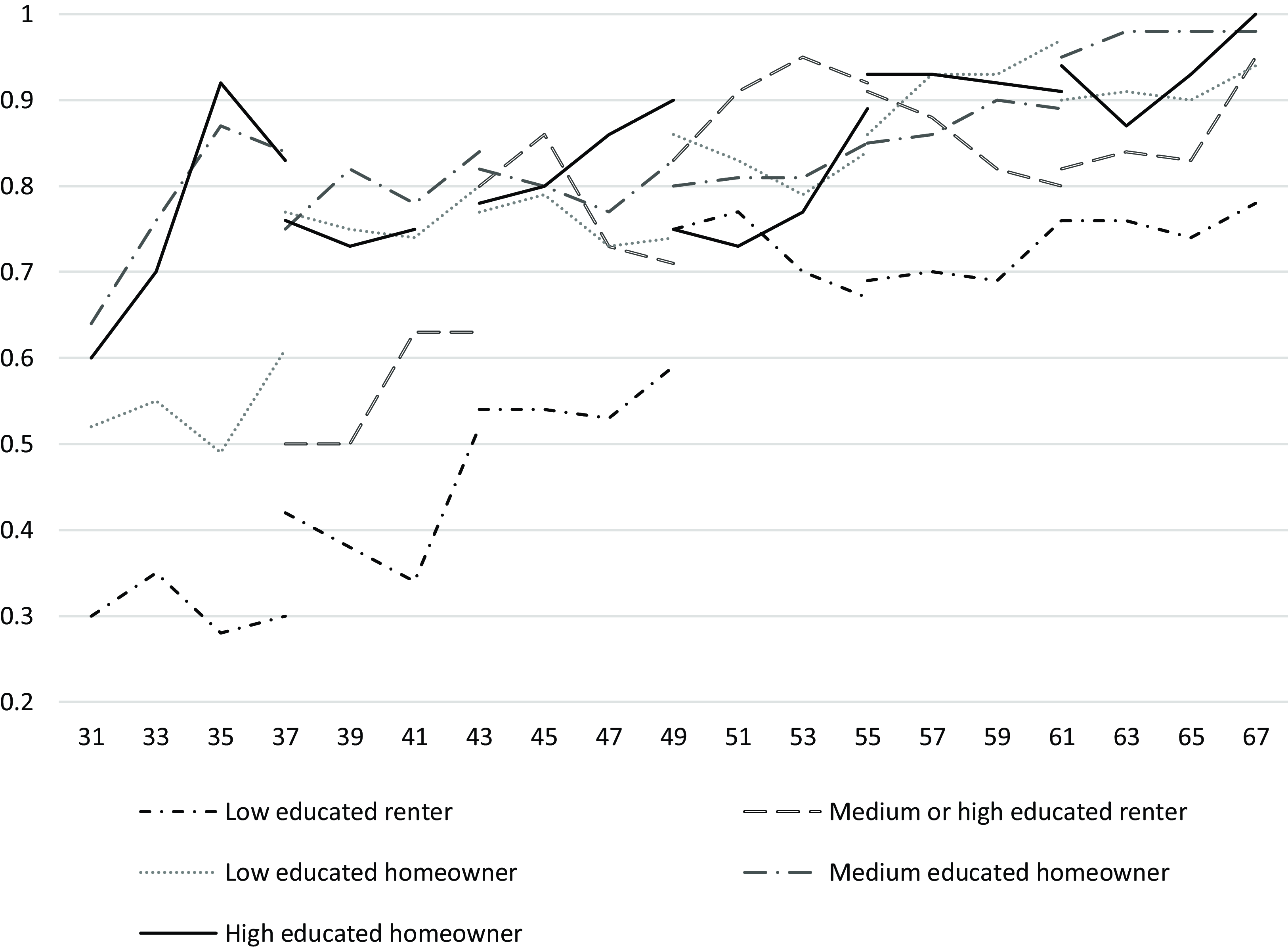

Figure 3, based on short 6-year unbalanced panels, plots the proportion of individuals reporting homeownership between 2010/12 and 2016/18 by family background. By matching the longitudinal sample analysis period with the age range within cohort groups we can analyse the changes in homeownership at the same age.Footnote 9 Figure 3 shows a clear trend in homeownership by family background. Around one in three offspring from the least advantaged group, those whose parents were low educated, report homeownership between age 31 and 37. Whereas the proportion increases from around 60% at age 31 to roughly 85% by age 37 among those whose parents are high educated homeowners. Figure 3 shows a degree of convergence at older ages; however, this refers to older cohorts who had greater absolute housing mobility, and a substantial gap of around 15–20% remains even in this cohort. Our findings suggest that homeownership opportunities are becoming increasingly unequal and stratified by parental wealth and based on current trends it is unlikely individuals born post-1980, especially those from the least advantaged backgrounds, will experience the same homeownership opportunities as their parents.

Figure 3. Home ownership by family background in WAS (2010/12–2016/18).

Notes: Proportion corresponds to individuals reporting housing wealth by single year age group, each group is defined by age and parent background. Based on unbalanced panel sample. N = 6,328. Proportions reported over 6 years corresponding with wave 3 (2010/12)–round 6 (2016/18) of WAS.

Importantly, our findings suggest the lack of homeownership opportunities among cohorts born after 1980 is more nuanced than is often debated. Comparing the youngest (31–37) and second youngest (37–43) cohorts in Figure 3 clearly shows individuals from the most disadvantaged backgrounds are less likely to report homeownership at the same age; however, no such pattern is found for the most advantaged groups. In fact, homeownership rates are higher based on this type of comparison. Among the latter group the proportion of individuals reporting homeownership at aged 37 in round 6 (2016/18) is roughly 10% higher than a slightly older cohort from the same family background. On the other hand, for cohorts whose parents are low-educated renters, there is a clear difference for the youngest group in the opposite direction, the proportion of individuals aged 37 in round 6 (2016/18) who report housing wealth is over 10% lower than a cohort slightly older from the same family background. Whilst this pattern is not evident at older ages, we note the most disadvantaged consistently report lower levels of homeownership relative to all other groups. Separately we note the levels of homeownership achieved by individuals from the most advantaged group by age 37 are comparable to the levels of homeownership reported by individuals from the least advantaged group in their early 60s.

Alongside homeownership, the rate at which the same individuals born to different cohorts accumulate housing wealth by parental background is relevant for understanding the drivers of wealth inequality in light of the findings in Table 4.

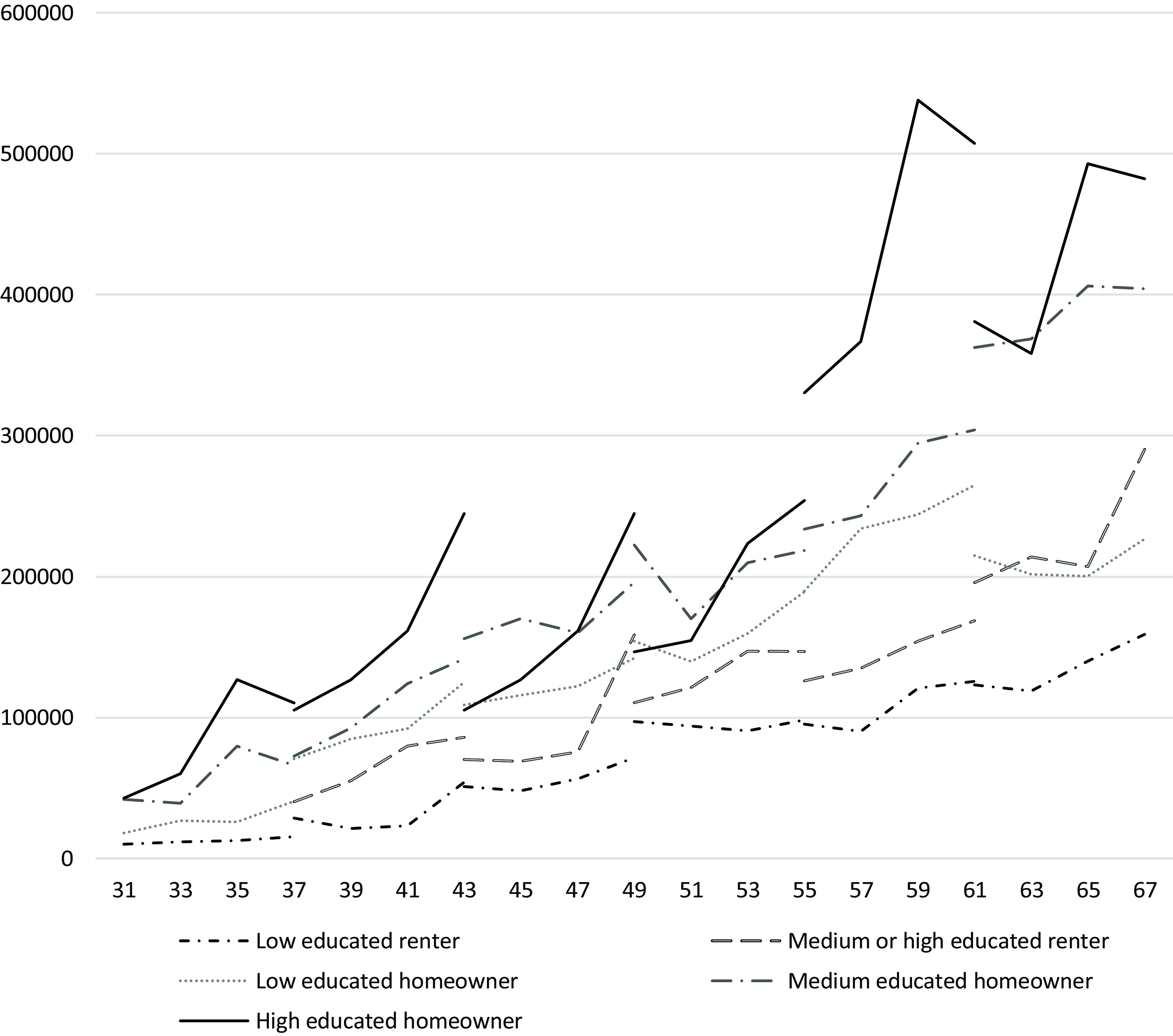

Figure 4 highlights that in addition to homeownership, the rate at which housing wealth is accumulated varies by family background. Given the profile of housing wealth accumulation by age group and parental background shown in Figure 1, this difference holds across the lifecourse. Between age 31 and 37 average housing wealth measured in 2022 prices among individuals from the least advantaged (most advantaged) backgrounds increased from £10,091 (£42,800) to £15,433 (£110,178), equivalent to an increase of 50% albeit from a low base. On the other hand, for those from the most advantaged background the average increase is over double the level reported at age 31, in absolute terms around £70,000 and over 35 times the absolute gain reported by individuals whose parents are low-educated renters. Thus, even at relatively young ages there is vast inequality in housing wealth as demonstrated in Figure 4, which plots accumulation of housing wealth by family background across successively younger cohorts. We note that the average level of housing wealth achieved by individuals from the most advantaged group by age 37 surpasses the levels of average housing wealth reported by individuals from the least advantaged group in their early 60s, the latter having arguably better homeownership opportunities than their counterparts from the same family background at younger ages.Footnote 10 Taken together the trends in Figures 3 and 4 suggest the cross-section differences in housing wealth reported in Figure 1 are set to widen in the future. Moreover, our results infer inequalities in housing wealth have been and are likely to continue driving the overall change in intergenerational wealth persistence in Britain.

Figure 4. Housing wealth by family background unbalanced panel.

Notes: Proportion corresponds to individuals reporting housing wealth by single age year, each group defined by age and parent background. Based on unbalanced panel sample minimum of one observation per individual to be included in sample. N = 6,328. Proportions reported over 6 years corresponding with wave 3 (2010/12)–round 6 (2016/18) of WAS.

Conclusion

Britain like many advanced economies has seen a rapid widening in wealth inequalities (Boserup, Reference Boserup, Kopczuk and Kreiner2017; Black et al., Reference Black, Devereux, Landaud and Salvanes2020; Gregg & Kanabar, Reference Gregg and Kanabar2022). Wealth significantly affects an individual’s living standards and is easily transferable, infering that inequalities early in adult life have profound implications for influencing major lifecycle events such as homeownership. Therefore, understanding which components of wealth drive offspring wealth inequality and how this is related to family background is of paramount importance if policymakers are to design effective policies to improve wealth and social mobility.

To our knowledge no studies have attempted to systematically study this question in Great Britain and quantify how rapidly family background is affecting offspring wealth inequalities, a gap we address in this paper. We show that in the case of Britain the change is largely attributable to growing inequalities in offspring homeownership and housing wealth. Between 2010/12 and 2016/18 we estimate the association between parental characteristics and offspring housing wealth increased by 0.036 rank points, and if this rate is maintained infers a doubling in the intergenerational correlation in roughly three decades. This finding is consistent with studies who seek to understand the evolution of wealth inequalities in the U.K. over a longer time period (Blanden et al., Reference Blanden, Eyles and Machin2023).

It is worth highlighting that our analysis covers a period when house prices and stock markets exhibited a strong upward trend, partly driven by historically low interest rates. Whilst this may contribute to the relationship between parental resources and offspring wealth outcomes, even if the return on certain assets slows, house price to earnings ratios remains close to historic highs and stagnant real earnings growth since 2007 suggests that homeownership is likely to remain highly stratified by parental background for younger cohorts. Even with the recent decline in housing prices in the U.K., higher interest rates have fed through to strong and persistent growth in rental costs, further hampering homeownership opportunities. Indeed, it is the least advantaged groups, which often includes renters, who have been disproportionately impacted by the cost-of-living crisis, and it is these same households who do not have buffers of liquid wealth to cushion shocks during prolonged periods of economic weakness. Finally, historic evidence shows that following many economic contractions in the U.K., house values have remained remarkably resilient and typically demonstrated strong growth in the subsequent post-recovery and expansionary period. So, without further policy intervention, a priori there is no reason to believe that the relationship we document between parental resources on the one hand and offspring wealth is unique to the sample period. For same arguments, we do not expect a decoupling between parental homeownership and education, these parental characteristics will continue to be useful markers of early life resources, in particular for research on intergenerational inequality and social mobility.

A second major finding is the divergence in homeownership and housing wealth across successively younger cohorts. By the time individuals born around 1980 reach their early 30s among those from the most advantaged background we find homeownership and housing wealth is being accumulated at a similar or even faster rate than slightly older cohorts. On the other hand, individuals from the most disadvantaged backgrounds in their early 30s are not only less likely to report homeownership compared to slightly older cohorts but the rate at which housing wealth is accumulated is also falling compared to individuals from the same parental background but who are slightly older. By age 35 homeownership levels are over three times higher among offspring whose parents are high-educated homeowners compared to individuals whose parents are from a low-educated renter background. In terms of housing wealth, the former group holds approximately 10 times the level reported by the latter. Such differences in housing wealth between the most and least advantaged persist between ages 30 and 64, and taken together with our findings are set to widen further. Importantly, we show that our results hold even after controlling for a range of offspring’s own characteristics, which are likely to influence homeownership such as earnings, education, sibling status and region of residence. More generally, our work contributes to ongoing debate regarding the historic returns from wealth versus human capital and its implications for individual social mobility (Piketty, Reference Piketty2017).

Taken together our findings infer the penalty for being born to parents with relatively low resources is growing rapidly over time in Great Britain, to the extent that it is influencing major lifecycle decisions such as the ability for offspring to access homeownership opportunities and hence the rate at which housing wealth can be accumulated. Our sample period corresponds to a period immediately following the Great Recession when the returns to housing were non-trivial: Average house prices in Britain grew by over 37% between 2010 and 2018 (ONS, 2021). Indeed, except for the period relating to the Great Recession there has been a consistent upward trend in house prices, quintupling between January 1990 and May 2022 (Land Registry, 2022). Thus, the illustrative predictions of future changes in the intergenerational wealth correlation we estimate are likely to reflect longer-term trends.

Despite various policies introduced to improve social mobility, such as the expansion of higher education that began in the 1960s in the U.K., and more recently targeted policies to help young people access homeownership such as Help to Buy, our findings suggest family background has only become more important in determining offspring wealth. Researchers have recently reconsidered the role wealth taxes could play in improving wealth inequality, or alternatively reforming certain regressive or inefficient elements of a country’s tax system, in the U.K. this includes inheritance, certain elements of capital gains and council tax (Glennerster, Reference Glennerster2012; Advani, Chamberlain, et al., Reference Advani, Chamberlain and Summers2020; Advani et al., Reference Advani, Hughson and Tarrant2021; Prabhakar, Reference Prabhakar2021). A wealth tax, given its inherent nature, will draw strong opinion both in public and policy settings. There are various reasons why such ideas have not been taken forward or subsequently dropped in the past, including inter-alia behavioural effects but also due to political economy reasons. Separately, better data and further research and understanding is needed on the exact design a wealth tax would take given such an initiative has not been actively discussed in the U.K. for 50 years, since which numerous economic and sociodemographic changes have taken place. Nevertheless, at a time when the tax burden in the U.K. is set to rise to levels not seen for 70 years, the recent announcements in the British government’s Spring 2023 Budget, which starting April 2024 remove the lifetime allowance on pension contributions and ongoing ability to drawdown 25% of pension pots tax free irrespective of pot size, benefits the wealthiest in society and is only likely to worsen, not improve, wealth inequality.

Supplementary material

To view supplementary material for this article, please visit https://doi.org/10.1017/S0047279423000442

Acknowledgements

The authors would like to thank the editor, two anonymous referees, Peter Eibich, Matt Dickson, Jo Blanden and Viola Hilbert for constructive feedback on an earlier versions of this paper.

Competing interests

The authors declare none.

Open access

Open access